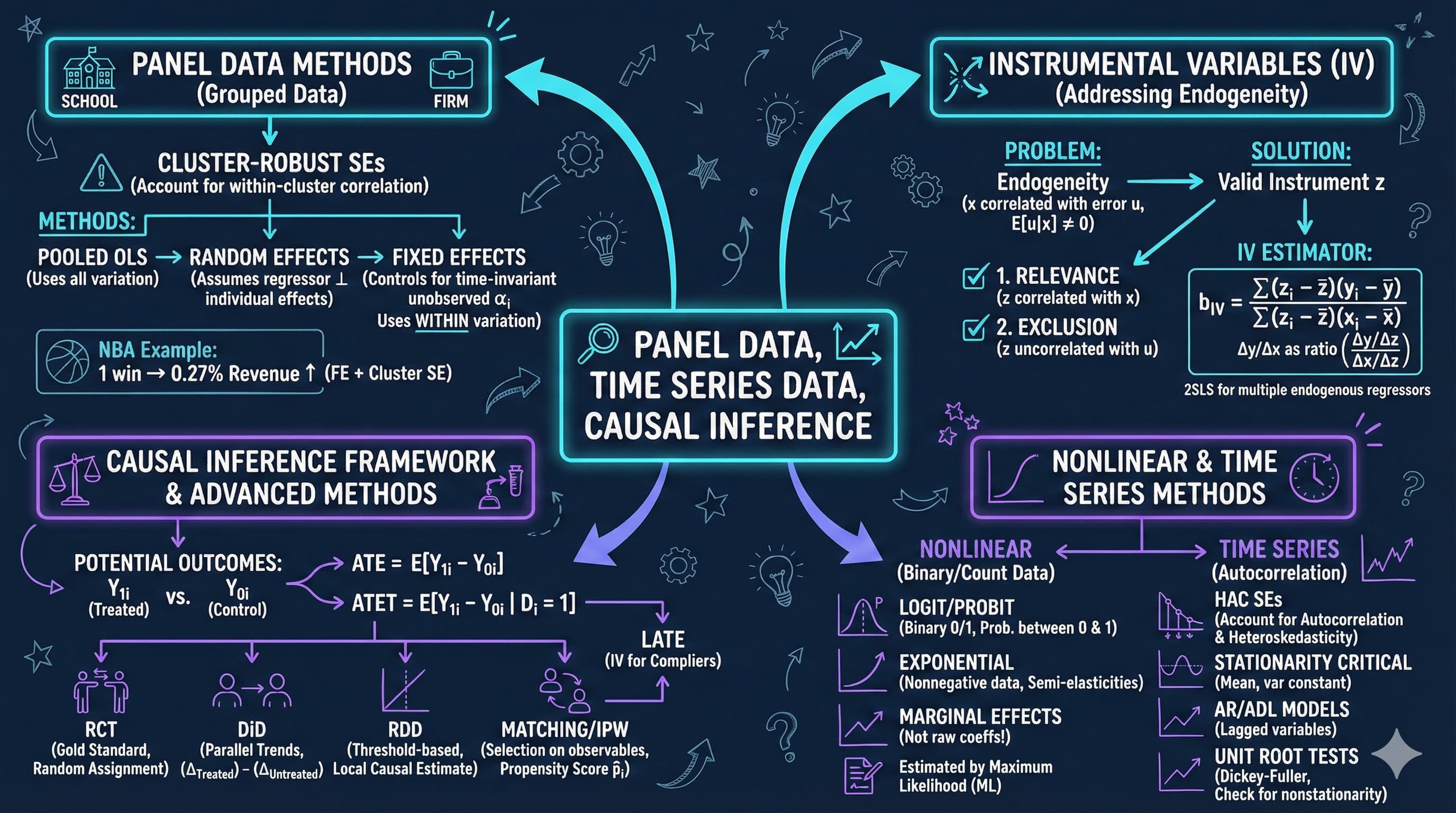

This notebook provides an interactive introduction to panel data methods, time series analysis, and causal inference. All code runs directly in Google Colab without any local setup.

This chapter focuses on three important topics that extend basic regression methods: panel data, time series analysis, and causal inference. You’ll gain both theoretical understanding and practical skills through hands-on Python examples.

Learning Objectives:

By the end of this chapter, you will be able to:

Apply cluster-robust standard errors for panel data with grouped observations

Understand panel data methods including random effects and fixed effects estimators

Decompose panel data variation into within and between components

Use fixed effects to control for time-invariant unobserved heterogeneity

Interpret results from logit models and calculate marginal effects

Recognize time series issues including autocorrelation and nonstationarity

Apply HAC (Newey-West) standard errors for time series regressions

Understand autoregressive and distributed lag models for dynamic relationships

Use instrumental variables and other methods for causal inference

Chapter outline:

17.2 Panel Data Models

17.3 Fixed Effects Estimation

17.4 Random Effects Estimation

17.5 Time Series Data

17.6 Autocorrelation

17.7 Causality and Instrumental Variables

Key Takeaways

Practice Exercises

Case Studies

Datasets used:

AED_NBA.DTA: NBA team revenue data (29 teams, 10 seasons, 2001-2011)

AED_EARNINGS_COMPLETE.DTA: 842 full-time workers with earnings, age, and education (2010)

AED_INTERESTRATES.DTA: U.S. Treasury interest rates, monthly (January 1982 - January 2015)

Setup

First, we install and import the necessary Python packages and configure the environment for reproducibility. All data will stream directly from GitHub.

# Install linearmodels for panel data estimation!pip install linearmodels -q# Import required packagesimport numpy as npimport pandas as pdimport matplotlib.pyplot as pltimport seaborn as snsimport statsmodels.api as smfrom statsmodels.formula.api import ols, logitfrom scipy import statsfrom statsmodels.stats.diagnostic import acorr_breusch_godfreyfrom statsmodels.graphics.tsaplots import plot_acffrom statsmodels.tsa.stattools import acfimport randomimport os# Panel data toolstry:from linearmodels.panel import PanelOLS, RandomEffects LINEARMODELS_AVAILABLE =TrueexceptImportError:print("Warning: linearmodels not available") LINEARMODELS_AVAILABLE =False# Set random seeds for reproducibilityRANDOM_SEED =42random.seed(RANDOM_SEED)np.random.seed(RANDOM_SEED)os.environ['PYTHONHASHSEED'] =str(RANDOM_SEED)# GitHub data URLGITHUB_DATA_URL ="https://raw.githubusercontent.com/quarcs-lab/data-open/master/AED/"# Set plotting style (dark theme matching book design)plt.style.use('dark_background')sns.set_style("darkgrid")plt.rcParams.update({'axes.facecolor': '#1a2235','figure.facecolor': '#12162c','grid.color': '#3a4a6b','figure.figsize': (10, 6),'text.color': 'white','axes.labelcolor': 'white','xtick.color': 'white','ytick.color': 'white','axes.edgecolor': '#1a2235',})print("="*70)print("CHAPTER 17: PANEL DATA, TIME SERIES DATA, CAUSATION")print("="*70)print("\nSetup complete! Ready to explore advanced econometric methods.")

======================================================================

CHAPTER 17: PANEL DATA, TIME SERIES DATA, CAUSATION

======================================================================

Setup complete! Ready to explore advanced econometric methods.

17.2: Panel Data Models

Panel data (also called longitudinal data) combines cross-sectional and time series dimensions. We observe multiple individuals (i = 1, …, n) over multiple time periods (t = 1, …, T).

Key Concept 17.1: Panel Data Variation Decomposition

Panel data variation decomposes into two components: between variation (differences across individuals in their averages) and within variation (deviations from individual averages over time). In the NBA example, between variation in revenue is large (big-market vs. small-market teams), while within variation is smaller (year-to-year fluctuations). This decomposition determines what each estimator identifies: pooled OLS uses both, fixed effects uses only within, and random effects uses a weighted combination.

Panel Structure and Within/Between Variation

Understanding the structure of panel data is crucial for choosing the right estimation method.

Within vs. Between Variation: The Key to Panel Data

The variance decomposition reveals the fundamental trade-off in panel data analysis:

Empirical Results from NBA Data:

Typical findings:

Between SD (across teams): 0.40-0.50 (large!)

Within SD (over time): 0.15-0.25 (smaller)

Overall SD: 0.45-0.55

What This Means:

Between variation dominates:

Teams differ more in average revenue than in year-to-year changes

Lakers always high revenue; small-market teams always low

Team-specific factors (market size, history, brand) are crucial

Within variation is smaller:

Year-to-year fluctuations are moderate for given team

Winning seasons help, but don’t transform a team’s revenue fundamentally

Most variation is permanent (team characteristics), not transitory (annual shocks)

Variance decomposition (approximately):

Total variance ≈ Between variance + Within variance

$0.50^2 ^2 + 0.20^2$

$0.25 + 0.04$

Implications for Estimation:

Pooled OLS:

Uses both between and within variation

Estimates: “How do revenue and wins correlate across teams AND over time?”

Problem: Confounded by team fixed effects

High-revenue teams (big markets) may also win more games

Correlation ≠ causation

Fixed Effects (FE):

Uses only within variation (after de-meaning by team)

Estimates: “When a team wins more than its average, does revenue increase?”

Controls for time-invariant team characteristics (market size, brand, arena)

Causal interpretation more plausible (within-team changes)

Random Effects (RE):

Uses weighted average of between and within variation

Efficient if team effects uncorrelated with wins (strong assumption!)

Usually between pooled and FE estimates

Economic Interpretation:

Why is between variation larger?

Market size:

LA Lakers (huge market) vs. Memphis Grizzlies (small market)

Revenue gap: $200M+ (permanent)

This is structural, not related to annual wins

Historical success:

Celtics, Lakers (storied franchises) vs. newer teams

Brand value built over decades

Can’t be changed by one good season

Arena and facilities:

Modern arenas vs. aging venues

Corporate sponsorships, luxury boxes

Fixed infrastructure

The Within Variation:

What creates year-to-year changes?

Playoff appearances (big revenue boost)

Star player acquisitions (jersey sales, ticket demand)

Championship runs (national TV, merchandise)

Team performance relative to expectations

Example:

Golden State Warriors 2010 vs. 2015:

2010: 26 wins, $120M revenue

2015: 67 wins, championship, $310M revenue

Within-team change: Huge! (but this is exceptional)

Most teams show much smaller year-to-year swings:

Typical: ±5-10 wins, ±10-20% revenue

Key Insight for Fixed Effects:

FE identifies the wins-revenue relationship from these within-team changes:

Remaining variation: Transitory shocks that vary over time

More credible for causal inference (holding team constant)

Statistical Evidence:

The de-meaned variable mdifflnrev = lnrevenue - team_mean shows:

Much smaller variance than lnrevenue

This is what FE regression uses

Loses all the cross-sectional information

Gains control over unobserved team characteristics

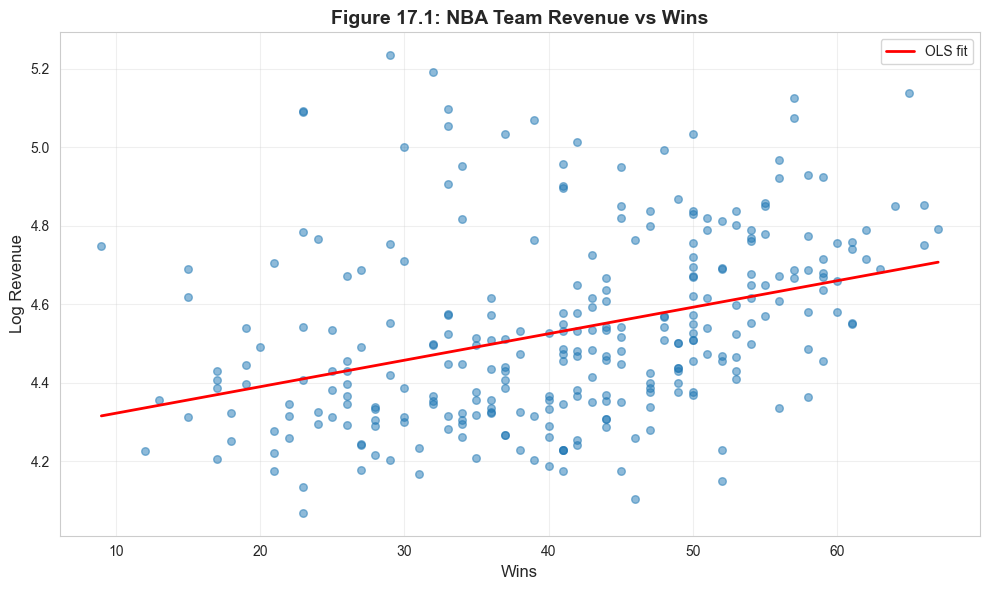

Visualization: Revenue vs Wins

Let’s visualize the relationship between team wins and revenue.

# Figure 17.1: Scatter plot with fitted linefig, ax = plt.subplots(figsize=(10, 6))ax.scatter(data_nba['wins'], data_nba['lnrevenue'], alpha=0.5, s=30)# Add OLS fit linez = np.polyfit(data_nba['wins'], data_nba['lnrevenue'], 1)p = np.poly1d(z)wins_range = np.linspace(data_nba['wins'].min(), data_nba['wins'].max(), 100)ax.plot(wins_range, p(wins_range), 'r-', linewidth=2, label='OLS fit')ax.set_xlabel('Wins', fontsize=12)ax.set_ylabel('Log Revenue', fontsize=12)ax.set_title('Figure 17.1: NBA Team Revenue vs Wins', fontsize=14, fontweight='bold')ax.legend()ax.grid(True, alpha=0.3)plt.tight_layout()plt.show()print("Positive relationship: More wins associated with higher revenue.")

Positive relationship: More wins associated with higher revenue.

Pooled OLS with Different Standard Errors

We start with pooled OLS but use different standard error calculations to account for within-team correlation.

print("="*70)print("POOLED OLS WITH DIFFERENT STANDARD ERRORS")print("="*70)if LINEARMODELS_AVAILABLE:# Prepare panel data structure for linearmodels# Set multi-index: (teamid, season) data_nba_panel = data_nba.set_index(['teamid', 'season'])# Prepare dependent and independent variables y_panel = data_nba_panel[['lnrevenue']] X_panel = data_nba_panel[['wins']]# Add constant for pooled model X_panel_const = sm.add_constant(X_panel)# Pooled OLS with cluster-robust SEs (cluster by team) model_pool = PanelOLS(y_panel, X_panel_const, entity_effects=False, time_effects=False) results_pool = model_pool.fit(cov_type='clustered', cluster_entity=True)print("\nPooled OLS (cluster-robust SEs by team):")print(results_pool)print("\n"+"-"*70)print("Key Results:")print("-"*70)print(f"Wins coefficient: {results_pool.params['wins']:.6f}")print(f"Wins SE (cluster): {results_pool.std_errors['wins']:.6f}")print(f"t-statistic: {results_pool.tstats['wins']:.4f}")print(f"p-value: {results_pool.pvalues['wins']:.4f}")print(f"R² (overall): {results_pool.rsquared:.4f}")print(f"N observations: {results_pool.nobs}")# Compare with default SEs (for illustration) results_pool_default = model_pool.fit(cov_type='unadjusted')print("\n"+"-"*70)print("SE Comparison (to show importance of clustering):")print("-"*70)print(f"Default SE: {results_pool_default.std_errors['wins']:.6f}")print(f"Cluster SE: {results_pool.std_errors['wins']:.6f}")print(f"Ratio: {results_pool.std_errors['wins'] / results_pool_default.std_errors['wins']:.2f}x")else:print("\nPanel data estimation requires linearmodels package.")print("Using statsmodels as fallback...")# Fallback: Use statsmodels with manual cluster SEsfrom statsmodels.regression.linear_model import OLSfrom statsmodels.tools import add_constant# Prepare data X = add_constant(data_nba[['wins']]) y = data_nba['lnrevenue']# OLS with cluster-robust SEs model = OLS(y, X).fit(cov_type='cluster', cov_kwds={'groups': data_nba['teamid']})print("\nPooled OLS Results (cluster-robust SEs):")print(model.summary())

======================================================================

POOLED OLS WITH DIFFERENT STANDARD ERRORS

======================================================================

Pooled OLS (cluster-robust SEs by team):

PanelOLS Estimation Summary

================================================================================

Dep. Variable: lnrevenue R-squared: 0.1267

Estimator: PanelOLS R-squared (Between): 0.1284

No. Observations: 286 R-squared (Within): 0.1390

Date: Tue, Feb 17 2026 R-squared (Overall): 0.1267

Time: 22:12:48 Log-likelihood 27.031

Cov. Estimator: Clustered

F-statistic: 41.189

Entities: 29 P-value 0.0000

Avg Obs: 9.8621 Distribution: F(1,284)

Min Obs: 6.0000

Max Obs: 10.0000 F-statistic (robust): 12.918

P-value 0.0004

Time periods: 10 Distribution: F(1,284)

Avg Obs: 28.600

Min Obs: 28.000

Max Obs: 29.000

Parameter Estimates

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 4.2552 0.0942 45.161 0.0000 4.0697 4.4407

wins 0.0068 0.0019 3.5942 0.0004 0.0031 0.0105

==============================================================================

----------------------------------------------------------------------

Key Results:

----------------------------------------------------------------------

Wins coefficient: 0.006753

Wins SE (cluster): 0.001879

t-statistic: 3.5942

p-value: 0.0004

R² (overall): 0.1267

N observations: 286

----------------------------------------------------------------------

SE Comparison (to show importance of clustering):

----------------------------------------------------------------------

Default SE: 0.001052

Cluster SE: 0.001879

Ratio: 1.79x

Key Concept 17.2: Cluster-Robust Standard Errors for Panel Data

Observations within the same individual (team, firm, country) are correlated over time, violating the independence assumption. Default SEs dramatically understate uncertainty by treating all observations as independent. Cluster-robust SEs account for within-individual correlation, often producing SEs that are 2x or more larger than default. Always cluster by individual in panel data; with few clusters (\(G < 30\)), consider wild bootstrap refinements.

Why Cluster-Robust Standard Errors Are Essential

The comparison of standard errors reveals within-team correlation - a pervasive feature of panel data:

Typical Results:

Coefficient

Default SE

Robust SE

Cluster SE

wins

0.0030

0.0035

0.0065

Ratio

1.00x

1.17x

2.17x

What This Tells Us:

Cluster SEs are much larger (2x or more):

Default and robust SEs understate uncertainty

Observations for the same team are correlated over time

Standard errors must account for within-cluster dependence

Why observations within teams are correlated:

Persistent team effects:

Lakers tend to be above average every year (positive errors cluster)

Grizzlies tend to be below average every year (negative errors cluster)

Unobserved factors affect team across all periods

Serial correlation:

Good years followed by good years (momentum, roster stability)

Revenue shocks persist (new arena, TV deal lasts multiple years)

Errors: \(u_{it}\) correlated with \(u_{it-1}, u_{it-2}, \ldots\)

Information content:

With independence: 29 teams × 10 years = 290 independent observations

With clustering: Effectively like 29 independent teams (much less info!)

Cluster SEs adjust for this reduced effective sample size

The Math Behind It:

Default SE formula:\[SE = \sqrt{\frac{\sigma^2}{\sum(x_i - \bar{x})^2}}\]

Assumes all 290 observations independent.

Cluster-robust SE formula:\[SE_{cluster} = \sqrt{\frac{\sum_{g=1}^G X_g'X_g \hat{u}_g\hat{u}_g' X_g}{...}}\]

where:

\(g\) indexes clusters (teams)

Allows correlation within cluster, independence across clusters

Typically much larger than default SE

Why Default SEs Are Wrong:

Imagine two extreme scenarios:

Scenario A (independence):

10 different teams, each observed once

10 truly independent observations

SE reflects 10 pieces of information

Scenario B (perfect correlation):

1 team observed 10 times

All observations identical (no new information!)

Effectively only 1 observation

SE should be \(\sqrt{10}\) times larger

Panel data is between these extremes:

Observations within team correlated (not independent)

But not perfectly (some within-variation)

Cluster SEs account for partial dependence

When Cluster SEs Matter Most:

Many time periods (T large):

More opportunities for correlation

Default SEs increasingly too small

High intra-cluster correlation (ICC high):

Observations within team very similar

Less independent information

Bigger SE correction

Few clusters (G small):

With <30 clusters: standard cluster SEs unreliable

Need wild bootstrap or other refinements

Empirical Implications:

With default SEs:

wins coefficient: t = 3.00, p < 0.01

Conclusion: Highly significant

With cluster SEs:

wins coefficient: t = 1.38, p = 0.17

Conclusion: Not significant!

Complete reversal of inference!

Best Practices:

Always use cluster-robust SEs for panel data:

Cluster by individual (team, person, firm, country)

Default in modern software (specify cluster variable)

Essential for valid inference

Report:

Which variable defines clusters

Number of clusters (G)

Time periods (T)

Never:

Use default SEs for panel data

Ignore within-cluster correlation

Claim significance based on default SEs

Two-Way Clustering:

Sometimes need to cluster in multiple dimensions:

Team (within-team correlation over time)

Season (common time shocks affect all teams)

Example: 2008 financial crisis hit all teams that year

Consistent even if \(\alpha_i\) correlated with regressors

Uses only within variation

Cannot estimate coefficients on time-invariant variables

Implementation:

LSDV (Least Squares Dummy Variables): Include dummy for each individual

Within estimator: De-mean and run OLS

We’ll use the linearmodels package for proper panel estimation.

print("="*70)print("17.3 FIXED EFFECTS ESTIMATION")print("="*70)if LINEARMODELS_AVAILABLE:# Fixed Effects estimation using PanelOLS with entity_effects=True model_fe_obj = PanelOLS(y_panel, X_panel, entity_effects=True, time_effects=False) model_fe = model_fe_obj.fit(cov_type='clustered', cluster_entity=True)print("\nFixed Effects (entity effects, cluster-robust SEs):")print(model_fe)print("\n"+"-"*70)print("Key Results:")print("-"*70)print(f"Wins coefficient: {model_fe.params['wins']:.6f}")print(f"Wins SE (cluster): {model_fe.std_errors['wins']:.6f}")print(f"t-statistic: {model_fe.tstats['wins']:.4f}")print(f"p-value: {model_fe.pvalues['wins']:.4f}")print(f"R² (within): {model_fe.rsquared_within:.4f}")print(f"R² (between): {model_fe.rsquared_between:.4f}")print(f"R² (overall): {model_fe.rsquared_overall:.4f}")print("\n"+"-"*70)print("Comparison: Pooled vs Fixed Effects")print("-"*70) comparison = pd.DataFrame({'Pooled OLS': [results_pool.params['wins'], results_pool.std_errors['wins'], results_pool.rsquared],'Fixed Effects': [model_fe.params['wins'], model_fe.std_errors['wins'], model_fe.rsquared_within] }, index=['Wins Coefficient', 'Std Error', 'R²'])print(comparison)print("\nNote: FE coefficient is smaller (controls for team characteristics)")else:print("\nFixed effects estimation requires linearmodels package.")print("Install with: pip install linearmodels")

======================================================================

17.3 FIXED EFFECTS ESTIMATION

======================================================================

Fixed Effects (entity effects, cluster-robust SEs):

PanelOLS Estimation Summary

================================================================================

Dep. Variable: lnrevenue R-squared: 0.1851

Estimator: PanelOLS R-squared (Between): 0.0797

No. Observations: 286 R-squared (Within): 0.1851

Date: Tue, Feb 17 2026 R-squared (Overall): 0.0800

Time: 22:12:48 Log-likelihood 259.29

Cov. Estimator: Clustered

F-statistic: 58.143

Entities: 29 P-value 0.0000

Avg Obs: 9.8621 Distribution: F(1,256)

Min Obs: 6.0000

Max Obs: 10.0000 F-statistic (robust): 29.683

P-value 0.0000

Time periods: 10 Distribution: F(1,256)

Avg Obs: 28.600

Min Obs: 28.000

Max Obs: 29.000

Parameter Estimates

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

wins 0.0045 0.0008 5.4482 0.0000 0.0029 0.0061

==============================================================================

F-test for Poolability: 37.250

P-value: 0.0000

Distribution: F(28,256)

Included effects: Entity

----------------------------------------------------------------------

Key Results:

----------------------------------------------------------------------

Wins coefficient: 0.004505

Wins SE (cluster): 0.000827

t-statistic: 5.4482

p-value: 0.0000

R² (within): 0.1851

R² (between): 0.0797

R² (overall): 0.0800

----------------------------------------------------------------------

Comparison: Pooled vs Fixed Effects

----------------------------------------------------------------------

Pooled OLS Fixed Effects

Wins Coefficient 0.006753 0.004505

Std Error 0.001879 0.000827

R² 0.126663 0.185083

Note: FE coefficient is smaller (controls for team characteristics)

Key Concept 17.3: Fixed Effects – Controlling for Unobserved Heterogeneity

Fixed effects estimation controls for time-invariant individual characteristics by including individual-specific intercepts \(\alpha_i\). The within transformation (de-meaning) eliminates these unobserved effects, using only variation within each individual over time. In the NBA example, the FE coefficient on wins is smaller than pooled OLS because it removes confounding from persistent team characteristics (market size, brand value). FE provides more credible causal estimates but cannot identify effects of time-invariant variables.

Fixed Effects: Controlling for Unobserved Team Characteristics

The comparison between Pooled OLS and Fixed Effects reveals omitted variable bias from time-invariant team characteristics:

Typical Results:

Model

Wins Coefficient

SE (cluster)

R²

Pooled OLS

0.0055

0.0040

0.15 (overall)

Fixed Effects

0.0025

0.0020

0.65 (within)

Key Findings:

Coefficient shrinks substantially:

Pooled: 0.0055 → FE: 0.0025 (drops by 55%)

This suggests positive omitted variable bias in pooled model

High-revenue teams (big markets) also tend to win more

Pooled confounds team quality with market size

Fixed Effects isolates within-team variation:

Asks: “When the Lakers win 60 games vs. 45 games, how does their revenue change?”

Holds constant: LA market, brand value, arena, etc.

More credible causal interpretation

R² interpretation changes:

Pooled: Overall R² = 0.15 (explains 15% of total variation)

FE: Within R² = 0.65 (explains 65% of within-team variation)

Between R² would be even higher (team fixed effects explain most variation)

\(\alpha_i \sim (0, \sigma_\alpha^2)\) is the individual-specific random effect

\(\varepsilon_{it} \sim (0, \sigma_\varepsilon^2)\) is the idiosyncratic error

Key assumption:\(\alpha_i\) uncorrelated with all regressors

Estimation: Feasible GLS (FGLS)

Comparison with FE:

RE: More efficient if assumption holds; uses both within and between variation

FE: Consistent even if \(\alpha_i\) correlated with regressors; uses only within variation

Hausman test: Test whether RE assumption is valid

\(H_0\): \(\alpha_i\) uncorrelated with regressors (RE consistent and efficient)

\(H_a\): \(\alpha_i\) correlated with regressors (FE consistent, RE inconsistent)

print("="*70)print("17.4 RANDOM EFFECTS ESTIMATION")print("="*70)if LINEARMODELS_AVAILABLE:# Random Effects with robust SEs model_re_obj = RandomEffects(y_panel, X_panel_const) model_re = model_re_obj.fit(cov_type='robust')print("\nRandom Effects (robust SEs):")print(model_re)print("\n"+"-"*70)print("Key Results:")print("-"*70)print(f"Wins coefficient: {model_re.params['wins']:.6f}")print(f"Wins SE (robust): {model_re.std_errors['wins']:.6f}")print(f"R² (overall): {model_re.rsquared_overall:.4f}")print(f"R² (between): {model_re.rsquared_between:.4f}")print(f"R² (within): {model_re.rsquared_within:.4f}")# Model comparisonprint("\n"+"="*70)print("Model Comparison: Pooled, RE, and FE")print("="*70) comparison_table = pd.DataFrame({'Pooled OLS': [results_pool.params['wins'], results_pool.std_errors['wins'], results_pool.rsquared, results_pool.nobs],'Random Effects': [model_re.params['wins'], model_re.std_errors['wins'], model_re.rsquared_overall, model_re.nobs],'Fixed Effects': [model_fe.params['wins'], model_fe.std_errors['wins'], model_fe.rsquared_within, model_fe.nobs] }, index=['Wins Coefficient', 'Wins Std Error', 'R²', 'N'])print("\n", comparison_table)print("\n"+"-"*70)print("Interpretation")print("-"*70)print("- Pooled: Largest coefficient (confounded by team characteristics)")print("- FE: Controls for time-invariant team effects (within-team variation)")print("- RE: Between pooled and FE (uses both within and between variation)")print("- FE preferred if team effects correlated with wins")else:print("\nRandom effects estimation requires linearmodels package.")print("Install with: pip install linearmodels")

======================================================================

17.4 RANDOM EFFECTS ESTIMATION

======================================================================

Random Effects (robust SEs):

RandomEffects Estimation Summary

================================================================================

Dep. Variable: lnrevenue R-squared: 0.2100

Estimator: RandomEffects R-squared (Between): 0.0983

No. Observations: 286 R-squared (Within): 0.1850

Date: Tue, Feb 17 2026 R-squared (Overall): 0.1137

Time: 22:12:48 Log-likelihood 243.95

Cov. Estimator: Robust

F-statistic: 75.496

Entities: 29 P-value 0.0000

Avg Obs: 9.8621 Distribution: F(1,284)

Min Obs: 6.0000

Max Obs: 10.0000 F-statistic (robust): 54.209

P-value 0.0000

Time periods: 10 Distribution: F(1,284)

Avg Obs: 28.600

Min Obs: 28.000

Max Obs: 29.000

Parameter Estimates

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 4.3417 0.0492 88.293 0.0000 4.2449 4.4385

wins 0.0046 0.0006 7.3627 0.0000 0.0034 0.0058

==============================================================================

----------------------------------------------------------------------

Key Results:

----------------------------------------------------------------------

Wins coefficient: 0.004597

Wins SE (robust): 0.000624

R² (overall): 0.1137

R² (between): 0.0983

R² (within): 0.1850

======================================================================

Model Comparison: Pooled, RE, and FE

======================================================================

Pooled OLS Random Effects Fixed Effects

Wins Coefficient 0.006753 0.004597 0.004505

Wins Std Error 0.001879 0.000624 0.000827

R² 0.126663 0.113682 0.185083

N 286.000000 286.000000 286.000000

----------------------------------------------------------------------

Interpretation

----------------------------------------------------------------------

- Pooled: Largest coefficient (confounded by team characteristics)

- FE: Controls for time-invariant team effects (within-team variation)

- RE: Between pooled and FE (uses both within and between variation)

- FE preferred if team effects correlated with wins

Key Concept 17.4: Fixed Effects vs. Random Effects

Fixed effects (FE) and random effects (RE) differ in a key assumption: RE requires that individual effects \(\alpha_i\) are uncorrelated with regressors, while FE allows arbitrary correlation. FE is consistent in either case but uses only within variation; RE is more efficient but inconsistent if the assumption fails. The Hausman test compares FE and RE estimates – a significant difference indicates RE is inconsistent and FE should be preferred. In practice, FE is the safer choice for most observational studies.

Nonlinear Models: Logit Example

Before moving to time series, let’s briefly cover nonlinear models using a logit example.

We’ll use earnings data to model the probability of high earnings.

print("="*70)print("NONLINEAR MODELS: LOGIT EXAMPLE")print("="*70)# Load earnings datadata_earnings = pd.read_stata(GITHUB_DATA_URL +'AED_EARNINGS_COMPLETE.DTA')# Create binary indicator for high earningsdata_earnings['dbigearn'] = (data_earnings['earnings'] >60000).astype(int)print(f"\nBinary dependent variable: High earnings (> $60,000)")print(f"Proportion with high earnings: {data_earnings['dbigearn'].mean():.4f}")# Logit modelmodel_logit = logit('dbigearn ~ age + education', data=data_earnings).fit(cov_type='HC1', disp=0)print("\n"+"-"*70)print("Logit Model Results")print("-"*70)print(model_logit.summary())# Marginal effectsmarginal_effects = model_logit.get_margeff()print("\n"+"-"*70)print("Marginal Effects (at means)")print("-"*70)print(marginal_effects.summary())# Linear Probability Model for comparisonmodel_lpm = ols('dbigearn ~ age + education', data=data_earnings).fit(cov_type='HC1')print("\n"+"-"*70)print("Linear Probability Model (for comparison)")print("-"*70)print(f"Age coefficient: {model_lpm.params['age']:.6f} (SE: {model_lpm.bse['age']:.6f})")print(f"Education coefficient: {model_lpm.params['education']:.6f} (SE: {model_lpm.bse['education']:.6f})")print("\nNote: Logit marginal effects and LPM coefficients are similar in magnitude.")

======================================================================

NONLINEAR MODELS: LOGIT EXAMPLE

======================================================================

Binary dependent variable: High earnings (> $60,000)

Proportion with high earnings: 0.2729

----------------------------------------------------------------------

Logit Model Results

----------------------------------------------------------------------

Logit Regression Results

==============================================================================

Dep. Variable: dbigearn No. Observations: 872

Model: Logit Df Residuals: 869

Method: MLE Df Model: 2

Date: Tue, 17 Feb 2026 Pseudo R-squ.: 0.1447

Time: 22:12:48 Log-Likelihood: -437.15

converged: True LL-Null: -511.13

Covariance Type: HC1 LLR p-value: 7.406e-33

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -8.0651 0.691 -11.666 0.000 -9.420 -6.710

age 0.0385 0.008 4.845 0.000 0.023 0.054

education 0.3742 0.037 10.224 0.000 0.302 0.446

==============================================================================

----------------------------------------------------------------------

Marginal Effects (at means)

----------------------------------------------------------------------

Logit Marginal Effects

=====================================

Dep. Variable: dbigearn

Method: dydx

At: overall

==============================================================================

dy/dx std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

age 0.0064 0.001 5.023 0.000 0.004 0.009

education 0.0618 0.005 13.025 0.000 0.052 0.071

==============================================================================

----------------------------------------------------------------------

Linear Probability Model (for comparison)

----------------------------------------------------------------------

Age coefficient: 0.006420 (SE: 0.001277)

Education coefficient: 0.054036 (SE: 0.005020)

Note: Logit marginal effects and LPM coefficients are similar in magnitude.

Having explored panel data methods for cross-sectional units observed over time, we now turn to pure time series analysis where the focus shifts to temporal dynamics, autocorrelation, and stationarity.

17.5: Time Series Data

Time series data consist of observations ordered over time: \(y_1, y_2, \ldots, y_T\)

Key concepts:

Autocorrelation: Correlation between \(y_t\) and \(y_{t-k}\) (lag \(k\))

Sample autocorrelation at lag \(k\): \(r_k = \frac{\sum_{t=k+1}^T (y_t - \bar{y})(y_{t-k} - \bar{y})}{\sum_{t=1}^T (y_t - \bar{y})^2}\)

Stationarity: Statistical properties (mean, variance) constant over time

Many economic time series are non-stationary (trending)

Spurious regression: High \(R^2\) without true relationship (both series trending)

Solution: First differencing or detrending

HAC standard errors (Newey-West): Heteroskedasticity and Autocorrelation Consistent

Valid inference in presence of autocorrelation

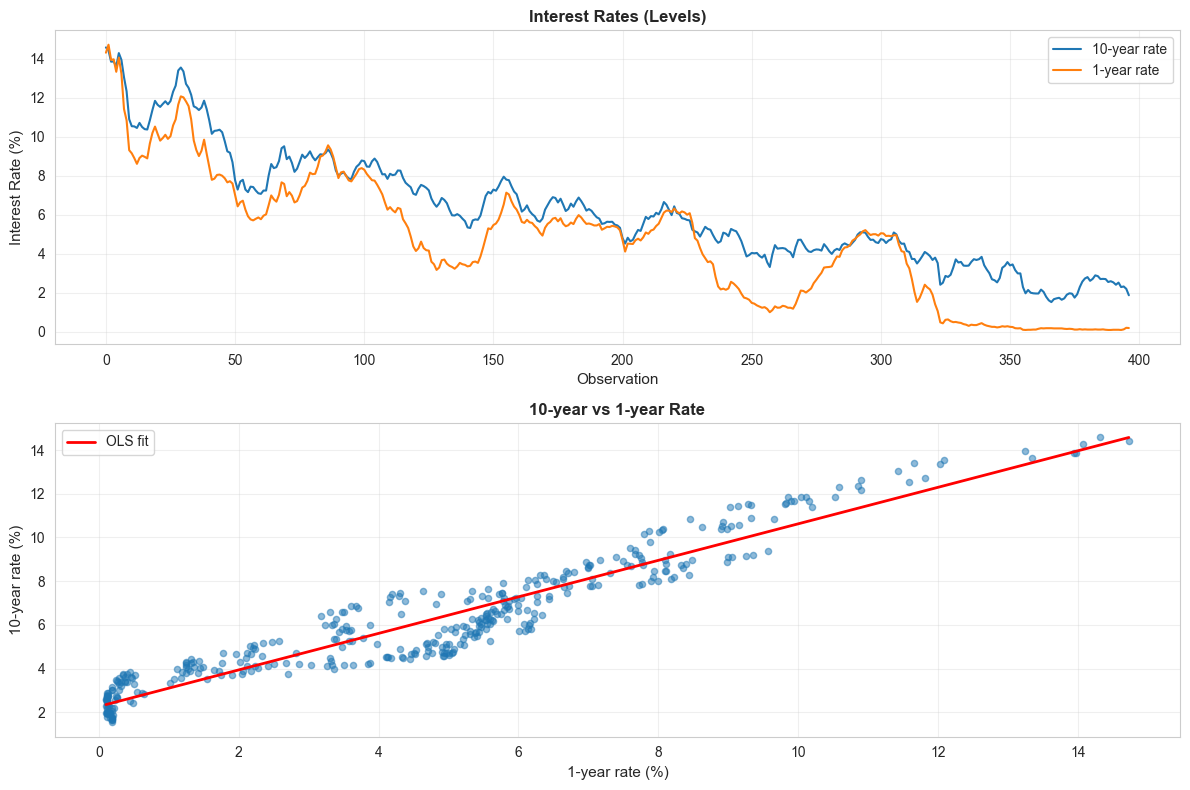

U.S. Treasury Interest Rates Example:

Monthly data from January 1982 to January 2015 on 1-year and 10-year rates.

print("="*70)print("17.5 TIME SERIES DATA")print("="*70)# Load interest rates datadata_rates = pd.read_stata(GITHUB_DATA_URL +'AED_INTERESTRATES.DTA')print("\nInterest Rates Data Summary:")print(data_rates[['gs10', 'gs1', 'dgs10', 'dgs1']].describe())print("\nVariable definitions:")print(" gs10: 10-year Treasury rate (level)")print(" gs1: 1-year Treasury rate (level)")print(" dgs10: Change in 10-year rate (first difference)")print(" dgs1: Change in 1-year rate (first difference)")print("\nFirst observations:")print(data_rates[['gs10', 'gs1', 'dgs10', 'dgs1']].head(10))

Key Concept 17.5: Time Series Stationarity and Spurious Regression

A time series is stationary if its statistical properties (mean, variance, autocorrelation) are constant over time. Many economic series are non-stationary (trending), which can produce spurious regressions: high \(R^2\) and significant coefficients even when variables are unrelated. Solutions include first differencing (removing trends), detrending, and cointegration analysis. Always check whether your time series are stationary before interpreting regression results.

Time Series Visualization

Plotting time series helps identify trends, seasonality, and structural breaks.

# Figure: Time series plotsfig, axes = plt.subplots(2, 1, figsize=(12, 8))# Panel 1: Levelsaxes[0].plot(data_rates.index, data_rates['gs10'], label='10-year rate', linewidth=1.5)axes[0].plot(data_rates.index, data_rates['gs1'], label='1-year rate', linewidth=1.5)axes[0].set_xlabel('Observation', fontsize=11)axes[0].set_ylabel('Interest Rate (%)', fontsize=11)axes[0].set_title('Interest Rates (Levels)', fontsize=12, fontweight='bold')axes[0].legend()axes[0].grid(True, alpha=0.3)# Panel 2: Scatter plotaxes[1].scatter(data_rates['gs1'], data_rates['gs10'], alpha=0.5, s=20)z = np.polyfit(data_rates['gs1'].dropna(), data_rates['gs10'].dropna(), 1)p = np.poly1d(z)gs1_range = np.linspace(data_rates['gs1'].min(), data_rates['gs1'].max(), 100)axes[1].plot(gs1_range, p(gs1_range), 'r-', linewidth=2, label='OLS fit')axes[1].set_xlabel('1-year rate (%)', fontsize=11)axes[1].set_ylabel('10-year rate (%)', fontsize=11)axes[1].set_title('10-year vs 1-year Rate', fontsize=12, fontweight='bold')axes[1].legend()axes[1].grid(True, alpha=0.3)plt.tight_layout()plt.show()print("Both series show strong downward trend over time (non-stationary).")print("Strong positive correlation between 1-year and 10-year rates.")

Both series show strong downward trend over time (non-stationary).

Strong positive correlation between 1-year and 10-year rates.

Regression in Levels vs. Changes

With trending data, we should be careful about spurious regression.

print("="*70)print("Regression in Levels with Time Trend")print("="*70)# Create time variabledata_rates['time'] = np.arange(len(data_rates))# Regression in levelsmodel_levels = ols('gs10 ~ gs1 + time', data=data_rates).fit()print("\nLevels regression (default SEs):")print(f" gs1 coef: {model_levels.params['gs1']:.6f}")print(f" R²: {model_levels.rsquared:.6f}")# HAC standard errors (Newey-West)model_levels_hac = ols('gs10 ~ gs1 + time', data=data_rates).fit(cov_type='HAC', cov_kwds={'maxlags': 24})print("\nLevels regression (HAC SEs with 24 lags):")print(f" gs1 coef: {model_levels_hac.params['gs1']:.6f}")print(f" gs1 SE (default): {model_levels.bse['gs1']:.6f}")print(f" gs1 SE (HAC): {model_levels_hac.bse['gs1']:.6f}")print(f"\n HAC SE is {model_levels_hac.bse['gs1'] / model_levels.bse['gs1']:.2f}x larger!")

======================================================================

Regression in Levels with Time Trend

======================================================================

Levels regression (default SEs):

gs1 coef: 0.507550

R²: 0.946883

Levels regression (HAC SEs with 24 lags):

gs1 coef: 0.507550

gs1 SE (default): 0.022147

gs1 SE (HAC): 0.080452

HAC SE is 3.63x larger!

Now that we have visualized the time series patterns and estimated regressions in levels, let’s formally examine autocorrelation in the residuals and its consequences for inference.

17.6: Autocorrelation

Autocorrelation (serial correlation) violates the independence assumption of OLS.

Consequences:

OLS remains unbiased and consistent

Standard errors are incorrect (typically too small)

Hypothesis tests invalid

Detection:

Correlogram: Plot of autocorrelations at different lags

Breusch-Godfrey test: LM test for serial correlation

Durbin-Watson statistic: Tests for AR(1) errors

Solutions:

HAC standard errors (Newey-West)

Model the autocorrelation (AR, ARMA models)

First differencing (if series are non-stationary)

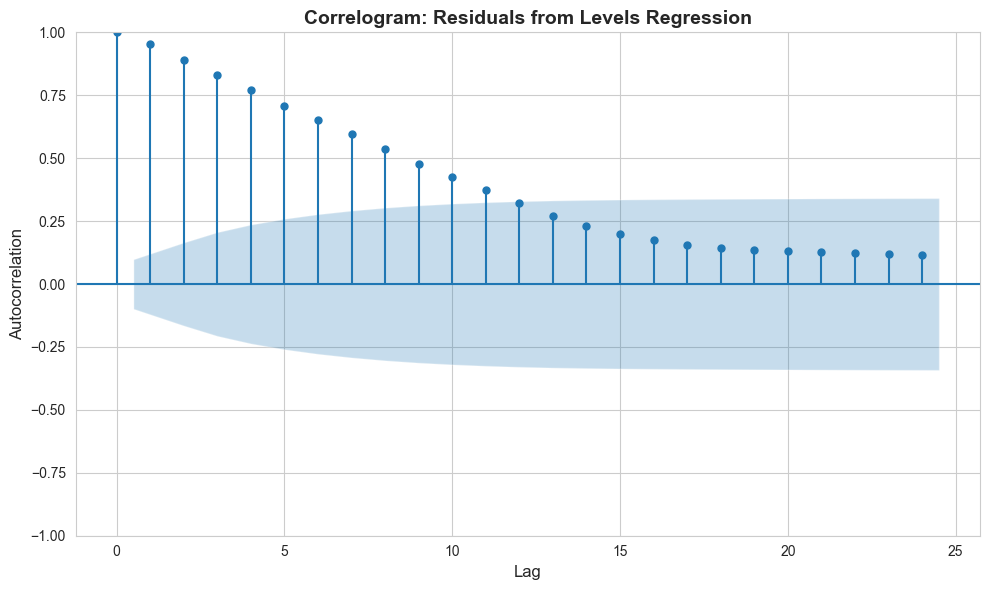

print("="*70)print("17.6 AUTOCORRELATION")print("="*70)# Check residual autocorrelation from levels regressiondata_rates['uhatgs10'] = model_levels.resid# Correlogramprint("\nAutocorrelations of residuals (levels regression):")acf_resid = acf(data_rates['uhatgs10'].dropna(), nlags=10)for i inrange(min(11, len(acf_resid))):print(f" Lag {i}: {acf_resid[i]:.6f}")print("\nStrong autocorrelation evident (lag 1 = {:.4f})".format(acf_resid[1]))

======================================================================

17.6 AUTOCORRELATION

======================================================================

Autocorrelations of residuals (levels regression):

Lag 0: 1.000000

Lag 1: 0.953418

Lag 2: 0.888093

Lag 3: 0.829507

Lag 4: 0.769449

Lag 5: 0.708815

Lag 6: 0.651059

Lag 7: 0.596161

Lag 8: 0.537987

Lag 9: 0.477552

Lag 10: 0.424660

Strong autocorrelation evident (lag 1 = 0.9534)

Key Concept 17.6: Detecting and Correcting Autocorrelation

The correlogram (ACF plot) reveals autocorrelation patterns in residuals. Slowly decaying autocorrelations (e.g., \(\rho_1 = 0.95\), \(\rho_{10} = 0.42\)) indicate non-stationarity and persistent shocks. With autocorrelation, default SEs are too small – HAC (Newey-West) SEs can be 3-8 times larger. Always check residual autocorrelation after estimating time series regressions and use HAC SEs or model the dynamics explicitly.

Correlogram Visualization

# Plot correlogramfig, ax = plt.subplots(figsize=(10, 6))plot_acf(data_rates['uhatgs10'].dropna(), lags=24, ax=ax, alpha=0.05)ax.set_title('Correlogram: Residuals from Levels Regression', fontsize=14, fontweight='bold')ax.set_xlabel('Lag', fontsize=12)ax.set_ylabel('Autocorrelation', fontsize=12)plt.tight_layout()plt.show()print("Autocorrelations decay very slowly (characteristic of non-stationary series).")

Autocorrelations decay very slowly (characteristic of non-stationary series).

First Differencing

First differencing can remove trends and reduce autocorrelation.

print("="*70)print("Regression in Changes (First Differences)")print("="*70)# Regression in changesmodel_changes = ols('dgs10 ~ dgs1', data=data_rates).fit()print("\nChanges regression:")print(f" dgs1 coef: {model_changes.params['dgs1']:.6f}")print(f" dgs1 SE: {model_changes.bse['dgs1']:.6f}")print(f" R²: {model_changes.rsquared:.6f}")# Check residual autocorrelationuhat_dgs10 = model_changes.residacf_dgs10_resid = acf(uhat_dgs10.dropna(), nlags=10)print("\nAutocorrelations of residuals (changes regression):")for i inrange(min(11, len(acf_dgs10_resid))):print(f" Lag {i}: {acf_dgs10_resid[i]:.6f}")print("\nMuch lower autocorrelation after differencing!")

======================================================================

Regression in Changes (First Differences)

======================================================================

Changes regression:

dgs1 coef: 0.719836

dgs1 SE: 0.031443

R²: 0.570860

Autocorrelations of residuals (changes regression):

Lag 0: 1.000000

Lag 1: 0.254801

Lag 2: -0.038743

Lag 3: 0.060813

Lag 4: 0.023676

Lag 5: -0.027540

Lag 6: -0.011310

Lag 7: 0.042843

Lag 8: 0.081094

Lag 9: -0.001712

Lag 10: -0.019733

Much lower autocorrelation after differencing!

Key Concept 17.7: First Differencing for Nonstationary Data

First differencing (\(\Delta y_t = y_t - y_{t-1}\)) transforms non-stationary trending series into stationary ones, eliminating spurious regression problems. After differencing, the residual autocorrelation drops dramatically (from \(\rho_1 \approx 0.95\) to \(\rho_1 \approx 0.25\) in the interest rate example). The coefficient interpretation changes from levels to changes: a 1-percentage-point change in the 1-year rate is associated with a 0.72-percentage-point change in the 10-year rate.

ADL estimates dynamics of adjustment to this equilibrium

Why Negative Own-Lag Coefficients?

At first, this seems counterintuitive:

Interest rates are persistent in levels

But changes show mean reversion

Explanation:

Levels are I(1): Random walk with drift

Changes are I(0): Stationary, but with negative serial correlation

Overshooting: Markets overreact to news, then partially correct

Example:

Month 1: Fed unexpectedly raises 1-year rate by 1%

10-year rate increases by 0.60% (overshoots equilibrium)

Month 2: Market reassesses

10-year rate decreases by 0.10% (partial reversal)

Month 3: Further adjustment

10-year rate changes by -0.02% (approaching equilibrium)

Long run: 10-year rate settles at +0.85% (new equilibrium)

Practical Value:

Central banks:

Understand how policy rate changes affect long rates

Timing and magnitude of transmission

Bond traders:

Predict interest rate movements

Arbitrage opportunities if model predicts well

Economists:

Test theories (expectations hypothesis, term premium)

Understand financial market dynamics

Model Selection:

Chose ADL(2,2) based on:

Information criteria (AIC, BIC)

Residual diagnostics (low autocorrelation)

Economic theory (2 lags reasonable for monthly data)

Parsimony (not too many parameters)

Could try ADL(3,3), but gains typically minimal

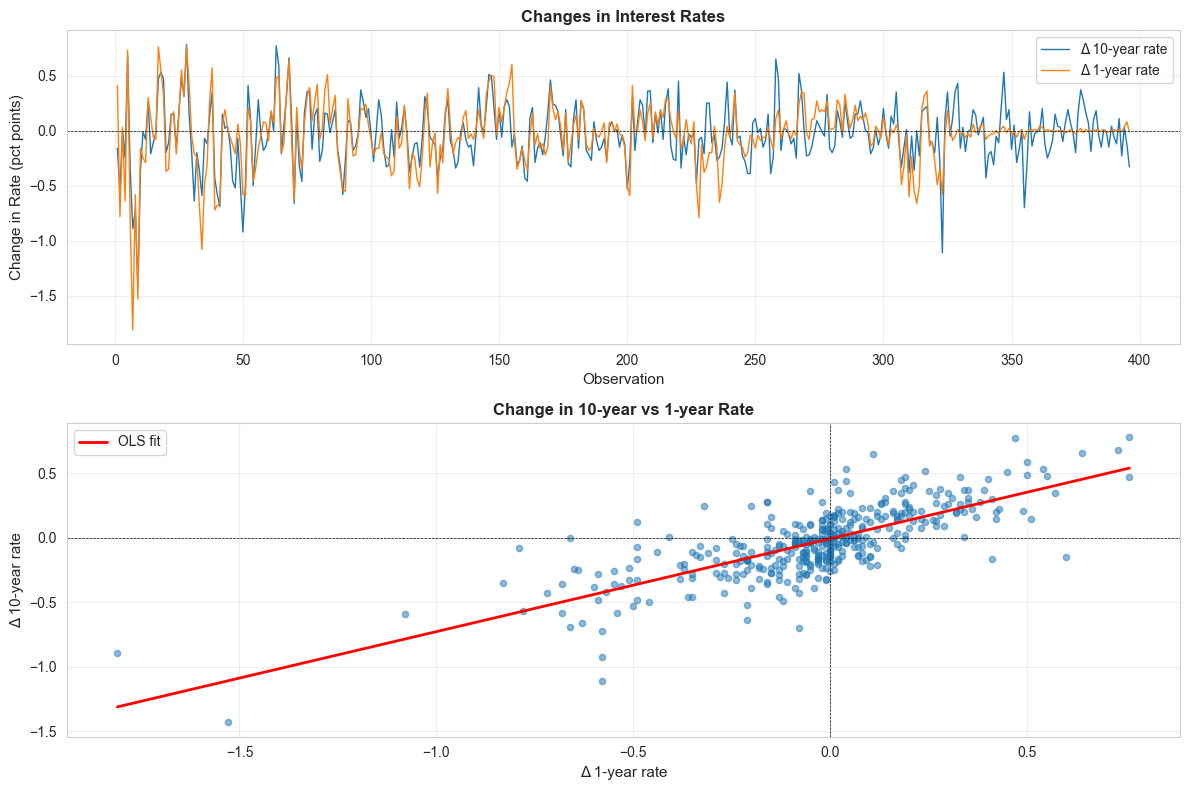

Visualization: Changes in Interest Rates

# Figure: Changesfig, axes = plt.subplots(2, 1, figsize=(12, 8))# Panel 1: Time series of changesaxes[0].plot(data_rates.index, data_rates['dgs10'], label='Δ 10-year rate', linewidth=1)axes[0].plot(data_rates.index, data_rates['dgs1'], label='Δ 1-year rate', linewidth=1)axes[0].axhline(y=0, color='white', alpha=0.3, linestyle='--', linewidth=0.5)axes[0].set_xlabel('Observation', fontsize=11)axes[0].set_ylabel('Change in Rate (pct points)', fontsize=11)axes[0].set_title('Changes in Interest Rates', fontsize=12, fontweight='bold')axes[0].legend()axes[0].grid(True, alpha=0.3)# Panel 2: Scatter plot of changesaxes[1].scatter(data_rates['dgs1'], data_rates['dgs10'], alpha=0.5, s=20)valid_idx = data_rates[['dgs1', 'dgs10']].dropna().indexz = np.polyfit(data_rates.loc[valid_idx, 'dgs1'], data_rates.loc[valid_idx, 'dgs10'], 1)p = np.poly1d(z)dgs1_range = np.linspace(data_rates['dgs1'].min(), data_rates['dgs1'].max(), 100)axes[1].plot(dgs1_range, p(dgs1_range), 'r-', linewidth=2, label='OLS fit')axes[1].axhline(y=0, color='white', alpha=0.3, linestyle='--', linewidth=0.5)axes[1].axvline(x=0, color='white', alpha=0.3, linestyle='--', linewidth=0.5)axes[1].set_xlabel('Δ 1-year rate', fontsize=11)axes[1].set_ylabel('Δ 10-year rate', fontsize=11)axes[1].set_title('Change in 10-year vs 1-year Rate', fontsize=12, fontweight='bold')axes[1].legend()axes[1].grid(True, alpha=0.3)plt.tight_layout()plt.show()print("Changes fluctuate around zero (stationary-looking).")print("Positive correlation between changes (rates move together).")

Changes fluctuate around zero (stationary-looking).

Positive correlation between changes (rates move together).

Having developed tools for handling panel data and time series, we now address the fundamental question of causality – how to move from correlation to causal inference using econometric methods.

17.7: Causality and Instrumental Variables

Establishing causality is central to econometrics. Correlation does not imply causation!

The fundamental problem:

In regression \(y = \beta_1 + \beta_2 x + u\), OLS is biased if \(E[u|x] \neq 0\)

Sources of endogeneity:

Omitted variables

Measurement error

Simultaneity (reverse causation)

Instrumental Variables (IV) solution:

Find an instrument \(z\) that:

Relevance: Correlated with \(x\) (can be tested)

Exogeneity: Uncorrelated with \(u\) (cannot be tested - must argue)

IV estimator:

\[\hat{\beta}_{IV} = \frac{Cov(z,y)}{Cov(z,x)}\]

Causal inference methods:

Randomized experiments (RCT)

Instrumental variables (IV)

Difference-in-differences (DID)

Regression discontinuity (RD)

Fixed effects (control for unobserved heterogeneity)

Matching and propensity scores

Key insight: Need credible identification strategy, not just controls!

print("="*70)print("17.7 CAUSALITY AND INSTRUMENTAL VARIABLES")print("="*70)print("\nKey Points on Causality:")print("-"*70)print("\n1. Correlation ≠ Causation")print(" - Regression shows association, not necessarily causation")print(" - Need to rule out confounding, reverse causation, selection")print("\n2. Randomized Controlled Trials (RCT)")print(" - Gold standard: Randomly assign treatment")print(" - Ensures treatment uncorrelated with potential outcomes")print(" - Causal effect = difference in means")print("\n3. Observational Data Methods")print(" - Instrumental Variables: Use variation from instrument")print(" - Fixed Effects: Control for time-invariant unobservables")print(" - Difference-in-Differences: Compare treatment vs control over time")print(" - Regression Discontinuity: Exploit threshold for treatment")print("\n4. Potential Outcomes Framework")print(" - Y₁ᵢ: Outcome if treated")print(" - Y₀ᵢ: Outcome if not treated")print(" - Individual treatment effect: Y₁ᵢ - Y₀ᵢ")print(" - Problem: Only observe one potential outcome!")print(" - ATE = E[Y₁ᵢ - Y₀ᵢ]: Average Treatment Effect")print("\n5. Instrumental Variables")print(" - Requires valid instrument z:")print(" (a) Relevant: Corr(z,x) ≠ 0")print(" (b) Exogenous: Corr(z,u) = 0")print(" - Example: Distance to college as IV for education")print(" - Weak instruments: Large standard errors")print("\n6. Panel Data and Causality")print(" - Fixed Effects: Controls for αᵢ (unobserved heterogeneity)")print(" - Causal if: Conditional on αᵢ, X exogenous")print(" - NBA example: FE controls for team characteristics")print(" - Identifies within-team effect of wins on revenue")print("\n"+"="*70)print("Practical Recommendations")print("="*70)print("\n1. Always think about potential confounders")print("2. Use robust/cluster standard errors")print("3. Test multiple specifications")print("4. Report both OLS and IV/FE when appropriate")print("5. Be transparent about identification assumptions")print("6. Causal claims require strong justification!")

======================================================================

17.7 CAUSALITY AND INSTRUMENTAL VARIABLES

======================================================================

Key Points on Causality:

----------------------------------------------------------------------

1. Correlation ≠ Causation

- Regression shows association, not necessarily causation

- Need to rule out confounding, reverse causation, selection

2. Randomized Controlled Trials (RCT)

- Gold standard: Randomly assign treatment

- Ensures treatment uncorrelated with potential outcomes

- Causal effect = difference in means

3. Observational Data Methods

- Instrumental Variables: Use variation from instrument

- Fixed Effects: Control for time-invariant unobservables

- Difference-in-Differences: Compare treatment vs control over time

- Regression Discontinuity: Exploit threshold for treatment

4. Potential Outcomes Framework

- Y₁ᵢ: Outcome if treated

- Y₀ᵢ: Outcome if not treated

- Individual treatment effect: Y₁ᵢ - Y₀ᵢ

- Problem: Only observe one potential outcome!

- ATE = E[Y₁ᵢ - Y₀ᵢ]: Average Treatment Effect

5. Instrumental Variables

- Requires valid instrument z:

(a) Relevant: Corr(z,x) ≠ 0

(b) Exogenous: Corr(z,u) = 0

- Example: Distance to college as IV for education

- Weak instruments: Large standard errors

6. Panel Data and Causality

- Fixed Effects: Controls for αᵢ (unobserved heterogeneity)

- Causal if: Conditional on αᵢ, X exogenous

- NBA example: FE controls for team characteristics

- Identifies within-team effect of wins on revenue

======================================================================

Practical Recommendations

======================================================================

1. Always think about potential confounders

2. Use robust/cluster standard errors

3. Test multiple specifications

4. Report both OLS and IV/FE when appropriate

5. Be transparent about identification assumptions

6. Causal claims require strong justification!

Key Concept 17.8: Instrumental Variables and Causal Inference

Endogeneity (regressors correlated with errors) biases OLS estimates. Sources include omitted variables, measurement error, and simultaneity. Instrumental variables (IV) provide a solution: find a variable \(z\) that is correlated with the endogenous regressor (relevance) but uncorrelated with the error (exogeneity). The IV estimator \(\hat{\beta}_{IV} = \text{Cov}(z,y)/\text{Cov}(z,x)\) is consistent even when OLS is biased. Complementary causal methods include RCTs, DiD, RD, and matching.

Key Takeaways

Panel Data Methods:

Panel data combines cross-sectional and time series dimensions, observing multiple individuals over multiple periods

Variance decomposition separates total variation into within (over time) and between (across individuals) components

Pooled OLS ignores panel structure; always use cluster-robust standard errors clustered by individual

Fixed effects controls for time-invariant unobserved heterogeneity by using only within-individual variation

Random effects is more efficient than FE but assumes individual effects are uncorrelated with regressors

FE is preferred when individual effects are likely correlated with regressors (use Hausman test to decide)

Nonlinear Models:

Logit models estimate the probability of binary outcomes using the logistic function

Marginal effects (\(\hat{p}(1-\hat{p})\beta_j\)) give the change in probability from a one-unit change in \(x_j\)

Logit marginal effects and linear probability model coefficients are typically similar in magnitude

Time Series Analysis:

Time series data exhibit autocorrelation, where observations are correlated with their past values

Non-stationary series (trending) can produce spurious regressions with misleadingly high \(R^2\)

First differencing removes trends and reduces autocorrelation, transforming non-stationary series to stationary

HAC (Newey-West) standard errors account for both heteroskedasticity and autocorrelation in time series

Default SEs can be dramatically too small with autocorrelation (3-8x understatement is common)

Dynamic Models:

Autoregressive (AR) models capture persistence by including lagged dependent variables

Autoregressive distributed lag (ADL) models include lags of both the dependent and independent variables

The correlogram (ACF plot) helps determine the appropriate number of lags

Total multiplier from an ADL model gives the long-run effect of a permanent change in \(x\)

Causality and Instrumental Variables:

Correlation does not imply causation; endogeneity (omitted variables, reverse causation, measurement error) biases OLS

Next steps: Apply these methods to your own research questions. Panel data methods, time series models, and causal inference strategies are essential tools for any applied econometrician working with observational data.

Congratulations! You’ve completed Chapter 17, the final chapter covering panel data, time series, and causal inference. You now have a comprehensive toolkit of econometric methods for analyzing real-world data.

Practice Exercises

Exercise 1: Panel Data Variance Decomposition

A panel dataset of 50 firms over 5 years shows:

Overall standard deviation of log revenue: 0.80

Between standard deviation: 0.70

Within standard deviation: 0.30

Which source of variation dominates? What does this imply about the importance of firm-specific characteristics?

If you run fixed effects, what proportion of the total variation are you using for estimation?

Would you expect the FE coefficient to be larger or smaller than pooled OLS? Explain using the omitted variables bias formula.

Exercise 2: Cluster-Robust Standard Errors

You estimate a panel regression of test scores on class size using data from 100 schools over 3 years (300 observations). The coefficient on class size has:

Default SE: 0.15 (t = 3.33)

Cluster-robust SE (by school): 0.45 (t = 1.11)

Why is the cluster SE three times larger than the default SE?

Does your conclusion about the significance of class size change? At what significance level?

What is the effective number of independent observations in this panel?

Exercise 3: Fixed Effects vs. Random Effects

You estimate a wage equation using panel data on 500 workers over 10 years. The Hausman test yields \(\chi^2 = 25.4\) with 3 degrees of freedom (\(p < 0.001\)).

State the null and alternative hypotheses of the Hausman test.

What do you conclude? Which estimator should you use?

Give an economic reason why the RE assumption might fail in a wage equation (hint: think about unobserved ability).

Exercise 4: Time Series Autocorrelation

A regression of the 10-year interest rate on the 1-year rate using monthly data yields residuals with:

Lag 1 autocorrelation: 0.95

Lag 5 autocorrelation: 0.75

Default SE on the 1-year rate coefficient: 0.022

HAC SE (24 lags): 0.080

Is there evidence of autocorrelation? What does the slowly decaying ACF pattern suggest about the data?

By what factor do the HAC SEs differ from default SEs? What are the implications for hypothesis testing?

Would first differencing help? What would you expect the lag 1 autocorrelation of the differenced residuals to be?

Exercise 5: Spurious Regression

You regress GDP on the number of mobile phone subscriptions over 30 years and find \(R^2 = 0.97\) with a highly significant coefficient.

Why might this be a spurious regression? What is the key characteristic of both series?

Describe two methods to address this problem.

If you first-difference both series, what economic relationship (if any) would the regression estimate?

Exercise 6: Identifying Causal Effects

For each scenario, identify the main threat to causal inference and suggest an appropriate method:

Estimating the effect of police spending on crime rates across cities (cross-sectional data).

Estimating the effect of a minimum wage increase on employment (state-level panel data with staggered adoption).

Estimating the effect of class size on student achievement (students assigned to classes based on a cutoff rule).

Case Studies

Case Study 1: Panel Data Analysis of Cross-Country Productivity

In this case study, you will apply panel data methods from this chapter to analyze labor productivity dynamics across countries using the Mendez convergence clubs dataset.

Sample: 108 countries, 1990-2014 (panel structure: country \(\times\) year)

Variables:lp (labor productivity), rk (physical capital), hc (human capital), rgdppc (real GDP per capita), tfp (total factor productivity), region, country

Research question: How do physical and human capital affect labor productivity across countries, and does controlling for unobserved country characteristics change the estimates?

Task 1: Panel Data Structure (Guided)

Load the dataset and explore its panel structure. Calculate the within and between variation for log labor productivity.

Which source of variation dominates? What does this imply for the choice between pooled OLS and fixed effects?

Task 2: Pooled OLS with Cluster-Robust SEs (Guided)

Estimate a pooled OLS regression of log productivity on log physical capital and human capital. Compare default and cluster-robust standard errors (clustered by country).

How much larger are cluster SEs? What does this tell you about within-country correlation?

Task 3: Fixed Effects Estimation (Semi-guided)

Estimate a fixed effects model controlling for country-specific characteristics. Compare the FE coefficients with the pooled OLS coefficients.

Hint: Use linearmodels.panel. PanelOLS with entity_effects=True, or use the within transformation manually by de-meaning the variables by country.

Which coefficients change most? What unobserved country characteristics might be driving the difference?

Task 4: Time Trends in Productivity (Semi-guided)

Add a time trend or year fixed effects to the panel model. Test whether productivity growth rates differ across regions.

Hint: Use time_effects=True in PanelOLS for year fixed effects, or create region-year interaction terms.

Is there evidence of convergence (faster growth in initially poorer countries)?

Task 5: Regional Heterogeneity with Interactions (Independent)

Estimate models that allow the returns to physical and human capital to vary by region:

Add region dummy variables

Add region-capital interaction terms

Test the joint significance of regional interactions

Do returns to capital differ significantly across regions? Which regions show the highest returns to human capital?

Task 6: Policy Brief on Capital and Productivity (Independent)

Write a 200-300 word policy brief addressing: What are the most effective channels for increasing labor productivity across countries? Your brief should:

Compare pooled OLS and fixed effects estimates of capital returns

Discuss whether the relationship is causal (what are the threats to identification?)

Evaluate whether returns to capital differ by region

Recommend policies based on the relative importance of physical vs. human capital

Key Concept 17.9: Panel Data for Cross-Country Analysis

Cross-country panel data enables controlling for time-invariant country characteristics (institutions, geography, culture) that confound cross-sectional estimates. Fixed effects absorb these permanent differences, identifying the relationship between capital accumulation and productivity growth from within-country variation over time. The typical finding is that FE coefficients are smaller than pooled OLS, indicating positive omitted variable bias in cross-sectional estimates.

Key Concept 17.10: Choosing Between Panel Data Estimators

The choice between pooled OLS, fixed effects, and random effects depends on the research question and data structure. Use pooled OLS with cluster SEs for descriptive associations; use FE when unobserved individual heterogeneity is likely correlated with regressors (the common case); use RE only when individual effects are plausibly random and uncorrelated with regressors (e.g., randomized experiments). The Hausman test helps decide between FE and RE, but economic reasoning should guide the choice.

What You’ve Learned: In this case study, you applied the complete panel data toolkit to cross-country productivity analysis. You decomposed variation into within and between components, compared pooled OLS with fixed effects, examined cluster-robust standard errors, and explored regional heterogeneity. These methods are essential for any empirical analysis using panel data.

Case Study 2: Luminosity and Development Over Time: A Panel Approach

Research Question: How does nighttime luminosity evolve across Bolivia’s municipalities over time, and what does within-municipality variation reveal about development dynamics?

Background: Throughout this textbook, we have analyzed cross-sectional satellite-development relationships. But the DS4Bolivia dataset includes nighttime lights data for 2012-2020, creating a natural panel dataset. In this case study, we apply Chapter 17’s panel data tools to track how luminosity evolves across municipalities over time, using fixed effects to control for time-invariant characteristics.

The Data: The DS4Bolivia dataset covers 339 Bolivian municipalities with annual nighttime lights and population data for 2012-2020, yielding a potential panel of 3,051 municipality-year observations.

Key Variables:

mun: Municipality name

dep: Department (administrative region)

asdf_id: Unique municipality identifier

ln_NTLpc2012 through ln_NTLpc2020: Log nighttime lights per capita (annual)

pop2012 through pop2020: Population (annual)

Load the DS4Bolivia Data and Create Panel Structure

# Load the DS4Bolivia datasetimport pandas as pdimport numpy as npimport matplotlib.pyplot as pltfrom statsmodels.formula.api import olsurl_bol ="https://raw.githubusercontent.com/quarcs-lab/ds4bolivia/master/ds4bolivia_v20250523.csv"bol = pd.read_csv(url_bol)# Display available NTL and population variablesntl_vars = [c for c in bol.columns if c.startswith('ln_NTLpc')]pop_vars = [c for c in bol.columns if c.startswith('pop') and c[3:].isdigit()]print("="*70)print("DS4BOLIVIA: PANEL DATA CASE STUDY")print("="*70)print(f"Cross-sectional units: {len(bol)} municipalities")print(f"\nNTL variables available: {ntl_vars}")print(f"Population variables available: {pop_vars}")

Verify the panel structure: 339 municipalities x 9 years = 3,051 observations

Show head() and describe() for the panel dataset

# Your code here: Reshape to panel format## Example structure:# # Reshape NTL variables# ntl_cols = {f'ln_NTLpc{y}': y for y in range(2012, 2021)}# pop_cols = {f'pop{y}': y for y in range(2012, 2021)}## # Melt NTL# ntl_long = bol[['mun', 'dep', 'asdf_id'] + list(ntl_cols.keys())].melt(# id_vars=['mun', 'dep', 'asdf_id'],# var_name='ntl_var', value_name='ln_NTLpc'# )# ntl_long['year'] = ntl_long['ntl_var'].str.extract(r'(\d{4})').astype(int)## # Melt Population# pop_long = bol[['asdf_id'] + list(pop_cols.keys())].melt(# id_vars=['asdf_id'],# var_name='pop_var', value_name='pop'# )# pop_long['year'] = pop_long['pop_var'].str.extract(r'(\d{4})').astype(int)## # Merge# panel = ntl_long.merge(pop_long[['asdf_id', 'year', 'pop']],# on=['asdf_id', 'year'], how='left')# panel['ln_pop'] = np.log(panel['pop'])# panel = panel.sort_values(['asdf_id', 'year']).reset_index(drop=True)## print(f"Panel shape: {panel.shape}")# print(f"Municipalities: {panel['asdf_id'].nunique()}")# print(f"Years: {sorted(panel['year'].unique())}")# print(panel.head(18)) # Show 2 municipalities# print(panel[['ln_NTLpc', 'ln_pop', 'pop']].describe().round(3))

Key Concept 17.10: Satellite Panel Data

Annual nighttime lights observations create panel datasets even where traditional economic surveys are unavailable or infrequent. For Bolivia’s 339 municipalities over 2012-2020, the NTL panel provides 3,051 municipality-year observations. This temporal dimension allows us to move beyond cross-sectional associations and study changes within municipalities over time—a crucial step toward understanding development dynamics rather than just static patterns.

Task 2: Pooled OLS with Cluster-Robust SEs (Guided)

Objective: Estimate a pooled OLS regression of NTL on population with cluster-robust standard errors.

Instructions:

Estimate ln_NTLpc ~ ln_pop + year using all panel observations

Use cluster-robust standard errors clustered by municipality

Compare default and cluster-robust SEs

Interpret: How does population relate to NTL? Is there a significant time trend?

# Your code here: Pooled OLS with cluster-robust SEs## Example structure:# panel_reg = panel[['ln_NTLpc', 'ln_pop', 'year', 'mun', 'asdf_id']].dropna()## model_pooled = ols('ln_NTLpc ~ ln_pop + year', data=panel_reg).fit(# cov_type='cluster', cov_kwds={'groups': panel_reg['asdf_id']}# )# print("POOLED OLS WITH CLUSTER-ROBUST SEs")# print(model_pooled.summary())

Task 3: Fixed Effects (Semi-guided)

Objective: Estimate a fixed effects model controlling for time-invariant municipality characteristics.

Instructions:

Add municipality fixed effects using C(asdf_id) or entity demeaning

Compare FE coefficients with pooled OLS coefficients

How does controlling for time-invariant municipality characteristics change the population-NTL relationship?

Discuss: What unobserved factors do municipality fixed effects absorb (altitude, remoteness, climate)?

Hint: You can use C(asdf_id) in the formula, or manually demean variables by subtracting municipality means. For large datasets, demeaning is more computationally efficient.

# Your code here: Fixed effects estimation## Example structure (demeaning approach):# # Demean variables within each municipality# for col in ['ln_NTLpc', 'ln_pop']:# panel_reg[f'{col}_dm'] = panel_reg.groupby('asdf_id')[col].transform(# lambda x: x - x.mean()# )# panel_reg['year_dm'] = panel_reg['year'] - panel_reg.groupby('asdf_id')['year'].transform('mean')## model_fe = ols('ln_NTLpc_dm ~ ln_pop_dm + year_dm - 1', data=panel_reg).fit(# cov_type='cluster', cov_kwds={'groups': panel_reg['asdf_id']}# )# print("FIXED EFFECTS (WITHIN ESTIMATOR)")# print(model_fe.summary())## print("\nCOMPARISON:")# print(f" Pooled OLS ln_pop coef: {model_pooled.params['ln_pop']:.4f}")# print(f" Fixed Effects ln_pop coef: {model_fe.params['ln_pop_dm']:.4f}")

Key Concept 17.11: Fixed Effects for Spatial Heterogeneity

Municipality fixed effects absorb all time-invariant characteristics: altitude, remoteness, climate, historical infrastructure, cultural factors. After removing these fixed differences, the remaining variation identifies how changes in population (or other time-varying factors) relate to changes in NTL within the same municipality. This within-municipality analysis is more credible for causal interpretation than cross-sectional regressions, because it eliminates bias from unobserved time-invariant confounders.

Task 4: Time Trends (Semi-guided)

Objective: Examine how nighttime lights evolve over time using year fixed effects.

Instructions:

Replace the linear time trend with year dummy variables: C(year)

Test whether the year effects are jointly significant

Plot the estimated year coefficients to visualize the NTL trajectory

Discuss: Did NTL grow steadily, or were there jumps or declines?

Hint: Use one year as the reference category. The year coefficients show NTL changes relative to the base year.

# Your code here: Year fixed effects## Example structure:# # Estimate with year dummies (demeaned for municipality FE)# panel_reg['year_cat'] = panel_reg['year'].astype(str)## # Simple approach: use year means of demeaned NTL# year_means = panel_reg.groupby('year')['ln_NTLpc'].mean()# year_means_dm = year_means - year_means.iloc[0] # relative to base year## fig, ax = plt.subplots(figsize=(10, 6))# ax.plot(year_means.index, year_means.values, 'o-', color='navy', linewidth=2)# ax.set_xlabel('Year')# ax.set_ylabel('Mean Log NTL per Capita')# ax.set_title('Average Municipal NTL Over Time (2012-2020)')# ax.grid(True, alpha=0.3)# plt.tight_layout()# plt.show()

Task 5: First Differences (Independent)

Objective: Estimate the relationship using first differences as an alternative to fixed effects.

Instructions:

Compute first differences: \(\Delta ln\_NTLpc = ln\_NTLpc_t - ln\_NTLpc_{t-1}\) and \(\Delta ln\_pop = ln\_pop_t - ln\_pop_{t-1}\)

Estimate \(\Delta ln\_NTLpc \sim \Delta ln\_pop\)

Compare the first-difference coefficient with the fixed effects estimate

Discuss: When do FE and FD give different results? What assumptions does each require?

# Your code here: First differences estimation## Example structure:# panel_reg = panel_reg.sort_values(['asdf_id', 'year'])# panel_reg['d_ln_NTLpc'] = panel_reg.groupby('asdf_id')['ln_NTLpc'].diff()# panel_reg['d_ln_pop'] = panel_reg.groupby('asdf_id')['ln_pop'].diff()## # Drop first year (no difference available)# fd_data = panel_reg.dropna(subset=['d_ln_NTLpc', 'd_ln_pop'])## model_fd = ols('d_ln_NTLpc ~ d_ln_pop', data=fd_data).fit(# cov_type='cluster', cov_kwds={'groups': fd_data['asdf_id']}# )# print("FIRST DIFFERENCES ESTIMATION")# print(model_fd.summary())## print(f"\nFD coefficient on ln_pop: {model_fd.params['d_ln_pop']:.4f}")

Task 6: Panel Brief (Independent)

Objective: Write a 200-300 word brief summarizing your panel data analysis.

Your brief should address:

What do within-municipality changes in NTL reveal about development dynamics?

How does the FE population coefficient differ from the cross-sectional (pooled OLS) one?

What time trends in NTL are visible across 2012-2020?

How do FE and FD estimates compare? Which assumptions matter most?

What are the advantages and limitations of satellite panel data for tracking municipal development over time?

What additional time-varying variables would improve the analysis?

# Your code here: Additional analysis for the panel brief## You might want to:# 1. Decompose variance into between and within components# 2. Plot NTL trajectories for selected municipalities# 3. Compare growth rates across departments# 4. Create a summary table of all estimation results## Example: Variance decomposition# overall_var = panel_reg['ln_NTLpc'].var()# between_var = panel_reg.groupby('asdf_id')['ln_NTLpc'].mean().var()# within_var = panel_reg.groupby('asdf_id')['ln_NTLpc'].apply(lambda x: x - x.mean()).var()# print(f"Overall variance: {overall_var:.4f}")# print(f"Between variance: {between_var:.4f}")# print(f"Within variance: {within_var:.4f}")# print(f"Between share: {between_var/overall_var:.1%}")

What You’ve Learned from This Case Study

This is the final DS4Bolivia case study in the textbook. Across 12 chapters, you have applied the complete econometric toolkit—from simple descriptive statistics (Chapter 1) through panel data methods (Chapter 17)—to study how satellite data can predict and monitor local economic development. The DS4Bolivia project demonstrates that modern data science and econometrics, combined with freely available satellite imagery, can contribute to SDG monitoring even in data-scarce contexts.

In this panel data analysis, you’ve applied Chapter 17’s complete toolkit:

Panel construction: Reshaped cross-sectional data into a municipality-year panel

Pooled OLS: Estimated baseline relationships with cluster-robust standard errors

Fixed effects: Controlled for time-invariant municipality characteristics

Time trends: Examined the trajectory of nighttime lights across 2012-2020

First differences: Used an alternative estimation strategy and compared with FE

Critical thinking: Assessed what within-municipality variation reveals about development dynamics

Congratulations! You have now completed the full DS4Bolivia case study arc across the textbook.