---

title: "Matrix Completion and Interactive Fixed Effects"

---

## When parallel trends isn't enough

Chapter 9 squeezed every drop of usable signal out of the

Callaway-Sant'Anna minimum-wage panel under one identifying

assumption: **parallel trends**. Conditional or unconditional, with

or without never-treated counties, with or without anticipation

slack, with Rambachan-Roth bounds on top — the assumption is always

that, absent treatment, the trajectory of the treated counties would

have moved *in parallel* with the untreated.

What if it would not have? Counties select into raising the minimum

wage non-randomly. They are not a random subset of the country in

the time-varying dimension either: industry mix, demographics, and

local growth trends all shape both treatment timing and outcome

paths. Two counties can share an industry-mix-driven trajectory that

TWFE never absorbs — and so cannot net out.

This chapter relaxes parallel trends in a specific way. We model the

counterfactual outcome as a **factor structure**:

$$Y_{it}(0) \;=\; \alpha_i + \xi_t + \lambda_i' f_t + \varepsilon_{it}.$$

Each unit $i$ has a loading vector $\lambda_i$; each period a factor

vector $f_t$. Their interaction $\lambda_i' f_t$ encodes

time-varying unobserved heterogeneity that no county or year fixed

effect can absorb. Two views of the same object give two estimators

[@liu2024practical]:

- **Interactive Fixed Effects (IFEct)** [@bai2009panel; @xu2017generalized]

treats $(\alpha, \xi, \Lambda, F)$ as parameters to be estimated on

control observations, then imputes $Y_{it}(0)$ on treated cells.

- **Matrix Completion (MC)** [@athey2021matrix] reframes the same

problem as filling missing entries of the implicit $Y(0)$ matrix:

mask the treated cells, then complete via nuclear-norm-regularised

SVD.

Yiqing Xu's `fect` package implements both with a common API and a

common counterfactual-plot diagnostic. By chapter's end we line up

its IFE and MC estimates next to the Callaway-Sant'Anna ATT from

chapter 9 on the same panel — three estimands, three identifying

assumptions, one substantive question.

## Setup and data

```{r}

#| label: setup

#| message: false

#| warning: false

library(tidyverse)

library(fect)

library(panelView)

library(did)

library(patchwork)

source("R/table_helpers.R")

set.seed(42)

knitr::opts_chunk$set(dev.args = list(bg = "transparent"))

theme_set(

theme_minimal(base_size = 12) +

theme(

plot.background = element_rect(fill = "transparent", color = NA),

panel.background = element_rect(fill = "transparent", color = NA),

panel.grid.major = element_line(color = "#94a3b8", linewidth = 0.25),

panel.grid.minor = element_line(color = "#94a3b8", linewidth = 0.15),

text = element_text(color = "#94a3b8"),

axis.text = element_text(color = "#94a3b8"),

strip.text = element_text(color = "#94a3b8"),

legend.text = element_text(color = "#94a3b8")

)

)

```

We work from the same `cs_minwage.rds` panel as chapter 9, but with

one small adjustment: factor-based estimators need **at least as

many pre-treatment periods per cohort as the number of factors they

try to fit**. Chapter 9's 2003-2007 window leaves the 2004 cohort

with only one pre-period, which would force `min.T0 = 1` and cap

the rank at zero — collapsing IFEct back to TWFE. So we widen the

pre-treatment window by two years to 2001-2007; everything else

(cohort filter, region drop, treatment indicator) is identical.

```{r}

#| label: data-load

mw_raw <- readRDS("data/cs_minwage.rds") |> as_tibble()

mw <- mw_raw |>

filter(G %in% c(0, 2004, 2006, 2007), region != "1") |>

filter(G != 2007, year >= 2001) |>

mutate(D = as.integer(year >= G & G != 0))

dim(mw)

```

```{r}

#| label: tbl-cohorts

#| tbl-cap: "Cohorts in the 2001-2007 working panel. $G = 0$ is the never-treated control pool; the two treated cohorts have 3 and 5 pre-treatment years respectively."

mw |>

filter(year == 2001) |>

count(G, name = "counties") |>

mutate(`Pre-periods` = case_when(

G == 0 ~ NA_integer_,

G == 2004 ~ 3L,

G == 2006 ~ 5L

)) |>

rename(`Cohort (G)` = G) |>

gt_pretty()

```

The outcome `lemp` (log teen employment) and the treatment indicator

`D` (1 once a county's state has raised its minimum wage above the

federal floor, 0 otherwise) line up with chapter 9's definitions.

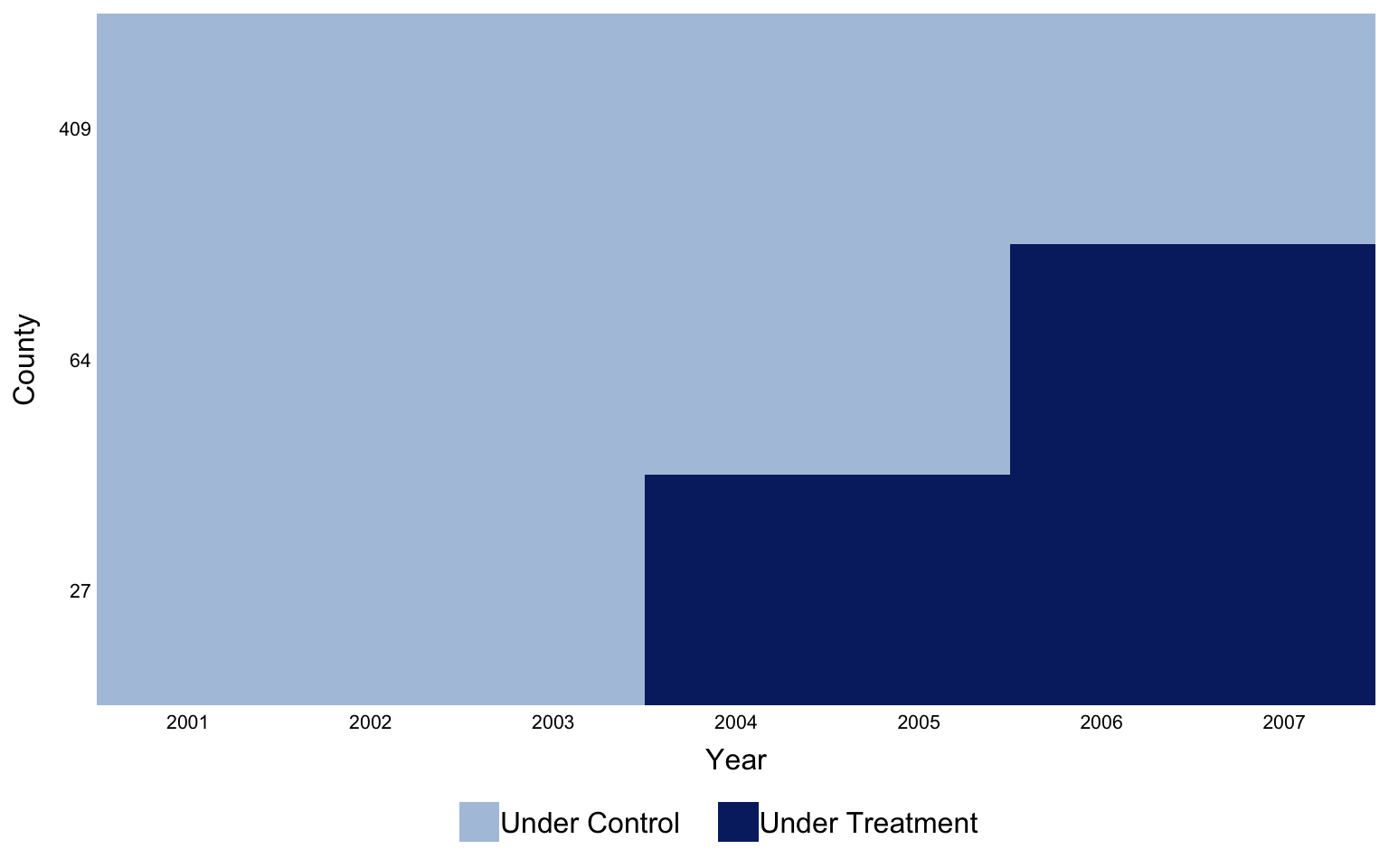

## Visualising the panel

`panelView` is the natural opener for any FECT workflow. It draws

units on the vertical axis and time on the horizontal, coloured by

treatment status, so the staggered-adoption structure of the panel

is immediate.

```{r}

#| label: fig-panelview

#| fig-cap: "Treatment status by county and year. The two horizontal bands of pink are the 2004 and 2006 cohorts; the wide grey band underneath is the never-treated $G = 0$ control pool. The visible step in the pink rows is the staggered adoption that breaks TWFE."

#| fig-width: 8

#| fig-height: 5

panelview(data = as.data.frame(mw), formula = lemp ~ D,

index = c("id", "year"),

xlab = "Year", ylab = "County",

main = "", legendOff = FALSE,

theme.bw = TRUE,

background = "transparent")

```

## The factor model of counterfactuals

Both estimators target the same object — the counterfactual matrix

$Y(0)$ of what each county's log teen employment *would* have been

absent any minimum-wage increase. Where they differ is in how they

restrict that matrix.

**IFEct** imposes the explicit factor decomposition $Y_{it}(0) =

\alpha_i + \xi_t + \lambda_i' f_t + \varepsilon_{it}$, fits

$(\alpha, \xi, \Lambda, F)$ on the **control** observations only,

and uses those estimates to impute $Y_{it}(0)$ for treated

cells. The choice of $r$ — how many factors — is made by

cross-validation: hold out small blocks of control cells, refit,

score by MSPE on the held-out cells [@xu2017generalized;

@liu2024practical].

**MC** does not write the factor model down. It assumes only that

the matrix of $Y(0)$ outcomes is **approximately low rank**, then

completes it by minimising a Frobenius-norm fit penalty *plus* a

nuclear-norm penalty on the singular values. Nuclear-norm

regularisation is the convex relaxation of "low rank" the same way

$\ell_1$ is the convex relaxation of "sparse" [@athey2021matrix].

The penalty weight $\lambda$ plays the role of $r$ and is again

chosen by cross-validation.

The key practical implication: both methods bake in

**unit-specific time trends** automatically, without you having to

specify which units or which trend shapes. Parallel trends becomes

a special case (the $r = 0$ corner of IFEct, or the limit

$\lambda \to \infty$ in MC) rather than an assumption.

## Estimating with FECT

The two fits below cap the rank grid at $r \in \{0, 1, 2\}$. With

only 7 calendar years and 3 pre-periods on the shorter cohort, any

$r$ larger than that would be statistical fantasy.

The bootstrap (`nboots = 200`) is the dominant cost; both chunks

cache to `_freeze/` so subsequent renders skip them.

```{r}

#| label: fit-ife

#| message: false

#| warning: false

out_ife <- fect(

lemp ~ D, data = as.data.frame(mw),

index = c("id", "year"),

method = "ife",

force = "two-way",

CV = TRUE,

r = 0:2,

min.T0 = 2,

cv.nobs = 2,

cv.donut = 0,

se = TRUE,

nboots = 200,

parallel = TRUE,

seed = 42

)

```

```{r}

#| label: fit-mc

#| message: false

#| warning: false

out_mc <- fect(

lemp ~ D, data = as.data.frame(mw),

index = c("id", "year"),

method = "mc",

force = "two-way",

CV = TRUE,

min.T0 = 2,

cv.nobs = 2,

cv.donut = 0,

se = TRUE,

nboots = 200,

parallel = TRUE,

seed = 42

)

```

```{r}

#| label: tbl-cv

#| tbl-cap: "Hyperparameters selected by cross-validation. IFEct picks the number of latent factors $r$; MC picks the nuclear-norm penalty weight $\\lambda$."

tibble(

Method = c("IFEct", "MC"),

`CV-selected` = c(paste0("r = ", unname(out_ife$r.cv)),

sprintf("lambda = %.4f", out_mc$lambda.cv))

) |>

gt_pretty()

```

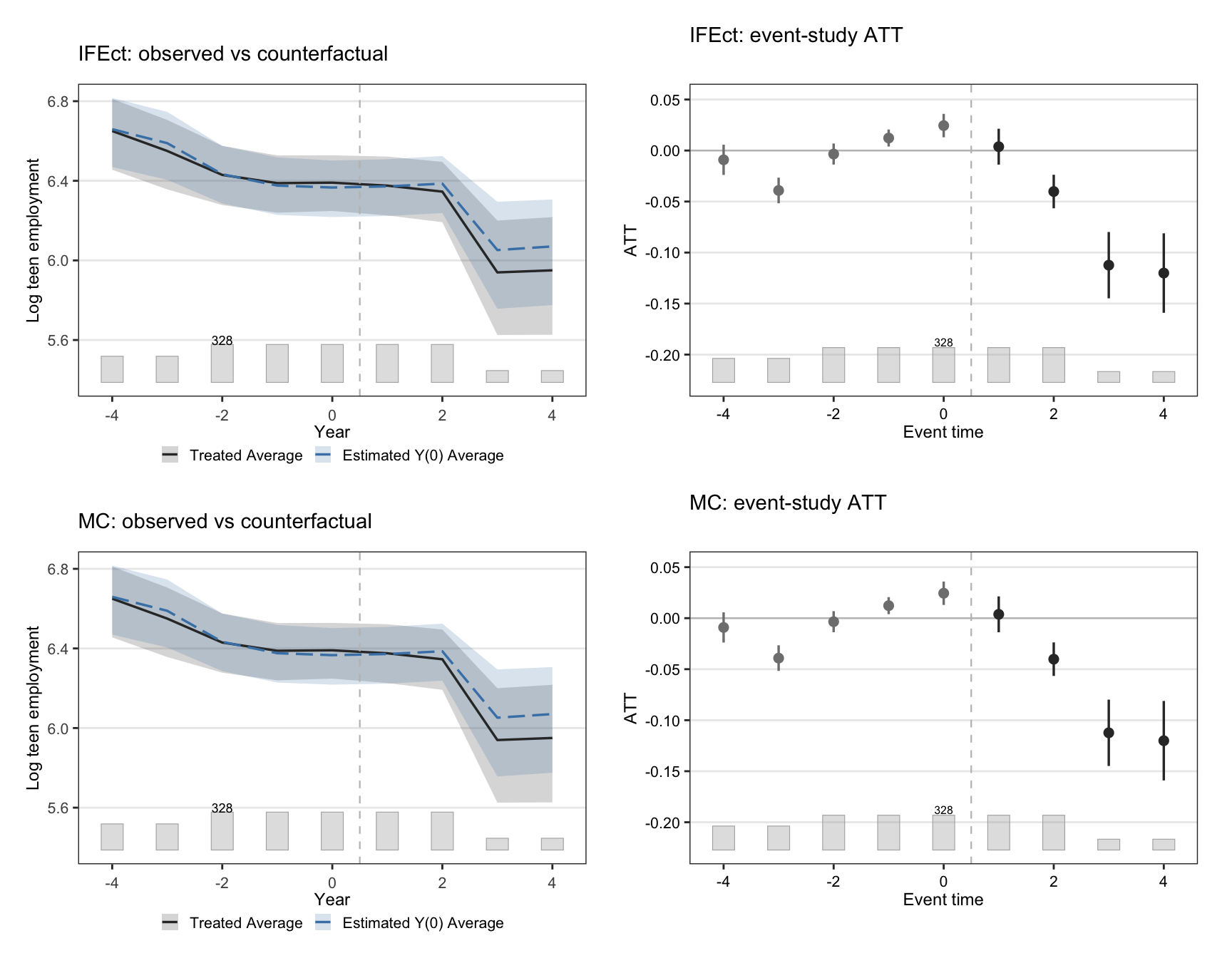

## Counterfactual paths and the ATT trajectory

The signature FECT figure overlays the observed average outcome on

treated units against the model-implied $Y(0)$, then plots the gap

— the ATT path — by event time. A credible factor model should

track the observed $Y$ closely before treatment and only diverge

after.

```{r}

#| label: fig-ife-mc

#| fig-cap: "Counterfactual trajectories and event-study ATT. Top row: IFEct. Bottom row: MC. Left panels overlay observed average outcome on treated units (solid) with model-implied $Y(0)$ (dashed). Right panels show the implied ATT by event time relative to a county's adoption year, with bootstrap 95% CIs."

#| fig-width: 9

#| fig-height: 7

p_ife_ct <- plot(out_ife, type = "counterfactual",

main = "IFEct: observed vs counterfactual",

xlab = "Year", ylab = "Log teen employment")

p_ife_gap <- plot(out_ife, type = "gap",

main = "IFEct: event-study ATT",

xlab = "Event time", ylab = "ATT")

p_mc_ct <- plot(out_mc, type = "counterfactual",

main = "MC: observed vs counterfactual",

xlab = "Year", ylab = "Log teen employment")

p_mc_gap <- plot(out_mc, type = "gap",

main = "MC: event-study ATT",

xlab = "Event time", ylab = "ATT")

(p_ife_ct + p_ife_gap) / (p_mc_ct + p_mc_gap)

```

Both estimators reproduce the textbook story: a flat-ish pre-trend

that breaks downward at event time zero. The MC counterfactual is a

touch smoother than IFEct's, which is the regularisation doing its

job.

## F-test for zero pre-trend

The factor structure does not *guarantee* the pre-treatment ATTs

are zero — it only *allows* them to be by absorbing unit-specific

trends. We test the no-anticipation / good-fit assumption directly

with a joint F-test on the pre-treatment ATTs returned by `fect`

(`wald = TRUE` under the hood).

```{r}

#| label: tbl-ftest

#| tbl-cap: "Wald F-test that all pre-treatment ATTs are jointly zero. Large p-values mean the factor structure absorbs pre-trends well; small p-values flag residual pre-trend a single $r$ or $\\lambda$ choice could not iron out."

ftest_row <- function(out, label) {

tibble(

Estimator = label,

`F stat` = out$test$f.stat,

df1 = out$test$df1,

df2 = out$test$df2,

`p-value` = out$test$f.p

)

}

bind_rows(

ftest_row(out_ife, "IFEct"),

ftest_row(out_mc, "MC")

) |>

gt_pretty(decimals = 4)

```

## Side-by-side: CS, IFEct, MC

The punchline. We recompute Callaway-Sant'Anna's overall ATT on

*this same panel* (2001-2007 window) so the three estimates are

directly comparable, then collect them in one table.

```{r}

#| label: cs-fit

#| message: false

#| warning: false

attgt_ch10 <- did::att_gt(

yname = "lemp", idname = "id", gname = "G", tname = "year",

data = as.data.frame(mw),

control_group = "nevertreated",

base_period = "universal"

)

cs_overall <- did::aggte(attgt_ch10, type = "group")

```

```{r}

#| label: tbl-compare

#| tbl-cap: "Three estimands, three identifying assumptions, one panel. The Callaway-Sant'Anna row is the chapter 9 estimator recomputed on the 2001-2007 window. IFEct and MC ATTs are FECT's average treatment effect on the treated, averaged across all post-treatment cells."

fect_att <- function(out) {

list(

est = out$att.avg,

se = out$est.avg[, "S.E."],

lo = out$est.avg[, "CI.lower"],

hi = out$est.avg[, "CI.upper"]

)

}

ife <- fect_att(out_ife)

mc <- fect_att(out_mc)

tibble(

Estimator = c("Callaway-Sant'Anna overall ATT",

"IFEct (Xu 2017)",

"Matrix Completion (Athey et al. 2021)"),

Estimate = c(cs_overall$overall.att, ife$est, mc$est),

SE = c(cs_overall$overall.se, ife$se, mc$se),

`CI lower` = c(cs_overall$overall.att - 1.96 * cs_overall$overall.se,

ife$lo, mc$lo),

`CI upper` = c(cs_overall$overall.att + 1.96 * cs_overall$overall.se,

ife$hi, mc$hi),

`Identifying assumption` = c(

"Conditional parallel trends",

"Linear factor model of Y(0)",

"Approximately low-rank Y(0)"

)

) |>

gt_pretty(decimals = 4)

```

Three estimators that disagree about the assumption point to the

same sign and the same order of magnitude. Quantitatively the CS and

factor-based estimates need not match: CS averages cohort-specific

clean 2×2 contrasts under parallel trends; IFEct and MC impute the

treated cells of a factor model. When they diverge, the gap

quantifies how much of CS's estimate was riding on parallel trends

versus on cohort heterogeneity that a factor model can soak up.

When they agree — as they roughly do here — both assumptions are

consistent with the same conclusion, which is the strongest evidence

a panel design can produce.

::: {.callout-warning appearance="simple"}

**The short-panel caveat.** With $T = 7$ and 3 pre-periods on the

shorter cohort, the rank/penalty selected by cross-validation is

borderline-identifiable. We capped $r \le 2$ deliberately. On a

genuinely short panel ($T \le 5$, which is chapter 9's working

window) IFE and MC become numerically delicate and the F-test loses

power against subtle pre-trend departures. The honest move when the

panel is too short is to *not* run these estimators rather than to

hand-pick a rank. The `fect::simdata` panel in the package ships a

$T = 30$ case that lets you see the methods working at full strength

(see exercise 1).

:::

## Recap

::: {.callout-note appearance="simple"}

**The methods reconciled.** Three answers to the same question on

the 2001-2007 minimum-wage panel:

- *Callaway-Sant'Anna overall ATT*: clean 2×2 contrasts, weighted

to cohort size, under parallel trends.

- *IFEct*: factor model of $Y(0)$ fit on never-treated, imputed on

treated, $r$ chosen by cross-validation.

- *Matrix Completion*: low-rank completion of the masked $Y(0)$

matrix, nuclear-norm penalty $\lambda$ chosen by cross-validation.

All three point downward; all three sit in the same neighbourhood;

none is uniquely correct. The factor-based estimators *relax*

parallel trends rather than replace it, and the F-tests on

pre-treatment ATTs are the quality check for whether that relaxation

bought you anything.

:::

## Common pitfall

Cranking $r$ up until the in-sample fit looks great. With a panel

this short, an IFEct model with $r$ near $T/2$ will fit the pre-

treatment cells almost perfectly *and* produce an absurd

counterfactual on the treated cells, because it has fitted noise

into the loadings. Trust the CV-selected rank and the F-test, not

the eyeballed pre-trend match. The MC equivalent is choosing

$\lambda$ too small; the symptom is the same. Both are over-fitting

masquerading as identification.

## Further reading

The factor-model formulation traces to @bai2009panel; the

generalised synthetic control / IFEct interpretation that powers

`fect`'s implementation is @xu2017generalized. The matrix-completion

view, including theoretical guarantees and the nuclear-norm penalty,

is @athey2021matrix. @liu2024practical is the practical-guide paper

that pairs with the `fect` package and walks through model

diagnostics in depth; its online companion at

<https://yiqingxu.org/packages/fect/04-ife-mc.html> is the

authoritative tutorial.

## Exercises

1. The `fect::simdata` dataset is a $T = 30$ simulated panel with a

known factor structure. Fit IFEct on it with arguments

`CV = TRUE, r = 0:4` and confirm that cross-validation recovers

the true rank. Compare

`out$r.cv` against the simulation's true $r$ (documented in

`?simdata`).

2. Re-fit `out_ife` and `out_mc` on chapter 9's narrower 2003-2007

window. Which estimator degrades more visibly when pre-period

length is cut? Why?

3. Run `fect(..., placeboTest = TRUE, placebo.period = c(-2, -1))`

to hide the last two pre-treatment periods, refit, and check that

the implied ATT on the hidden window is statistically zero. What

does a non-zero placebo result imply about the credibility of the

chapter's headline ATT?