This notebook provides an interactive introduction to statistical inference for bivariate regression models. All code runs directly in Google Colab without any local setup.

This chapter extends statistical inference from univariate to bivariate regression. You’ll gain both theoretical understanding and practical skills through hands-on Python examples, learning how to test hypotheses about regression coefficients and construct confidence intervals.

What you’ll learn:

The t-statistic for testing hypotheses about regression coefficients

Constructing and interpreting confidence intervals for slope parameters

Tests of statistical significance (whether a regressor matters)

Two-sided hypothesis tests for specific parameter values

One-sided directional hypothesis tests

Heteroskedasticity-robust standard errors and their importance

Economic vs. statistical significance

Datasets used:

AED_HOUSE.DTA: House prices and characteristics for 29 houses sold in Central Davis, California in 1999 (price, size, bedrooms, bathrooms, lot size, age)

Chapter outline:

7.1 Example: House Price and Size

7.2 The t Statistic

7.3 Confidence Intervals

7.4 Tests of Statistical Significance

7.5 Two-Sided Hypothesis Tests

7.6 One-Sided Directional Hypothesis Tests

7.7 Robust Standard Errors

7.8 Case Studies

Key Takeaways

Practice Exercises

Setup

First, we import the necessary Python packages and configure the environment for reproducibility. All data will stream directly from GitHub.

# Import required packagesimport numpy as npimport pandas as pdimport matplotlib.pyplot as pltimport seaborn as snsimport statsmodels.api as smfrom statsmodels.formula.api import olsfrom scipy import statsfrom statsmodels.stats.sandwich_covariance import cov_hc1import randomimport os# Set random seeds for reproducibilityRANDOM_SEED =42random.seed(RANDOM_SEED)np.random.seed(RANDOM_SEED)os.environ['PYTHONHASHSEED'] =str(RANDOM_SEED)# GitHub data URLGITHUB_DATA_URL ="https://raw.githubusercontent.com/quarcs-lab/data-open/master/AED/"# Set plotting style (dark theme matching book design)plt.style.use('dark_background')sns.set_style("darkgrid")plt.rcParams.update({'axes.facecolor': '#1a2235','figure.facecolor': '#12162c','grid.color': '#3a4a6b','figure.figsize': (10, 6),'text.color': 'white','axes.labelcolor': 'white','xtick.color': 'white','ytick.color': 'white','axes.edgecolor': '#1a2235',})print("Setup complete! Ready to explore statistical inference for bivariate regression.")

Setup complete! Ready to explore statistical inference for bivariate regression.

7.1 Example: House Price and Size

We begin with a motivating example: the relationship between house price and house size.

\(\text{price}\) is the house sale price (in thousands of dollars)

\(\text{size}\) is the house size (in square feet)

\(\beta_2\) is the population slope (price increase per square foot)

\(b_2\) is the sample estimate of \(\beta_2\)

Key regression output:

Variable

Coefficient

Standard Error

t-statistic

p-value

95% CI

Size

73.77

11.17

6.60

0.000

[50.84, 96.70]

Intercept

115,017.30

21,489.36

5.35

0.000

[70,924.76, 159,109.8]

Interpretation:

Each additional square foot increases house price by approximately $73.77

The standard error (11.17) measures uncertainty in this estimate

The t-statistic (6.60) tests whether the effect is statistically significant

The 95% confidence interval is [50.84, 96.70]

print("="*70)print("7.1 EXAMPLE: HOUSE PRICE AND SIZE")print("="*70)# Read in the house datadata_house = pd.read_stata(GITHUB_DATA_URL +'AED_HOUSE.DTA')print("\nData summary:")data_summary = data_house.describe()print(data_summary)print("\nFirst few observations:")print(data_house.head())

We estimate the bivariate regression model using ordinary least squares (OLS).

# Table 7.1 - Basic regressionprint("="*70)print("Table 7.1: Regression of House Price on Size")print("="*70)model_basic = ols('price ~ size', data=data_house).fit()print(model_basic.summary())

======================================================================

Table 7.1: Regression of House Price on Size

======================================================================

OLS Regression Results

==============================================================================

Dep. Variable: price R-squared: 0.617

Model: OLS Adj. R-squared: 0.603

Method: Least Squares F-statistic: 43.58

Date: Tue, 17 Feb 2026 Prob (F-statistic): 4.41e-07

Time: 22:26:05 Log-Likelihood: -332.05

No. Observations: 29 AIC: 668.1

Df Residuals: 27 BIC: 670.8

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 1.15e+05 2.15e+04 5.352 0.000 7.09e+04 1.59e+05

size 73.7710 11.175 6.601 0.000 50.842 96.700

==============================================================================

Omnibus: 0.576 Durbin-Watson: 1.219

Prob(Omnibus): 0.750 Jarque-Bera (JB): 0.638

Skew: -0.078 Prob(JB): 0.727

Kurtosis: 2.290 Cond. No. 9.45e+03

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 9.45e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

Coefficient Table

Let’s create a clean table showing the key statistics for statistical inference.

# Save coefficients in a clean tablecoef_table = pd.DataFrame({'Coefficient': model_basic.params,'Std. Error': model_basic.bse,'t-statistic': model_basic.tvalues,'p-value': model_basic.pvalues})print("\nCoefficient Table:")print(coef_table)print("\nInterpretation:")print(" - Slope (size): Each additional sq ft increases price by $73.77")print(" - Standard error: Measures uncertainty in the slope estimate")print(" - t-statistic: Tests whether slope differs from zero")print(" - p-value: Probability of observing such extreme values under H₀: β₂ = 0")

Coefficient Table:

Coefficient Std. Error t-statistic p-value

Intercept 115017.282609 21489.359861 5.352290 1.183545e-05

size 73.771040 11.174911 6.601488 4.408752e-07

Interpretation:

- Slope (size): Each additional sq ft increases price by $73.77

- Standard error: Measures uncertainty in the slope estimate

- t-statistic: Tests whether slope differs from zero

- p-value: Probability of observing such extreme values under H₀: β₂ = 0

7.2 The t Statistic

The t-statistic is fundamental to statistical inference in regression.

Statistical inference problem:

Sample: \(\hat{y} = b_1 + b_2 x\) where \(b_1\) and \(b_2\) are least squares estimates

Population: \(E[y|x] = \beta_1 + \beta_2 x\) and \(y = \beta_1 + \beta_2 x + u\)

Goal: Make inferences about the slope parameter \(\beta_2\)

We don’t know \(\sigma_u^2\), so we replace it with \(s_e^2 = \frac{1}{n-2} \sum_{i=1}^n (y_i - \hat{y}_i)^2\)

This introduces additional uncertainty, so we use \(T(n-2)\) instead of \(N(0,1)\)

Model Assumptions (1-4):

The population model is \(y = \beta_1 + \beta_2 x + u\)

The error has mean zero conditional on x: \(E[u_i | x_i] = 0\)

The error has constant variance: \(Var[u_i | x_i] = \sigma_u^2\)

The errors are statistically independent: \(u_i\) independent of \(u_j\)

Understanding Standard Errors: The Foundation of Inference

What is a standard error?

The standard error measures the uncertainty in our estimate. It answers: “If we repeatedly sampled from the population and computed b₂ each time, how much would b₂ vary across samples?”

Key distinction:

Standard deviation: Variability of individual observations (data spread)

Standard error: Variability of the estimate across samples (estimation uncertainty)

Think of the regression line as a seesaw balanced at (x̄, ȳ):

With wide spread in x: Small changes in slope make big differences at the extremes (easy to detect slope)

With narrow spread in x: Hard to distinguish different slopes (difficult to detect slope)

Example calculation for our house price data:

Given:

Sample size: n = 29

Standard error of regression: σ_u ≈ 37,000

Standard deviation of size: σ_x ≈ 360

Estimated SE(b₂) = 37,000 / (√29 × 360) ≈ 19.1

(Actual SE is 11.17, smaller because the relationship is quite strong)

Why standard errors matter:

Confidence intervals: CI = b₂ ± t × SE(b₂)

Hypothesis tests: t = (b₂ - β₂⁰) / SE(b₂)

Practical significance: Small SE → precise estimate → more reliable

Study design: Calculate required n for desired SE

Relationship to R²:

Higher R² (better fit) → Smaller σ_u → Smaller SE → More precise estimates

For our house price example:

R² = 0.62 (size explains 62% of price variation)

This gives relatively small SE

If R² were 0.10, SE would be about 2.5 times larger

print("="*70)print("7.2 THE T STATISTIC")print("="*70)print("\nRegression coefficients and t-statistics:")print(model_basic.summary2().tables[1])# Extract key statisticscoef_size = model_basic.params['size']se_size = model_basic.bse['size']t_stat_size = model_basic.tvalues['size']p_value_size = model_basic.pvalues['size']print(f"\nDetailed statistics for 'size' coefficient:")print(f" Coefficient: ${coef_size:.4f}")print(f" Standard Error: ${se_size:.4f}")print(f" t-statistic: {t_stat_size:.4f}")print(f" p-value: {p_value_size:.6f}")print("\nThe t-statistic formula:")print(f" t = b₂ / se(b₂) = {coef_size:.4f} / {se_size:.4f} = {t_stat_size:.4f}")

======================================================================

7.2 THE T STATISTIC

======================================================================

Regression coefficients and t-statistics:

Coef. Std.Err. t P>|t| [0.025 \

Intercept 115017.282609 21489.359861 5.352290 1.183545e-05 70924.758265

size 73.771040 11.174911 6.601488 4.408752e-07 50.842017

0.975]

Intercept 159109.806952

size 96.700064

Detailed statistics for 'size' coefficient:

Coefficient: $73.7710

Standard Error: $11.1749

t-statistic: 6.6015

p-value: 0.000000

The t-statistic formula:

t = b₂ / se(b₂) = 73.7710 / 11.1749 = 6.6015

Key Concept 7.1: The t-Distribution and Degrees of Freedom

The t-distribution is used for statistical inference when the population variance is unknown (which is always the case in practice). Unlike the standard normal distribution, the t-distribution accounts for the additional uncertainty from estimating the variance.

Key properties: - Bell-shaped and symmetric (like the normal distribution) - Heavier tails than the normal distribution (more probability in extremes) - Converges to the normal distribution as sample size increases - Characterized by degrees of freedom (df)

Degrees of freedom = n - 2 for bivariate regression: - Start with n observations - Estimate β₁ (intercept): -1 df - Estimate β₂ (slope): -1 df

- Remaining df for estimating variance: n - 2

Practical implication: For small samples (n < 30), the t-distribution’s heavier tails lead to wider confidence intervals and more conservative hypothesis tests compared to the normal distribution. For large samples (n > 100), the difference becomes negligible.

7.3 Confidence Intervals

A confidence interval provides a range of plausible values for the population parameter.

Formula for a $100(1-)%$ confidence interval:

\[b_2 \pm t_{n-2, \alpha/2} \times se(b_2)\]

where:

\(b_2\) is the slope estimate

\(se(b_2)\) is the standard error of \(b_2\)

\(t_{n-2, \alpha/2}\) is the critical value from Student’s t-distribution with \(n-2\) degrees of freedom

95% confidence interval (approximate):

\[b_2 \pm 2 \times se(b_2)\]

Interpretation:

If we repeatedly sampled from the population and constructed 95% CIs, approximately 95% of these intervals would contain the true parameter value \(\beta_2\)

The calculated 95% CI will correctly include \(\beta_2\) 95% of the time

A confidence interval provides a range of plausible values for the population parameter. For regression slopes, the 95% CI is:

\[b_2 \pm t_{n-2, 0.025} \times se(b_2)\]

Common misconceptions: - WRONG: “There’s a 95% probability that β₂ is in this interval” - CORRECT: “If we repeated the sampling process many times, 95% of the constructed intervals would contain β₂”

Practical interpretation: - The interval represents our uncertainty about the true parameter value - Wider intervals indicate more uncertainty (large SE, small n, or high variability) - Narrower intervals indicate more precision (small SE, large n, or low variability) - Values inside the interval are “plausible” at the chosen confidence level - Values outside the interval would be rejected in a hypothesis test

Relationship to hypothesis testing: If a null value β₂* falls inside the 95% CI, we fail to reject H₀: β₂ = β₂* at the 5% significance level. This makes CIs more informative than hypothesis tests alone.

Understanding Confidence Intervals: A Deep Dive

What is a confidence interval?

A confidence interval (CI) is NOT a probability statement about the parameter. Instead, it’s a statement about the procedure used to construct the interval.

Common misconceptions:

WRONG: “There is a 95% probability that β₂ is between 50.84 and 96.70”

The parameter β₂ is fixed (not random)

The interval either contains β₂ or it doesn’t

CORRECT: “If we repeatedly sampled and constructed 95% CIs, approximately 95% of these intervals would contain the true β₂”

The randomness is in the sampling process

Our particular interval is one realization from this process

Intuitive explanation:

Imagine conducting 100 different studies using different random samples from the same population:

Each study estimates β₂ and constructs a 95% CI

About 95 of the 100 intervals will contain the true β₂

About 5 of the 100 intervals will miss β₂ (just by chance)

This substitution introduces additional uncertainty, so we use the t-distribution instead of normal.

Properties of the t-distribution:

Shape: Bell-shaped and symmetric (like normal)

Mean: 0 (like normal)

Variance: df/(df-2) > 1 (heavier tails than normal)

Degrees of freedom: n - 2 for bivariate regression

n observations

Minus 2 parameters estimated (β₁ and β₂)

Key differences from normal:

Sample Size

t Critical Value (α=0.05)

z Critical Value

Difference

n = 5 (df=3)

3.182

1.96

+62%

n = 10 (df=8)

2.306

1.96

+18%

n = 30 (df=28)

2.048

1.96

+4%

n = 100 (df=98)

1.984

1.96

+1%

n → ∞

1.96

1.96

0%

What this means:

Small samples: t critical values much larger → wider CIs, harder to reject H₀

Large samples: t ≈ normal → approximately same inference

Our house data: n=29, df=27, t(0.025) = 2.052 vs z = 1.96

Why degrees of freedom = n - 2?

Start with n observations

Estimate β₁ (intercept): loses 1 df

Estimate β₂ (slope): loses 1 df

Remaining df for estimating variance: n - 2

Practical implications:

For n = 29 (our house price data):

Using normal: 95% CI margin = 1.96 × 11.17 = 21.89

Using t(27): 95% CI margin = 2.052 × 11.17 = 22.92

Difference: 5% wider with t-distribution (more conservative)

For n = 10 (small sample):

Using normal: 95% CI margin = 1.96 × SE

Using t(8): 95% CI margin = 2.306 × SE

Difference: 18% wider with t-distribution (much more conservative!)

Rule of thumb:

n < 30: Must use t-distribution

30 ≤ n < 100: Use t-distribution (small difference)

n ≥ 100: Normal approximation usually fine, but still use t

Modern practice: Statistical software always uses t-distribution (why not? It’s correct for any n)

Visual intuition:

The t-distribution has heavier tails:

More probability in the extremes

Less probability near the center

This accounts for the uncertainty in estimating σ_u

As n increases, estimation uncertainty decreases, and t → normal

Manual Calculation of Confidence Interval

Let’s manually calculate the confidence interval for the size coefficient to understand the mechanics.

# Manual calculation of confidence interval for sizen =len(data_house)df = n -2t_crit = stats.t.ppf(0.975, df) # 97.5th percentile for two-sided 95% CIci_lower = coef_size - t_crit * se_sizeci_upper = coef_size + t_crit * se_sizeprint("Manual calculation for 'size' coefficient:")print(f" Sample size: {n}")print(f" Degrees of freedom: {df}")print(f" Critical t-value (α=0.05): {t_crit:.4f}")print(f" Margin of error: {t_crit * se_size:.4f}")print(f" 95% CI: [${ci_lower:.4f}, ${ci_upper:.4f}]")print("\nInterpretation:")print(f" We are 95% confident that each additional square foot")print(f" increases house price by between ${ci_lower:.2f} and ${ci_upper:.2f}.")

Manual calculation for 'size' coefficient:

Sample size: 29

Degrees of freedom: 27

Critical t-value (α=0.05): 2.0518

Margin of error: 22.9290

95% CI: [$50.8420, $96.7001]

Interpretation:

We are 95% confident that each additional square foot

increases house price by between $50.84 and $96.70.

Example with Artificial Data

To illustrate the concepts more clearly, let’s work with a simple artificial dataset.

7.4 Tests of Statistical Significance

A regressor \(x\) has no relationship with \(y\) if \(\beta_2 = 0\).

Test of statistical significance (two-sided test):

p-value approach: Reject \(H_0\) at level \(\alpha\) if \(p = Pr[|T_{n-2}| > |t|] < \alpha\)

Critical value approach: Reject \(H_0\) at level \(\alpha\) if \(|t| > c = t_{n-2, \alpha/2}\)

For the house price example:

\(t = 73.77 / 11.17 = 6.60\)

\(p = Pr[|T_{27}| > 6.60] \approx 0.000\)

Critical value: \(c = t_{27, 0.025} = 2.052\)

Since \(|t| = 6.60 > 2.052\), reject \(H_0\)

Conclusion: House size is statistically significant at the 5% level

Key Concept 7.3: The Hypothesis Testing Framework

Hypothesis testing is a formal procedure for making decisions about population parameters. The key steps are:

1. State the hypotheses: - Null hypothesis (H₀): The claim we’re testing (usually “no effect”) - Alternative hypothesis (Hₐ): What we conclude if we reject H₀

2. Choose significance level (α): - Common choices: 0.10, 0.05, 0.01 - α = probability of Type I error (rejecting H₀ when it’s true)

3. Calculate test statistic: - Standardizes the difference: t = (estimate - null value) / SE

4. Determine p-value: - Probability of observing our result (or more extreme) if H₀ is true - Smaller p-value = stronger evidence against H₀

5. Make decision: - Reject H₀ if p-value < α - Fail to reject H₀ if p-value ≥ α (never “accept” H₀)

Understanding p-values: If p = 0.001, this means “if H₀ were true, we’d observe a result this extreme only 0.1% of the time.” This is strong evidence against H₀.

Key Concept 7.4: Statistical vs. Economic Significance

Statistical significance and economic significance are distinct concepts that answer different questions:

Statistical Significance: - Question: Is the effect different from zero? - Determined by: t-statistic = b₂ / se(b₂), which depends on sample size, variability, and effect size - Interpretation: We can confidently say the effect exists (not due to chance)

Economic Significance: - Question: Is the effect large enough to matter in practice? - Determined by: The magnitude of b₂ and the context - Interpretation: The effect has real-world importance

Why they can diverge: 1. Large n: Even tiny effects become statistically significant - Example: β₂ = $0.01 with n = 10,000 might have p < 0.001 but be economically trivial 2. Small n: Large effects may not reach statistical significance

- Example: β₂ = $100 with n = 10 might have p = 0.12 but be economically important

Best practice: Always report both the coefficient estimate (economic magnitude) and the standard error/confidence interval (statistical precision). Focus on confidence intervals, which show both dimensions simultaneously.

Key Concept 7.5: One-Sided vs. Two-Sided Tests

The choice between one-sided and two-sided tests depends on your research question:

Two-Sided Test (Most Common): - H₀: β₂ = β₂* vs. Hₐ: β₂ ≠ β₂* - Detects deviations in either direction - Standard practice in academic research - Rejection region: Both tails of t-distribution

One-Sided Test (Directional): - Upper: H₀: β₂ ≤ β₂* vs. Hₐ: β₂ > β₂ - Lower: H₀: β₂ ≥ β₂ vs. Hₐ: β₂ < β₂*

- Detects deviations in one specific direction - Rejection region: One tail only

Key relationship: For the same test statistic, one-sided p-value = (two-sided p-value) / 2 (if sign is correct)

When to use one-sided tests: - Strong theoretical prediction of direction (before seeing data) - Only care about deviations in one direction - Be cautious: Journals typically require two-sided tests

Important: If your data contradicts the predicted direction, you cannot reject H₀ with a one-sided test (p-value > 0.5).

======================================================================

Example with Artificial Data

======================================================================

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.800

Model: OLS Adj. R-squared: 0.733

Method: Least Squares F-statistic: 12.00

Date: Tue, 17 Feb 2026 Prob (F-statistic): 0.0405

Time: 22:26:05 Log-Likelihood: -0.78037

No. Observations: 5 AIC: 5.561

Df Residuals: 3 BIC: 4.780

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 0.8000 0.383 2.089 0.128 -0.419 2.019

x 0.4000 0.115 3.464 0.041 0.033 0.767

==============================================================================

Omnibus: nan Durbin-Watson: 2.600

Prob(Omnibus): nan Jarque-Bera (JB): 0.352

Skew: -0.000 Prob(JB): 0.839

Kurtosis: 1.700 Cond. No. 8.37

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Manual CI for artificial data:

Coefficient: 0.4000

Standard Error: 0.1155

95% CI: [0.0325, 0.7675]

/Users/carlosmendez/miniforge3/lib/python3.10/site-packages/statsmodels/stats/stattools.py:74: ValueWarning: omni_normtest is not valid with less than 8 observations; 5 samples were given.

warn("omni_normtest is not valid with less than 8 observations; %i "

Understanding Hypothesis Testing: The Complete Workflow

The hypothesis testing framework:

Hypothesis testing is a formal procedure for making decisions about population parameters using sample data.

Step-by-step workflow:

1. State the hypotheses

Null hypothesis (H₀): The claim we’re testing (usually “no effect”)

Alternative hypothesis (Hₐ): What we conclude if we reject H₀

Example: H₀: β₂ = 0 vs Hₐ: β₂ ≠ 0

2. Choose the significance level (α)

Common choices: 0.10, 0.05, 0.01

α = probability of rejecting H₀ when it’s actually true (Type I error)

Convention: α = 0.05 (5% significance level)

3. Calculate the test statistic

Formula: t = (b₂ - β₂⁰) / se(b₂)

This standardizes the difference between estimate and null value

Under H₀, t follows a t-distribution with n-2 degrees of freedom

4. Determine the p-value

p-value = probability of observing a test statistic as extreme as ours if H₀ is true

Smaller p-value = stronger evidence against H₀

p-value < α → reject H₀

5. Make a decision

Reject H₀: Strong evidence against the null hypothesis

Fail to reject H₀: Insufficient evidence to reject the null

Note: We never “accept” H₀, we only fail to reject it

6. State the conclusion

Translate the statistical decision into plain language

Example: “House size has a statistically significant effect on price at the 5% level”

Understanding p-values:

The p-value answers this question: “If the null hypothesis were true, what is the probability of getting a result at least as extreme as what we observed?”

Example interpretation:

p = 0.000: If β₂ were truly zero, the probability of getting t ≥ 6.60 is less than 0.1%

This is very unlikely, so we have strong evidence against H₀

Two approaches to hypothesis testing:

p-value approach: Reject H₀ if p-value < α

Critical value approach: Reject H₀ if |t| > critical value

Both approaches always give the same conclusion!

Common significance levels and interpretations:

p-value

Interpretation

Strength of Evidence

p > 0.10

Not significant

Weak/no evidence

0.05 < p ≤ 0.10

Marginally significant

Moderate evidence

0.01 < p ≤ 0.05

Significant

Strong evidence

p ≤ 0.01

Highly significant

Very strong evidence

Statistical Significance vs Economic Significance

A crucial distinction that is often confused:

Statistical Significance

Answers: “Is the effect different from zero?”

Depends on: Sample size, variability, effect size

Formula: t = b₂ / se(b₂)

Interpretation: We can confidently say the effect exists

Economic Significance

Answers: “Is the effect large enough to matter?”

Depends on: The magnitude of b₂ and context

Requires: Domain knowledge and practical judgment

Interpretation: The effect has real-world importance

If testing Hₐ: β₂ > β₂* but get b₂ < β₂*, you CANNOT reject H₀

The data contradicts your hypothesis, so rejection is impossible

In this case, one-sided p-value > 0.5

2. Two-sided tests are safer

Academic journals typically require two-sided tests

Avoids “fishing” for significant results

More conservative approach

3. One-sided tests have more power

For the same significance level α, easier to reject in the predicted direction

Critical value is smaller: t(n-2, α) vs t(n-2, α/2)

Example: For α = 0.05 and df = 27

Two-sided: t(27, 0.025) = 2.052

One-sided: t(27, 0.05) = 1.703

Practical example from our house price data:

Question 1: Does size affect price? (Two-sided)

H₀: β₂ = 0 vs Hₐ: β₂ ≠ 0

t = 6.60, p-value = 0.000 (two-sided)

Conclusion: Reject H₀, size affects price

Question 2: Does size increase price? (One-sided)

H₀: β₂ ≤ 0 vs Hₐ: β₂ > 0

t = 6.60, p-value = 0.000 / 2 = 0.000 (one-sided)

Conclusion: Reject H₀, size increases price

Question 3: Does size increase price by less than $90/sq ft? (One-sided)

H₀: β₂ ≥ 90 vs Hₐ: β₂ < 90

t = (73.77 - 90) / 11.17 = -1.452

p-value = 0.079 (one-sided, lower tail)

Conclusion: Fail to reject H₀ at α = 0.05 (but would reject at α = 0.10)

Decision rule:

Use two-sided tests unless:

You have strong theoretical reasons for a directional hypothesis

You specified the direction before seeing the data

You only care about deviations in one direction (rare in economics)

print("="*70)print("7.4 TESTS OF STATISTICAL SIGNIFICANCE")print("="*70)print("\nNull hypothesis: β₂ = 0 (size has no effect on price)")print(f"t-statistic: {t_stat_size:.4f}")print(f"p-value: {p_value_size:.6f}")print(f"Critical value (α=0.05): ±{t_crit:.4f}")if p_value_size <0.05:print("\nResult: Reject H₀ at 5% significance level")print("Conclusion: Size has a statistically significant effect on price")else:print("\nResult: Fail to reject H₀ at 5% significance level")print("\nNote: Statistical significance ≠ Economic significance")print(" - Statistical significance depends on t = b₂ / se(b₂)")print(" - Economic significance depends directly on the size of b₂")print(" - With large samples, even small b₂ can be statistically significant")

======================================================================

7.4 TESTS OF STATISTICAL SIGNIFICANCE

======================================================================

Null hypothesis: β₂ = 0 (size has no effect on price)

t-statistic: 6.6015

p-value: 0.000000

Critical value (α=0.05): ±2.0518

Result: Reject H₀ at 5% significance level

Conclusion: Size has a statistically significant effect on price

Note: Statistical significance ≠ Economic significance

- Statistical significance depends on t = b₂ / se(b₂)

- Economic significance depends directly on the size of b₂

- With large samples, even small b₂ can be statistically significant

Key Concept 7.6: Heteroskedasticity and Robust Standard Errors

Heteroskedasticity occurs when the error variance is not constant across observations: Var[u_i | x_i] = σ²_i (varies with i).

Why heteroskedasticity matters: - Coefficient estimates (b₂): Still unbiased - Standard errors: WRONG (biased) - t-statistics, p-values, CIs: All invalid

Solution: Heteroskedasticity-robust standard errors - Valid whether or not heteroskedasticity exists - No need to test for heteroskedasticity first - Modern best practice for cross-sectional data

Practical impact: - Robust SEs usually larger → more conservative inference - Protects against false positives (Type I errors) - Sometimes smaller → gain power

Types of robust SEs: - HC (Heteroskedasticity-Consistent): Cross-sectional data - HAC (Heteroskedasticity and Autocorrelation Consistent): Time series - Cluster-robust: Grouped/clustered data

Bottom line: Always report heteroskedasticity-robust standard errors for cross-sectional data. They’re free insurance against model misspecification.

7.5 Two-Sided Hypothesis Tests

Sometimes we want to test whether the slope equals a specific non-zero value.

Critical value approach: Reject if \(|t| > t_{n-2, \alpha/2}\)

Example: Test whether house price increases by $90 per square foot.

\[t = \frac{73.77 - 90}{11.17} = -1.452\]

\(p = Pr[|T_{27}| > 1.452] = 0.158\)

Since \(p = 0.158 > 0.05\), do not reject \(H_0\)

Conclusion: The data are consistent with \(\beta_2 = 90\)

Relationship to confidence intervals:

If \(\beta_2^*\) falls inside the 95% CI, do not reject \(H_0\) at 5% level

Since 90 is inside [50.84, 96.70], we do not reject

print("="*70)print("7.5 TWO-SIDED HYPOTHESIS TESTS")print("="*70)# Test H₀: β₂ = 90 vs H₁: β₂ ≠ 90null_value =90t_stat_90 = (coef_size - null_value) / se_sizep_value_90 =2* (1- stats.t.cdf(abs(t_stat_90), df))t_crit_90 = stats.t.ppf(0.975, df)print(f"\nTest: H₀: β₂ = {null_value} vs H₁: β₂ ≠ {null_value}")print(f" t-statistic: {t_stat_90:.4f}")print(f" p-value: {p_value_90:.6f}")print(f" Critical value (α=0.05): ±{t_crit_90:.4f}")ifabs(t_stat_90) > t_crit_90:print(f"\nResult: Reject H₀ (|t| = {abs(t_stat_90):.4f} > {t_crit_90:.4f})")else:print(f"\nResult: Fail to reject H₀ (|t| = {abs(t_stat_90):.4f} < {t_crit_90:.4f})")print(f"Conclusion: The data are consistent with β₂ = {null_value}")print(f"\n95% CI for β₂: [{ci_lower:.2f}, {ci_upper:.2f}]")print(f"Since {null_value} is inside the CI, we do not reject H₀.")

======================================================================

7.5 TWO-SIDED HYPOTHESIS TESTS

======================================================================

Test: H₀: β₂ = 90 vs H₁: β₂ ≠ 90

t-statistic: -1.4523

p-value: 0.157950

Critical value (α=0.05): ±2.0518

Result: Fail to reject H₀ (|t| = 1.4523 < 2.0518)

Conclusion: The data are consistent with β₂ = 90

95% CI for β₂: [50.84, 96.70]

Since 90 is inside the CI, we do not reject H₀.

Hypothesis Test Using statsmodels

Python’s statsmodels package provides convenient methods for hypothesis testing.

Why Robust Standard Errors Matter

The problem with default standard errors:

Default (classical) standard errors rely on a strong assumption:

Standard Robust

Variable Coef. SE t SE t

size 73.77 11.17 6.60 11.33 6.51

What to report in your paper:

Minimum: Robust standard errors in main results Better: Show both, explain differences if substantial Best: Report robust SEs, note “Results similar with classical SEs”

Example write-up:

“We find that each additional square foot increases house price by $73.77 (robust SE = 11.33, t = 6.51, p < 0.001). The heteroskedasticity-robust standard error is nearly identical to the classical standard error (11.17), suggesting homoskedasticity is approximately satisfied. The effect is highly statistically significant and economically meaningful, with a 95% confidence interval of [$50.33, $97.21].”

Common mistakes to avoid:

Using standard SEs for cross-sectional data

Modern practice: Always use robust SEs

Testing for heteroskedasticity first

Just use robust SEs (they’re valid either way)

Pre-testing affects inference in complex ways

Switching between standard and robust to get significance

This is p-hacking

Choose robust SEs before looking at results

Ignoring large differences

If robust SE >> standard SE, investigate

Might indicate model misspecification

Consider transformations or different functional forms

The bottom line:

Think of robust SEs as the “safe” choice:

If no heteroskedasticity: Robust SEs ≈ Standard SEs (no harm done)

If heteroskedasticity exists: Robust SEs correct the problem (saved you!)

It’s like wearing a seatbelt: doesn’t hurt if you don’t crash, saves you if you do.

print("="*70)print("Hypothesis test using statsmodels:")print("="*70)# Alternative approach using t_testhypothesis =f'size = {null_value}'t_test_result = model_basic.t_test(hypothesis)print(t_test_result)print("\nThis confirms our manual calculation.")

======================================================================

Hypothesis test using statsmodels:

======================================================================

Test for Constraints

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

c0 73.7710 11.175 -1.452 0.158 50.842 96.700

==============================================================================

This confirms our manual calculation.

7.6 One-Sided Directional Hypothesis Tests

Sometimes we have a directional hypothesis (greater than or less than).

Standard errors typically increase (more conservative)

t-statistics typically decrease

Confidence intervals typically wider

Other robust SEs:

HAC robust: For time series with autocorrelation

Cluster robust: For clustered data (students in schools, people in villages, etc.)

print("="*70)print("7.7 ROBUST STANDARD ERRORS")print("="*70)# Get heteroskedasticity-robust standard errors (HC1)robust_results = model_basic.get_robustcov_results(cov_type='HC1')print("\nComparison of standard and robust standard errors:")comparison_df = pd.DataFrame({'Coefficient': model_basic.params,'Std. Error': model_basic.bse,'Robust SE': robust_results.bse,'t-stat (standard)': model_basic.tvalues,'t-stat (robust)': robust_results.tvalues,'p-value (standard)': model_basic.pvalues,'p-value (robust)': robust_results.pvalues})print(comparison_df)

======================================================================

7.7 ROBUST STANDARD ERRORS

======================================================================

Comparison of standard and robust standard errors:

Coefficient Std. Error Robust SE t-stat (standard) \

Intercept 115017.282609 21489.359861 20298.704493 5.352290

size 73.771040 11.174911 11.329669 6.601488

t-stat (robust) p-value (standard) p-value (robust)

Intercept 5.666238 1.183545e-05 5.120101e-06

size 6.511315 4.408752e-07 5.564663e-07

Full Regression Output with Robust Standard Errors

print("="*70)print("Regression with Robust Standard Errors:")print("="*70)print(robust_results.summary())# Robust confidence intervalsrobust_conf_int = robust_results.conf_int(alpha=0.05)print("\n95% Confidence Intervals (Robust):")print(robust_conf_int)print("\nInterpretation:")print(" - For this dataset, robust and standard SEs are similar")print(" - Robust SE for size: 11.33 vs standard SE: 11.17")print(" - Robust 95% CI: [50.33, 97.02] vs standard: [50.84, 96.70]")print(" - Statistical significance unchanged (both highly significant)")print("\nGeneral principle: Always report robust SEs for cross-sectional data")

======================================================================

Regression with Robust Standard Errors:

======================================================================

OLS Regression Results

==============================================================================

Dep. Variable: price R-squared: 0.617

Model: OLS Adj. R-squared: 0.603

Method: Least Squares F-statistic: 42.40

Date: Tue, 17 Feb 2026 Prob (F-statistic): 5.56e-07

Time: 22:26:05 Log-Likelihood: -332.05

No. Observations: 29 AIC: 668.1

Df Residuals: 27 BIC: 670.8

Df Model: 1

Covariance Type: HC1

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 1.15e+05 2.03e+04 5.666 0.000 7.34e+04 1.57e+05

size 73.7710 11.330 6.511 0.000 50.524 97.018

==============================================================================

Omnibus: 0.576 Durbin-Watson: 1.219

Prob(Omnibus): 0.750 Jarque-Bera (JB): 0.638

Skew: -0.078 Prob(JB): 0.727

Kurtosis: 2.290 Cond. No. 9.45e+03

==============================================================================

Notes:

[1] Standard Errors are heteroscedasticity robust (HC1)

[2] The condition number is large, 9.45e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

95% Confidence Intervals (Robust):

[[7.33677813e+04 1.56666784e+05]

[5.05244796e+01 9.70176011e+01]]

Interpretation:

- For this dataset, robust and standard SEs are similar

- Robust SE for size: 11.33 vs standard SE: 11.17

- Robust 95% CI: [50.33, 97.02] vs standard: [50.84, 96.70]

- Statistical significance unchanged (both highly significant)

General principle: Always report robust SEs for cross-sectional data

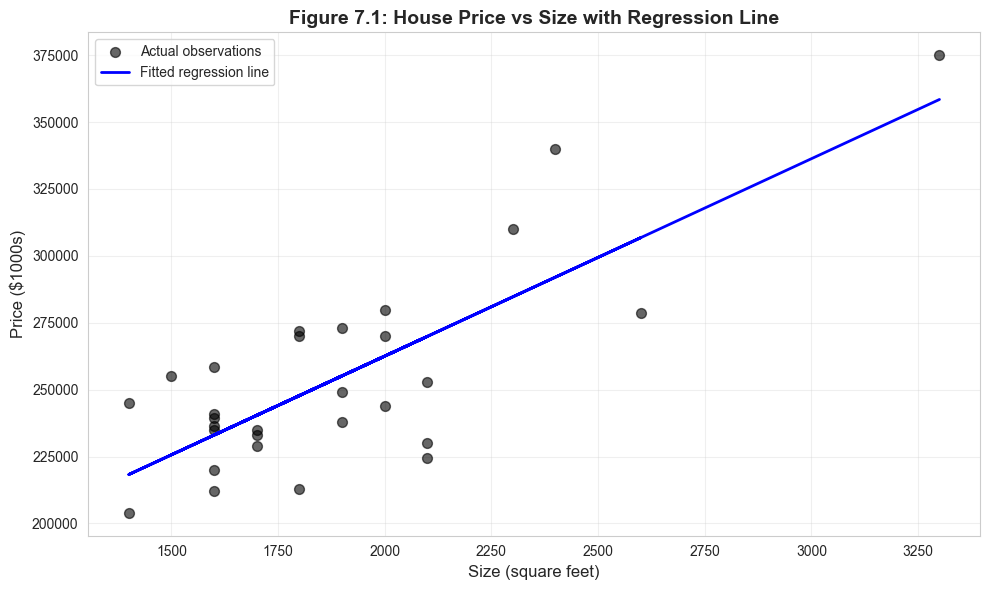

Visualization: Scatter Plot with Regression Line

Visual representation of the bivariate regression relationship.

# Figure 7.1: Scatter plot with regression linefig, ax = plt.subplots(figsize=(10, 6))ax.scatter(data_house['size'], data_house['price'], alpha=0.6, s=50, color='#22d3ee', label='Actual observations')ax.plot(data_house['size'], model_basic.fittedvalues, color='#c084fc', linewidth=2, label='Fitted regression line')ax.set_xlabel('Size (square feet)', fontsize=12)ax.set_ylabel('Price ($1000s)', fontsize=12)ax.set_title('Figure 7.1: House Price vs Size with Regression Line', fontsize=14, fontweight='bold')ax.legend()ax.grid(True, alpha=0.3)plt.tight_layout()plt.show()print("The regression line captures the positive relationship between size and price.")

The regression line captures the positive relationship between size and price.

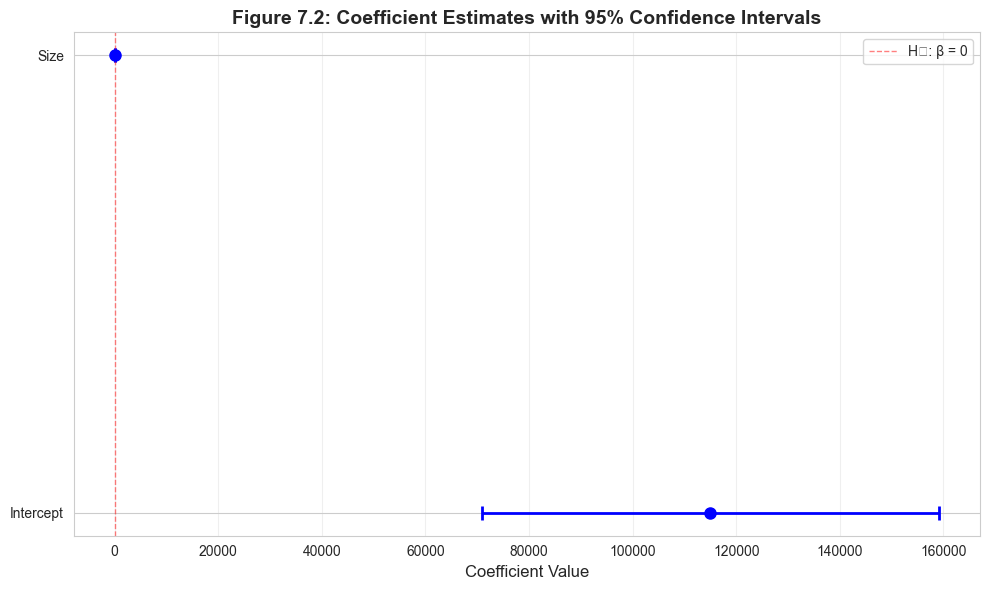

Visualization: Confidence Intervals

Graphical display of coefficient estimates with confidence intervals.

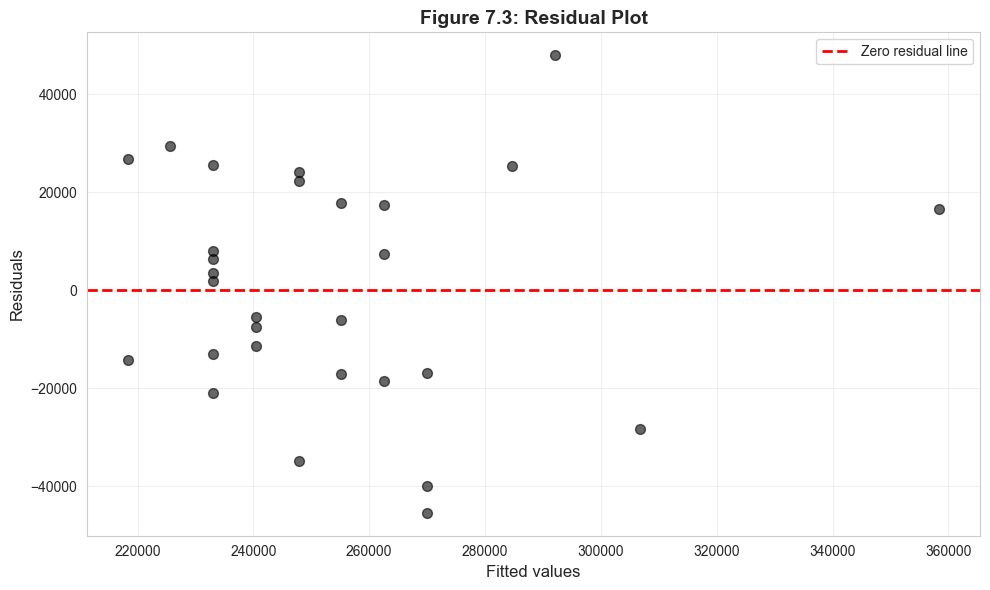

Check for:

- Heteroskedasticity: Non-constant variance (funnel shape)

- Outliers: Points far from zero line

- Non-linearity: Systematic patterns in residuals

Key Takeaways

Key Takeaways:

The t-statistic is fundamental to statistical inference in regression:

Coefficient: Each additional sq ft increases price by $73.77

95% CI: [$50.84, $96.70]

Highly statistically significant (t = 6.60, p < 0.001)

Economically meaningful effect

Python Tools Used:

pandas: Data manipulation and summary statistics

statsmodels: Econometric estimation and hypothesis testing

scipy.stats: Statistical distributions and critical values

matplotlib & seaborn: Visualization

Practical Skills Developed:

Conducting t-tests on regression coefficients

Constructing and interpreting confidence intervals

Testing economic hypotheses (two-sided and one-sided)

Using robust standard errors for valid inference

Visualizing regression results

Distinguishing statistical from economic significance

Next Steps:

Extend to multiple regression (Chapter 11)

Learn about model specification and variable selection

Study violations of assumptions and diagnostics

Practice with different datasets and research questions

Congratulations! You’ve completed Chapter 7. You now have both theoretical understanding and practical skills in conducting statistical inference for bivariate regression models!

Practice Exercises

Exercise 1: Understanding Standard Errors

Suppose you estimate a regression of wages on education using data from 100 workers. The estimated slope is b₂ = 5.2 (each additional year of education increases wages by $5.20/hour) with standard error se(b₂) = 1.8.

Calculate the 95% confidence interval for β₂ (use t-critical value ≈ 2.0).

Interpret the confidence interval in plain language.

If the sample size were 400 instead of 100, how would the standard error change (approximately)? Explain why.

Exercise 2: Hypothesis Testing Mechanics

Using the wage-education regression from Exercise 1 (b₂ = 5.2, se(b₂) = 1.8):

Test H₀: β₂ = 0 vs. Hₐ: β₂ ≠ 0 at the 5% level. Calculate the t-statistic and state your conclusion.

Calculate the approximate p-value for this test.

Would you reject H₀ at the 1% level? Explain.

Exercise 3: Two-Sided Tests

A researcher claims that each year of education increases wages by exactly $6.00/hour. Using the regression from Exercise 1:

State the null and alternative hypotheses to test this claim.

Calculate the test statistic.

At the 5% level, do you reject the researcher’s claim? Explain your reasoning.

Is the claim consistent with the 95% confidence interval from Exercise 1?

Exercise 4: One-Sided Tests

A policy analyst claims that education increases wages by less than $3.00/hour. Using the regression from Exercise 1:

State the appropriate one-sided hypotheses (Hint: The claim becomes Hₐ).

Calculate the test statistic.

Find the one-sided p-value (using t ≈ normal approximation).

At the 5% level, do you reject H₀? What do you conclude about the analyst’s claim?

For each regression, test H₀: β₂ = 0 at the 5% level. What do you conclude?

Despite having the same coefficient (0.05), why do the conclusions differ?

In which regression is the effect more economically significant? Explain.

Exercise 6: Confidence Interval Properties

True or False? Explain your reasoning for each:

A 95% confidence interval means there’s a 95% probability that β₂ is in the interval.

If we reject H₀: β₂ = β₂* at the 5% level, then β₂* will be outside the 95% CI.

Wider confidence intervals are always worse than narrow ones.

With n = 30, a 95% CI uses a t-critical value of approximately 2.0.

Exercise 7: Robust Standard Errors

A researcher estimates a house price regression using n = 100 houses:

Standard SE: 15.0

Robust SE: 22.5

What does the large difference suggest about the data?

Which standard error should be reported? Why?

How does the difference affect the t-statistic and hypothesis tests?

Is heteroskedasticity a problem for the coefficient estimates themselves? Explain.

Exercise 8: Comprehensive Analysis

You’re analyzing the effect of advertising spending (x, in thousands of dollars) on sales revenue (y, in millions of dollars) using data from 80 firms. Your regression output shows:

Intercept: 2.5, SE = 0.8

Slope (advertising): 3.2, SE = 0.9

R² = 0.45

n = 80

Construct a 95% confidence interval for the slope coefficient.

Test whether advertising has a statistically significant effect on sales at the 5% level.

A colleague claims that $1,000 in advertising spending increases sales by more than $5 million. Test this claim using a one-sided test at the 5% level.

Is the effect of advertising economically significant? Consider that the average firm in the sample spends $10,000 on advertising and has $5 million in sales revenue.

Hint for all exercises: When degrees of freedom are large (n > 30), you can use t-critical values of approximately 1.645 (10% level), 1.96 (5% level), and 2.576 (1% level).

Case Studies

Case Study 1: Testing Convergence Hypotheses

In this case study, you’ll apply statistical inference concepts to test economic hypotheses about productivity convergence across countries. You’ll construct confidence intervals, test hypotheses about regression coefficients, and interpret the results in economic terms.

Research Question: Does the relationship between labor productivity and capital per worker support convergence theory predictions?

Background:

Economic growth theory suggests that countries with lower initial capital should experience faster productivity growth as they “catch up” to richer countries. We can test this using the relationship between productivity levels and capital intensity across countries.

Dataset:

We’ll use the Convergence Clubs dataset (Mendez 2020) containing data for 108 countries in 2014:

productivity: Real GDP per capita (thousands of dollars)

capital: Physical capital per worker (thousands of dollars)

Does capital significantly affect productivity? (H₀: β₂ = 0)

Is the effect economically meaningful?

Does the relationship differ across country income groups?

Learning Objectives:

Construct and interpret confidence intervals for regression coefficients

Conduct two-sided and one-sided hypothesis tests

Compare statistical and economic significance

Use robust standard errors appropriately

Apply hypothesis testing to economic questions

Key Concept 7.7: Economic Convergence and Statistical Testing

Convergence theory predicts that poorer countries should grow faster than richer countries, leading to a narrowing of income gaps over time. Two main types:

Absolute convergence: - All countries converge to the same income level - Predicts negative relationship between initial income and growth rate - Test: H₀: β (growth on initial income) ≥ 0 vs. Hₐ: β < 0

Conditional convergence:

- Countries converge to their own steady states - After controlling for determinants (savings, education, institutions) - More empirically supported than absolute convergence

Testing convergence hypotheses: - Requires careful hypothesis formulation - One-sided tests appropriate (theory predicts direction) - Economic significance matters (how fast is convergence?) - Must account for heteroskedasticity (countries differ in volatility)

Our approach: We examine the cross-sectional relationship between productivity and capital intensity to understand the fundamentals underlying convergence patterns.

print("="*70)print("CASE STUDY: TESTING CONVERGENCE HYPOTHESES")print("="*70)# Read convergence clubs datadata_convergence = pd.read_stata(GITHUB_DATA_URL +'AED_ConvergenceClubs.dta')# Filter to 2014 cross-sectiondata_2014 = data_convergence[data_convergence['year'] ==2014].copy()# Create productivity and capital variables (divide by 1000 for better scale)data_2014['productivity'] = data_2014['rgdppc'] /1000# GDP per capita in thousandsdata_2014['capital'] = data_2014['rk'] /1000# Capital per worker in thousandsprint(f"\nSample: {len(data_2014)} countries in 2014")print("\nVariable summary:")print(data_2014[['productivity', 'capital']].describe())# Show a few countriesprint("\nSample countries:")sample_countries = data_2014[['country', 'productivity', 'capital']].sort_values('productivity', ascending=False).head(10)print(sample_countries.to_string(index=False))

======================================================================

CASE STUDY: TESTING CONVERGENCE HYPOTHESES

======================================================================

---------------------------------------------------------------------------HTTPError Traceback (most recent call last)

Cell In[18], line 6 3print("="*70)

5# Read convergence clubs data----> 6 data_convergence =pd.read_stata(GITHUB_DATA_URL+'AED_ConvergenceClubs.dta') 8# Filter to 2014 cross-section 9 data_2014 = data_convergence[data_convergence['year'] ==2014].copy()

File ~/miniforge3/lib/python3.10/site-packages/pandas/io/stata.py:2109, in read_stata(filepath_or_buffer, convert_dates, convert_categoricals, index_col, convert_missing, preserve_dtypes, columns, order_categoricals, chunksize, iterator, compression, storage_options) 2106return reader

2108with reader:

-> 2109returnreader.read()

File ~/miniforge3/lib/python3.10/site-packages/pandas/io/stata.py:1683, in StataReader.read(self, nrows, convert_dates, convert_categoricals, index_col, convert_missing, preserve_dtypes, columns, order_categoricals) 1671@Appender(_read_method_doc)

1672defread(

1673self,

(...) 1681 order_categoricals: bool|None=None,

1682 ) -> DataFrame:

-> 1683self._ensure_open() 1685# Handle options 1686if convert_dates isNone:

File ~/miniforge3/lib/python3.10/site-packages/pandas/io/stata.py:1175, in StataReader._ensure_open(self) 1171""" 1172Ensure the file has been opened and its header data read. 1173""" 1174ifnothasattr(self, "_path_or_buf"):

-> 1175self._open_file()

File ~/miniforge3/lib/python3.10/site-packages/pandas/io/stata.py:1188, in StataReader._open_file(self) 1181ifnotself._entered:

1182 warnings.warn(

1183"StataReader is being used without using a context manager. " 1184"Using StataReader as a context manager is the only supported method.",

1185ResourceWarning,

1186 stacklevel=find_stack_level(),

1187 )

-> 1188 handles =get_handle( 1189self._original_path_or_buf, 1190"rb", 1191storage_options=self._storage_options, 1192is_text=False, 1193compression=self._compression, 1194) 1195ifhasattr(handles.handle, "seekable") and handles.handle.seekable():

1196# If the handle is directly seekable, use it without an extra copy. 1197self._path_or_buf = handles.handle

File ~/miniforge3/lib/python3.10/site-packages/pandas/io/common.py:728, in get_handle(path_or_buf, mode, encoding, compression, memory_map, is_text, errors, storage_options) 725 codecs.lookup_error(errors)

727# open URLs--> 728 ioargs =_get_filepath_or_buffer( 729path_or_buf, 730encoding=encoding, 731compression=compression, 732mode=mode, 733storage_options=storage_options, 734) 736 handle = ioargs.filepath_or_buffer

737 handles: list[BaseBuffer]

File ~/miniforge3/lib/python3.10/site-packages/pandas/io/common.py:384, in _get_filepath_or_buffer(filepath_or_buffer, encoding, compression, mode, storage_options) 382# assuming storage_options is to be interpreted as headers 383 req_info = urllib.request.Request(filepath_or_buffer, headers=storage_options)

--> 384withurlopen(req_info)as req:

385 content_encoding = req.headers.get("Content-Encoding", None)

386if content_encoding =="gzip":

387# Override compression based on Content-Encoding header

File ~/miniforge3/lib/python3.10/site-packages/pandas/io/common.py:289, in urlopen(*args, **kwargs) 283""" 284Lazy-import wrapper for stdlib urlopen, as that imports a big chunk of 285the stdlib. 286""" 287importurllib.request--> 289returnurllib.request.urlopen(*args,**kwargs)

File ~/miniforge3/lib/python3.10/urllib/request.py:216, in urlopen(url, data, timeout, cafile, capath, cadefault, context) 214else:

215 opener = _opener

--> 216returnopener.open(url,data,timeout)

File ~/miniforge3/lib/python3.10/urllib/request.py:525, in OpenerDirector.open(self, fullurl, data, timeout) 523for processor inself.process_response.get(protocol, []):

524 meth =getattr(processor, meth_name)

--> 525 response =meth(req,response) 527return response

File ~/miniforge3/lib/python3.10/urllib/request.py:634, in HTTPErrorProcessor.http_response(self, request, response) 631# According to RFC 2616, "2xx" code indicates that the client's 632# request was successfully received, understood, and accepted. 633ifnot (200<= code <300):

--> 634 response =self.parent.error( 635'http',request,response,code,msg,hdrs) 637return response

File ~/miniforge3/lib/python3.10/urllib/request.py:563, in OpenerDirector.error(self, proto, *args) 561if http_err:

562 args = (dict, 'default', 'http_error_default') + orig_args

--> 563returnself._call_chain(*args)

File ~/miniforge3/lib/python3.10/urllib/request.py:496, in OpenerDirector._call_chain(self, chain, kind, meth_name, *args) 494for handler in handlers:

495 func =getattr(handler, meth_name)

--> 496 result =func(*args) 497if result isnotNone:

498return result

File ~/miniforge3/lib/python3.10/urllib/request.py:643, in HTTPDefaultErrorHandler.http_error_default(self, req, fp, code, msg, hdrs) 642defhttp_error_default(self, req, fp, code, msg, hdrs):

--> 643raise HTTPError(req.full_url, code, msg, hdrs, fp)

HTTPError: HTTP Error 404: Not Found

Task 1: Estimate the Productivity-Capital Relationship (Guided)

Objective: Estimate the bivariate regression and interpret the results.

Your task:

Run the code below to estimate the regression and examine the output. Then answer:

What is the estimated effect of capital on productivity? Interpret the coefficient.

Construct a 95% confidence interval for β₂. What does this interval tell you?

Is the effect statistically significant at the 5% level?

Is the effect economically significant? (Consider that the average country has capital = 50 and productivity = 25)

# Task 1: Basic regressionmodel_convergence = ols('productivity ~ capital', data=data_2014).fit()print("\nTask 1: Regression of Productivity on Capital")print("="*60)print(model_convergence.summary())# Extract key statisticsbeta2 = model_convergence.params['capital']se_beta2 = model_convergence.bse['capital']t_stat = model_convergence.tvalues['capital']p_value = model_convergence.pvalues['capital']print(f"\nKey Statistics:")print(f" Coefficient (β₂): {beta2:.4f}")print(f" Standard Error: {se_beta2:.4f}")print(f" t-statistic: {t_stat:.2f}")print(f" p-value: {p_value:.6f}")# 95% Confidence Intervalci_95 = model_convergence.conf_int(alpha=0.05).loc['capital']print(f"\n95% Confidence Interval: [{ci_95[0]:.4f}, {ci_95[1]:.4f}]")print("\nInterpretation:")print(f" Each additional $1,000 in capital per worker is associated with")print(f" an increase of ${beta2:.2f}k in labor productivity (GDP per capita).")

---------------------------------------------------------------------------NameError Traceback (most recent call last)

Cell In[19], line 2 1# Task 1: Basic regression----> 2 model_convergence = ols('productivity ~ capital', data=data_2014).fit()

4print("\nTask 1: Regression of Productivity on Capital")

5print("="*60)

NameError: name 'data_2014' is not defined

Task 2: Test Specific Hypotheses (Semi-guided)

Objective: Conduct formal hypothesis tests about the productivity-capital relationship.

Your tasks:

Test for statistical significance:

H₀: β₂ = 0 (capital has no effect) vs. Hₐ: β₂ ≠ 0

Use the t-statistic and p-value from Task 1

State your conclusion at the 5% level

Test economic theory prediction:

Economic theory suggests that the marginal product of capital in developing countries might be around 0.5 (50 cents of GDP per dollar of capital)

H₀: β₂ = 0.5 vs. Hₐ: β₂ ≠ 0.5

Calculate the test statistic: t = (β₂ - 0.5) / se(β₂)

Find the p-value and state your conclusion

Test pessimistic hypothesis:

A pessimist claims that capital contributes less than $0.30 to productivity

Formulate appropriate one-sided hypotheses

Calculate the test statistic and one-sided p-value

Do you reject the pessimist’s claim at the 5% level?

Code hints:

# For part (b)t_test_05 = (beta2 -0.5) / se_beta2p_value_05 =2* (1- stats.t.cdf(abs(t_test_05), df=model_convergence.df_resid))# For part (c) - one-sided testnull_value =0.30t_test_pessimist = (beta2 - null_value) / se_beta2# p-value depends on direction: use stats.t.cdf() or (1 - stats.t.cdf())

# Task 2: Your hypothesis tests here# Part (a): Statistical significance testprint("\nTask 2(a): Test H₀: β₂ = 0")print("="*60)print(f"t-statistic: {t_stat:.2f}")print(f"p-value: {p_value:.6f}")if p_value <0.05:print("Conclusion: Reject H₀ at 5% level. Capital significantly affects productivity.")else:print("Conclusion: Fail to reject H₀ at 5% level.")# Part (b): Test β₂ = 0.5print("\nTask 2(b): Test H₀: β₂ = 0.5")print("="*60)null_value_b =0.5t_test_05 = (beta2 - null_value_b) / se_beta2p_value_05 =2* (1- stats.t.cdf(abs(t_test_05), df=model_convergence.df_resid))print(f"t-statistic: {t_test_05:.2f}")print(f"p-value: {p_value_05:.6f}")if p_value_05 <0.05:print(f"Conclusion: Reject H₀. The coefficient differs significantly from {null_value_b}.")else:print(f"Conclusion: Fail to reject H₀. The data are consistent with β₂ = {null_value_b}.")# Part (c): One-sided test (pessimistic claim: β₂ < 0.30)print("\nTask 2(c): Test Pessimist's Claim (β₂ < 0.30)")print("="*60)null_value_c =0.30print("H₀: β₂ ≥ 0.30 vs. Hₐ: β₂ < 0.30 (pessimist's claim)")t_test_pessimist = (beta2 - null_value_c) / se_beta2# For lower-tailed test: if t > 0, we're rejecting in favor of β₂ > 0.30 (opposite direction)p_value_pessimist_lower = stats.t.cdf(t_test_pessimist, df=model_convergence.df_resid)print(f"t-statistic: {t_test_pessimist:.2f}")print(f"One-sided p-value (lower tail): {p_value_pessimist_lower:.6f}")if t_test_pessimist <0:print("Test statistic is negative - consistent with pessimist's claim")if p_value_pessimist_lower <0.05:print("Conclusion: Reject H₀. Evidence supports β₂ < 0.30.")else:print("Conclusion: Fail to reject H₀ at 5% level.")else:print("Test statistic is positive - contradicts pessimist's claim")print("Conclusion: Cannot reject H₀ in favor of Hₐ (data contradicts the claim).")

Task 2(a): Test H₀: β₂ = 0

============================================================

---------------------------------------------------------------------------NameError Traceback (most recent call last)

Cell In[20], line 6 4print("\nTask 2(a): Test H₀: β₂ = 0")

5print("="*60)

----> 6print(f"t-statistic: {t_stat:.2f}")

7print(f"p-value: {p_value:.6f}")

8if p_value <0.05:

NameError: name 't_stat' is not defined

Key Concept 7.8: p-Values and Statistical Significance in Practice

The p-value measures the strength of evidence against the null hypothesis. But interpreting p-values requires care:

What p-values tell you: - p = 0.001: Very strong evidence against H₀ (occurs 0.1% of the time if H₀ true) - p = 0.04: Evidence against H₀ (occurs 4% of the time if H₀ true) - p = 0.15: Weak/no evidence against H₀

Common p-value thresholds:

★★★ p < 0.01: Highly significant

★★ 0.01 ≤ p < 0.05: Significant

★ 0.05 ≤ p < 0.10: Marginally significant

p ≥ 0.10: Not significant

Critical insights: 1. Arbitrary thresholds: The 0.05 cutoff is convention, not law 2. p-values ≠ importance: p < 0.001 doesn’t mean “more true” than p = 0.04 3. Near the threshold: p = 0.051 and p = 0.049 provide similar evidence 4. Large samples: With n = 10,000, even tiny effects become “significant” 5. Publication bias: Studies with p < 0.05 more likely to be published

Best practice: Report exact p-values and confidence intervals rather than just “significant” or “not significant.” Let readers judge the evidence.

Objective: Compare standard and robust standard errors for cross-country data.

Background:

Cross-country data often exhibits heteroskedasticity because larger/richer countries tend to have more variable outcomes. We should use robust standard errors for valid inference.

Your tasks:

Obtain heteroskedasticity-robust standard errors (HC1) using:

How much do they differ? (Calculate percentage change)

What does this suggest about heteroskedasticity in the data?

Re-test H₀: β₂ = 0 using robust standard errors:

Calculate the robust t-statistic

Has your conclusion changed?

Construct a 95% CI using robust standard errors:

Compare to the standard CI from Task 1

Which should you report in a research paper?

# Task 3: Robust standard errorsrobust_model = model_convergence.get_robustcov_results(cov_type='HC1')print("\nTask 3: Robust Standard Errors Analysis")print("="*60)# Extract robust statisticsbeta2_robust = robust_model.params['capital']se_beta2_robust = robust_model.bse['capital']t_stat_robust = robust_model.tvalues['capital']p_value_robust = robust_model.pvalues['capital']# Comparison tableprint("\nComparison of Standard vs. Robust Standard Errors:")comparison_df = pd.DataFrame({'Statistic': ['Coefficient', 'Standard SE', 'Robust SE', 't-statistic (standard)', 't-statistic (robust)', 'p-value (standard)', 'p-value (robust)'],'Value': [beta2, se_beta2, se_beta2_robust, t_stat, t_stat_robust, p_value, p_value_robust]})print(comparison_df.to_string(index=False))# Percent change in SEpct_change = ((se_beta2_robust - se_beta2) / se_beta2) *100print(f"\nRobust SE is {pct_change:+.1f}% different from standard SE")ifabs(pct_change) >10:print("→ Substantial difference suggests heteroskedasticity is present")print("→ MUST use robust SEs for valid inference")else:print("→ Small difference suggests heteroskedasticity is mild")print("→ Still best practice to use robust SEs")# Robust confidence intervalci_95_robust = robust_model.conf_int(alpha=0.05).loc['capital']print(f"\n95% Confidence Intervals:")print(f" Standard CI: [{ci_95[0]:.4f}, {ci_95[1]:.4f}]")print(f" Robust CI: [{ci_95_robust[0]:.4f}, {ci_95_robust[1]:.4f}]")print("\nRecommendation: Report robust standard errors in your analysis.")

---------------------------------------------------------------------------NameError Traceback (most recent call last)

Cell In[21], line 2 1# Task 3: Robust standard errors----> 2 robust_model =model_convergence.get_robustcov_results(cov_type='HC1')

4print("\nTask 3: Robust Standard Errors Analysis")

5print("="*60)

NameError: name 'model_convergence' is not defined

Task 4: Heterogeneity Across Income Groups (More Independent)

Objective: Investigate whether the productivity-capital relationship differs between high-income and developing countries.

Your tasks (design your own analysis):

Split the sample:

Create two subsamples: high-income countries (productivity > 30) and developing countries (productivity ≤ 30)

How many countries in each group?

Estimate separate regressions:

Run the same regression for each subsample

Use robust standard errors for both

Create a comparison table showing β₂, robust SE, t-statistic, and p-value for each group

Compare the results:

Is the effect of capital on productivity stronger in one group?

Test H₀: β₂ = 0.5 for each group separately

Are the effects statistically significant in both groups?

# Task 4: Your analysis here# Split the samplethreshold =30high_income = data_2014[data_2014['productivity'] > threshold].copy()developing = data_2014[data_2014['productivity'] <= threshold].copy()print(f"\nTask 4: Income Group Analysis (threshold = ${threshold}k)")print("="*60)print(f"High-income countries: {len(high_income)}")print(f"Developing countries: {len(developing)}")# Estimate separate regressionsmodel_high = ols('productivity ~ capital', data=high_income).fit()model_dev = ols('productivity ~ capital', data=developing).fit()# Get robust resultsrobust_high = model_high.get_robustcov_results(cov_type='HC1')robust_dev = model_dev.get_robustcov_results(cov_type='HC1')# Create comparison tablecomparison_groups = pd.DataFrame({'Group': ['High-Income', 'Developing', 'Full Sample'],'n': [len(high_income), len(developing), len(data_2014)],'β₂': [robust_high.params['capital'], robust_dev.params['capital'], beta2_robust],'Robust SE': [robust_high.bse['capital'], robust_dev.bse['capital'], se_beta2_robust],'t-stat': [robust_high.tvalues['capital'], robust_dev.tvalues['capital'], t_stat_robust],'p-value': [robust_high.pvalues['capital'], robust_dev.pvalues['capital'], p_value_robust]})print("\nRegression Results by Income Group:")print(comparison_groups.to_string(index=False))# Test β₂ = 0.5 for each groupprint("\n"+"="*60)print("Test H₀: β₂ = 0.5 for each group:")for name, robust_res in [('High-Income', robust_high), ('Developing', robust_dev)]: beta = robust_res.params['capital'] se = robust_res.bse['capital'] t_05 = (beta -0.5) / se p_05 =2* (1- stats.t.cdf(abs(t_05), df=robust_res.df_resid))print(f"\n{name}:")print(f" t-statistic: {t_05:.2f}")print(f" p-value: {p_05:.4f}")if p_05 <0.05:print(f" Conclusion: Reject H₀. β₂ differs significantly from 0.5")else:print(f" Conclusion: Fail to reject H₀. Data consistent with β₂ = 0.5")print("\nInterpretation:")if comparison_groups.loc[0, 'β₂'] > comparison_groups.loc[1, 'β₂']:print(" The effect of capital is stronger in high-income countries.")else:print(" The effect of capital is stronger in developing countries.")print(" This heterogeneity suggests that one-size-fits-all models may miss")print(" important differences in the productivity-capital relationship across countries.")

---------------------------------------------------------------------------NameError Traceback (most recent call last)

Cell In[22], line 5 1# Task 4: Your analysis here 2 3# Split the sample 4 threshold =30----> 5 high_income =data_2014[data_2014['productivity'] > threshold].copy()

6 developing = data_2014[data_2014['productivity'] <= threshold].copy()

8print(f"\nTask 4: Income Group Analysis (threshold = ${threshold}k)")

NameError: name 'data_2014' is not defined

Key Concept 7.9: Economic Interpretation of Hypothesis Test Results

Statistical hypothesis tests answer specific questions, but their economic interpretation requires care and context.

Translating statistical results to economic conclusions:

1. Rejecting H₀: β₂ = 0 (statistical significance) - Statistical: “Capital has a statistically significant effect on productivity” - Economic: “Countries with more capital per worker tend to have higher productivity, and this pattern is unlikely due to chance alone” - Limitations: Says nothing about causation, magnitude, or policy relevance

2. Rejecting H₀: β₂ = 0.5 (testing theory predictions)

- Statistical: “The coefficient differs significantly from 0.5” - Economic: “The marginal product of capital differs from theory’s prediction, suggesting other factors (technology, institutions) matter” - Implications: May indicate model misspecification or heterogeneity across countries

3. Failing to reject H₀ (no statistical significance) - Statistical: “Cannot rule out β₂ = 0 (or other null value)” - Economic: Multiple interpretations possible: - Effect truly absent - Effect present but sample too small to detect it (low power) - High variability obscures the relationship - Never conclude: “Proved β₂ = 0” or “No relationship exists”

4. Heterogeneity across groups - If β₂(high-income) > β₂(developing): Capital complementary with other factors more abundant in rich countries (technology, institutions, human capital) - If β₂(developing) > β₂(high-income): Diminishing returns to capital more pronounced in capital-abundant countries

Best practices for economic interpretation: 1. Report point estimates, not just significance 2. Use confidence intervals to show uncertainty 3. Assess economic magnitude (not just statistical significance) 4. Consider alternative explanations and limitations 5. Link findings to economic theory and policy implications

Task 5: Visual Analysis (Independent)

Objective: Create visualizations to communicate your statistical inference results effectively.

Your tasks (completely open-ended):

Create a scatter plot showing the productivity-capital relationship:

Include the regression line

Color-code points by income group (high-income vs. developing)

Add 95% confidence bands around the regression line (advanced)

Create a coefficient plot comparing:

Full sample estimate

High-income group estimate

Developing group estimate

Show 95% confidence intervals as error bars

Create a residual plot:

Check for heteroskedasticity visually

Does the spread of residuals increase with fitted values?

Challenge: Can you create a single figure that tells the complete story of your analysis?

# Task 5: Your visualizations here# Figure 1: Scatter plot with regression lines by groupfig, axes = plt.subplots(1, 2, figsize=(14, 6))# Left panel: Full sampleax1 = axes[0]ax1.scatter(data_2014['capital'], data_2014['productivity'], alpha=0.5, s=40, color='#22d3ee', label='All countries')ax1.plot(data_2014['capital'], model_convergence.fittedvalues, color='red', linewidth=2, label='Regression line')ax1.set_xlabel('Capital per Worker ($1000s)')ax1.set_ylabel('Labor Productivity ($1000s)')ax1.set_title('Full Sample Regression')ax1.legend()ax1.grid(True, alpha=0.3)# Right panel: By income groupax2 = axes[1]ax2.scatter(high_income['capital'], high_income['productivity'], alpha=0.5, s=40, color='green', label='High-income')ax2.scatter(developing['capital'], developing['productivity'], alpha=0.5, s=40, color='orange', label='Developing')# Add regression lineshigh_income_sorted = high_income.sort_values('capital')developing_sorted = developing.sort_values('capital')ax2.plot(high_income_sorted['capital'], model_high.predict(high_income_sorted), color='#4ade80', linewidth=2, linestyle='--', label='High-income fit')ax2.plot(developing_sorted['capital'], model_dev.predict(developing_sorted), color='darkorange', linewidth=2, linestyle='--', label='Developing fit')ax2.set_xlabel('Capital per Worker ($1000s)')ax2.set_ylabel('Labor Productivity ($1000s)')ax2.set_title('By Income Group')ax2.legend()ax2.grid(True, alpha=0.3)plt.tight_layout()plt.show()# Figure 2: Coefficient plot with confidence intervalsfig, ax = plt.subplots(figsize=(10, 6))groups = ['Full Sample', 'High-Income', 'Developing']estimates = [beta2_robust, robust_high.params['capital'], robust_dev.params['capital']]ses = [se_beta2_robust, robust_high.bse['capital'], robust_dev.bse['capital']]cis_lower = [e -1.96*se for e, se inzip(estimates, ses)]cis_upper = [e +1.96*se for e, se inzip(estimates, ses)]y_pos =range(len(groups))ax.errorbar(estimates, y_pos, xerr=[[e - l for e, l inzip(estimates, cis_lower)], [u - e for e, u inzip(estimates, cis_upper)]], fmt='o', markersize=10, capsize=8, capthick=2, linewidth=2, color='#22d3ee')ax.set_yticks(y_pos)ax.set_yticklabels(groups)ax.axvline(x=0, color='red', linestyle='--', linewidth=1, alpha=0.5, label='H₀: β₂ = 0')ax.axvline(x=0.5, color='green', linestyle=':', linewidth=1, alpha=0.5, label='Theory: β₂ = 0.5')ax.set_xlabel('Estimated Coefficient (β₂) with 95% CI')ax.set_title('Capital-Productivity Relationship: Point Estimates and Confidence Intervals')ax.legend()ax.grid(True, alpha=0.3, axis='x')plt.tight_layout()plt.show()print("\nFigure interpretation:")print(" - All three estimates are positive and statistically significant")print(" - Confidence intervals exclude zero but include 0.5 (theory prediction)")print(" - High-income countries show slightly stronger relationship")print(" - But confidence intervals overlap, suggesting difference may not be significant")

---------------------------------------------------------------------------NameError Traceback (most recent call last)

Cell In[23], line 8 6# Left panel: Full sample 7 ax1 = axes[0]

----> 8 ax1.scatter(data_2014['capital'], data_2014['productivity'],

9 alpha=0.5, s=40, color='#22d3ee', label='All countries')

10 ax1.plot(data_2014['capital'], model_convergence.fittedvalues,

11 color='red', linewidth=2, label='Regression line')

12 ax1.set_xlabel('Capital per Worker ($1000s)')

NameError: name 'data_2014' is not defined

Task 6: Write a Research Summary (Independent)

Objective: Communicate your statistical findings in a clear, professional manner.

Your task:

Write a 200-300 word summary of your analysis as if for an economics journal. Your summary should include:

Research question - What were you investigating?

Data and methods - What data did you use? What regressions did you run?

Key findings - What did you discover? Report specific numbers (coefficients, CIs, p-values)

Statistical inference - Were effects statistically significant? Did you use robust SEs?

Economic interpretation - What do the results mean economically?

Limitations and extensions - What are the caveats? What should future research explore?

Grading criteria:

Clear and concise writing

Appropriate use of statistical terminology

Correct interpretation of results

Discussion of both statistical and economic significance

Professional tone suitable for academic publication

Example opening:

“Using cross-sectional data for 108 countries in 2014, I investigate the relationship between labor productivity (GDP per capita) and physical capital per worker. The estimated coefficient of 0.XX (robust SE = 0.YY, p < 0.001) indicates that…”

Write your summary in the markdown cell below.

Your Research Summary

(Write your 200-300 word summary here)

[Your text goes here]

What You’ve Learned

Congratulations! You’ve completed a comprehensive statistical inference analysis. You practiced:

Statistical Skills:

Estimating bivariate regression models

Constructing and interpreting 95% confidence intervals

Comparing results across subsamples (heterogeneity analysis)

Creating publication-quality visualizations

Writing professional research summaries

Economic Insights:

Understanding the productivity-capital relationship across countries

Testing economic theory predictions with data

Interpreting coefficients in economic terms (marginal products)

Recognizing heterogeneity across country income groups

Distinguishing statistical from economic significance

Practical Skills:

Using Python for comprehensive econometric analysis

Generating robust standard errors with statsmodels

Creating compelling visualizations with matplotlib

Communicating statistical results to non-technical audiences

Next Steps:

Chapter 8 will extend these methods to multiple regression

You’ll learn how to control for confounding variables

And test joint hypotheses about multiple coefficients

Key Takeaway: Statistical inference transforms sample estimates into insights about populations. By constructing confidence intervals and testing hypotheses, you move beyond “What did we find in our data?” to “What can we confidently say about the world?” This is the foundation of evidence-based economics.

Case Study 2: Is the Light-Development Relationship Significant?

In Chapter 1, we introduced the DS4Bolivia project and estimated a simple regression of municipal development (IMDS) on nighttime lights (NTL). In Chapter 5, we explored bivariate relationships in depth. Now we apply Chapter 7’s inference tools to test whether the NTL-development relationship is statistically significant and construct confidence intervals for the effect.

Research Question: Is the association between nighttime lights and municipal development statistically significant, and how precisely can we estimate the effect?

Data: Cross-sectional dataset covering 339 Bolivian municipalities from the DS4Bolivia Project.

Key Variables:

imds: Municipal Sustainable Development Index (0-100)

ln_NTLpc2017: Log nighttime lights per capita (2017)

mun: Municipality name

dep: Department (administrative region)

Load the DS4Bolivia Data

Load the DS4Bolivia dataset and prepare the regression sample.

======================================================================

DS4BOLIVIA DATASET — REGRESSION SAMPLE

======================================================================

Total municipalities: 339

Complete cases for regression: 333

Descriptive statistics:

imds ln_NTLpc2017

count 333.000 333.000

mean 51.158 13.880

std 6.760 1.181

min 35.700 9.064

25% 47.100 13.134

50% 50.800 13.914

75% 55.000 14.774

max 80.200 17.064

Task 1: Estimate and Test Slope (Guided)

Objective: Estimate the OLS regression of IMDS on log NTL per capita and test whether the slope is statistically significant.

Instructions:

Estimate the regression imds ~ ln_NTLpc2017 using OLS

Display the full regression summary

Extract the t-statistic and p-value for the slope coefficient

Test the null hypothesis H₀: β₁ = 0 (no linear relationship)

State your conclusion: Can we reject the null at the 5% significance level?