---

title: 3. The Sample Mean

execute:

enabled: true

warning: false

---

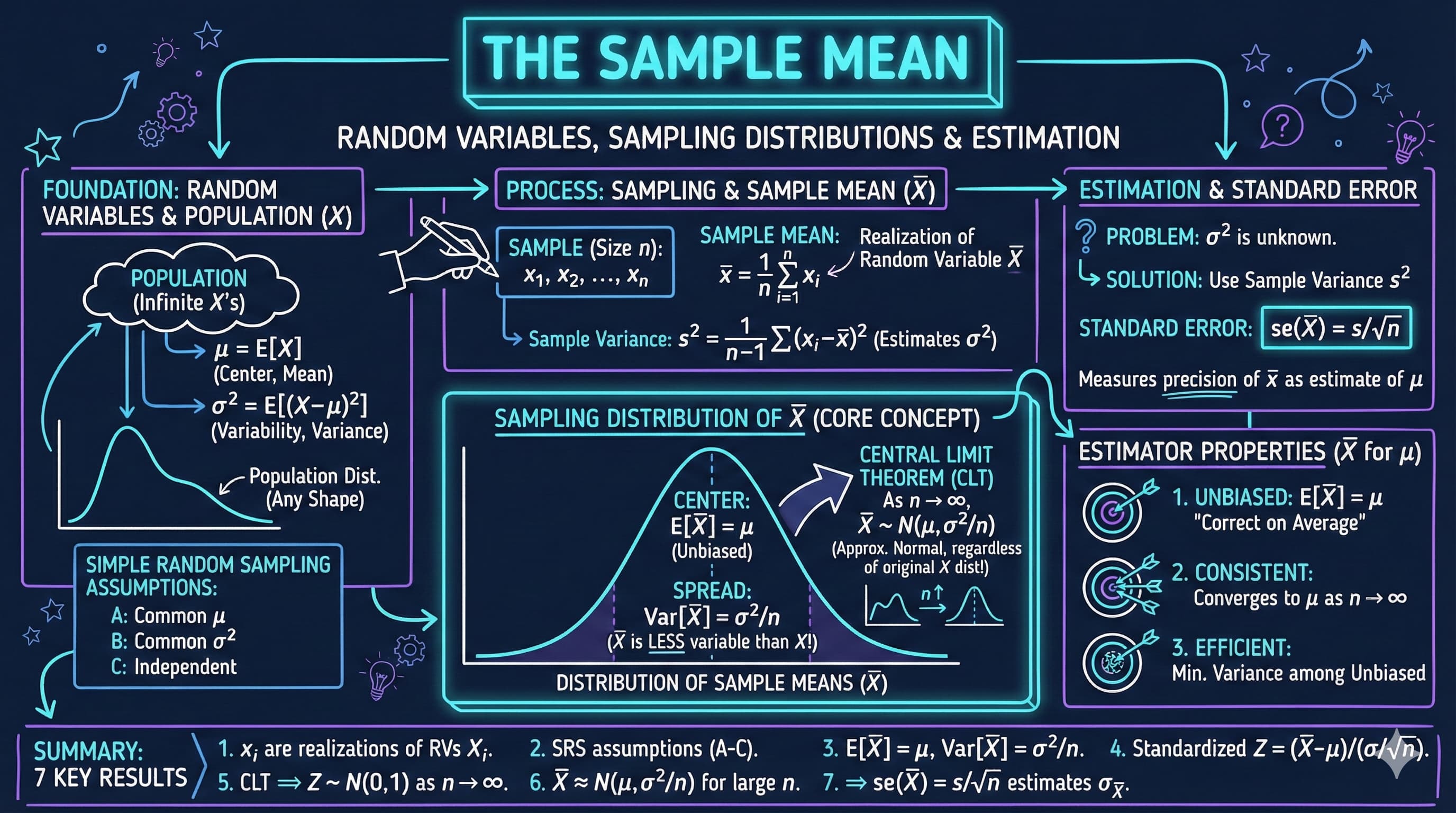

**metricsAI: An Introduction to Econometrics with Python and AI in the Cloud**

*[Carlos Mendez](https://carlos-mendez.org)*

<img src="https://raw.githubusercontent.com/quarcs-lab/metricsai/main/images/ch03_visual_summary.jpg" alt="Chapter 03 Visual Summary" width="100%">

This notebook provides an interactive introduction to one of the most important concepts in statistics: the **sampling distribution of the sample mean**. You'll explore how sample means behave through experiments and simulations, building intuition for the Central Limit Theorem. All code runs directly in Google Colab without any local setup.

[](https://colab.research.google.com/github/quarcs-lab/metricsai/blob/main/notebooks_colab/ch03_The_Sample_Mean.ipynb)

<div class="chapter-resources">

<a href="https://www.youtube.com/watch?v=pnv9ff_3hrI" target="_blank" class="resource-btn">🎬 AI Video</a>

<a href="https://carlos-mendez.my.canva.site/s03-the-sample-mean-pdf" target="_blank" class="resource-btn">✨ AI Slides</a>

<a href="https://cameron.econ.ucdavis.edu/aed/traedv1_03" target="_blank" class="resource-btn">📊 Cameron Slides</a>

<a href="https://app.edcafe.ai/quizzes/697864e12f5d08069e0471b5" target="_blank" class="resource-btn">✏️ Quiz</a>

<a href="https://app.edcafe.ai/chatbots/69789d252f5d08069e06fdad" target="_blank" class="resource-btn">🤖 AI Tutor</a>

</div>

## Chapter Overview

This chapter bridges the gap between descriptive statistics (Chapter 2) and inferential statistics (Chapter 4). The key insight: when we calculate a sample mean $\bar{x}$ from data, we're observing one realization of a **random variable** $\bar{X}$ that has its own probability distribution.

**What you'll learn:**

- Understand sample values as realizations of random variables

- Derive the mean and variance of the sample mean: $E[\bar{X}] = \mu$, $Var[\bar{X}] = \sigma^2/n$

- Explore the **sampling distribution** of $\bar{X}$ through experiments

- Discover the **Central Limit Theorem**: $\bar{X}$ is approximately normal for large $n$

- Learn properties of good estimators (unbiasedness, efficiency, consistency)

- Compute the **standard error** of the mean: $se(\bar{X}) = s/\sqrt{n}$

**Datasets used:**

- **AED_COINTOSSMEANS.DTA**: 400 sample means from coin toss experiments (n=30 each)

- **AED_CENSUSAGEMEANS.DTA**: 100 sample means from 1880 U.S. Census ages (n=25 each)

**Key economic relevance:**

This chapter provides the theoretical foundation for ALL statistical inference in economics. Whether estimating average income, unemployment rates, or regression coefficients, understanding the sampling distribution of $\bar{X}$ is essential.

**Chapter outline:**

- 3.1 Random Variables

- 3.2 Experiment: Coin Tosses

- 3.3 Properties of the Sample Mean

- 3.4 Real Data Example - 1880 U.S. Census

- 3.5 Estimator Properties

- 3.6 Computer Simulation of Random Samples

- 3.7 Samples other than Simple Random Samples

## Key Concepts

Six core ideas anchor this chapter. Skim them before you start, and come back when a term feels fuzzy. Each entry pairs a concrete example using the chapter's data with a non-technical analogy. Click a panel to expand it.

**Population Parameter vs. Sample Statistic:** A population parameter is a fixed number describing the entire population that we typically never observe directly, like $\mu$ or $\sigma$. A sample statistic is a number we compute from one drawn sample, like $\bar{x}$ or $s$, and it changes from sample to sample.

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

For 1880 U.S. Census ages, the population parameter is $\mu = 24.13$ years (computed once from all 50,169,452 records). When researchers draw a sample of $n = 25$ people they compute one sample statistic — say $\bar{x} = 27.84$ years (the first of the chapter's 100 census samples). Across 100 such samples, the statistics range from 14.6 to 33.4 years even though $\mu$ never changes.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

A population parameter is the published recipe for a cake — written down once and fixed forever. A sample statistic is the cake one baker actually pulls from the oven tonight: a little drier, a little sweeter, a little different from every other baker's cake. The recipe is the truth; each cake is one noisy realization of it.

:::

::::

:::::

**Estimator:** A rule or formula that takes a sample and returns a number meant to approximate a population parameter. The sample mean $\bar{X} = \tfrac{1}{n}\sum X_i$ is an estimator of $\mu$. An *estimate* is the specific number that comes out when we feed the rule one specific sample.

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

In ch03, $\bar{X}$ is the estimator. Feed it the first 30 coin-toss outcomes and it returns the estimate $\bar{x} = 0.40$. Feed it a different 30 tosses and it returns $0.53$, then $0.47$, and so on — across the 400 simulated samples we get 400 different estimates from one estimator, with mean $0.5004$ and SD $0.0887$.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

An estimator is sheet music for a song; an estimate is the recording made by one orchestra on one night. The same sheet music can produce thousands of recordings, each a little different in tempo and emphasis, but all generated by the same underlying rule. Don't confuse the score with any single performance of it.

:::

::::

:::::

**Unbiasedness:** A property meaning the estimator's expected value equals the parameter it targets, with no systematic over- or under-shooting. The sample mean is unbiased for $\mu$ because $E[\bar{X}] = \mu$.

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

Across the 400 simulated coin-toss samples ($n = 30$, $\mu = 0.5$), the average of all sample means is $0.5004$ — almost exactly the true $\mu$. Across the 100 census-age samples ($n = 25$, $\mu = 24.13$ years), the average of the sample means is $23.78$ years — within $0.4$ of the truth even though individual means range from $14.6$ to $33.4$.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

An unbiased archer fires a hundred arrows: each one lands somewhere off-target due to wind and tremor, but their *average* position is exactly the bullseye. The archer doesn't pull left or right systematically — only the unavoidable jitter of small disturbances. That's $\bar{X}$ around $\mu$.

:::

::::

:::::

**Efficiency:** Among all unbiased estimators, the one with the smallest variance is called efficient. The sample mean $\bar{X}$ is efficient for $\mu$ in many common settings (Bernoulli, normal, Poisson) — its sample-to-sample bounce is as small as theory allows.

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

For the coin toss ($\sigma^2 = 0.25$, $n = 30$), the sample mean has $\operatorname{Var}[\bar{X}] = 0.0083$ and standard deviation $\sigma/\sqrt{n} = 0.0913$. Any rival unbiased estimator — like keeping only the first toss, or averaging just the first and last — would have a wider sample-to-sample swing than this; the simulation's empirical SD of $0.0887$ closely matches the theoretical floor.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

A sharp camera lens and a foggy lens both centre on the same subject (no bias), but the sharp lens produces a tight, crisp image while the foggy lens smears across the frame. Efficiency is the optical quality of an estimator: same target, smallest blur, no detail wasted.

:::

::::

:::::

**Consistency:** A property meaning the estimator gets arbitrarily close to the parameter as the sample size grows. For $\bar{X}$, this follows from $\operatorname{Var}[\bar{X}] = \sigma^2/n \to 0$ as $n \to \infty$ — the bounce shrinks without limit.

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

With census ages ($\sigma = 18.61$ years), the standard deviation of $\bar{X}$ is $3.72$ at $n = 25$, but only $1.86$ at $n = 100$, $0.83$ at $n = 500$, and $0.26$ at $n = 5{,}000$. By the time $n$ approaches the size of the full 1880 census, $\bar{X}$ is glued to $\mu = 24.13$ within hundredths of a year.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

A GPS receiver is consistent for your location when its accuracy improves as you collect more satellite pings — at one ping you're "somewhere in the city", at fifty pings "on this street", at five hundred pings "at this house". The error doesn't merely become small on average; it shrinks all the way to zero given enough data.

:::

::::

:::::

**Law of Large Numbers:** A foundational result stating that as $n \to \infty$, the sample mean $\bar{X}$ converges to the population mean $\mu$ with near certainty. It is the formal guarantee behind consistency for $\bar{X}$.

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

With $n = 30$ coin tosses, individual simulated sample means range from $0.27$ to $0.77$ across the 400 simulations — strikingly far from $\mu = 0.5$ on the noisy days. Push to $n = 1{,}000$ and the typical deviation shrinks more than fivefold; at $n = 1{,}000{,}000$ it is a mere $0.0005$. The Law of Large Numbers promises this convergence is mathematically guaranteed, not lucky.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

A casino's roulette wheel keeps about five cents of every dollar wagered in expectation. One night a single gambler may win big or lose big, but the casino — playing the wheel a million times a year — pockets almost exactly the expected house edge. The Law of Large Numbers is why casinos always win in the long run: averages drift inevitably toward their expected value as the count grows.

:::

::::

:::::

## Setup

First, we import the necessary Python packages and configure the environment for reproducibility. All data will stream directly from GitHub.

```{python}

#| code-fold: true

#| code-summary: "Setup: Import libraries and configure environment"

# --- Libraries ---

import numpy as np # numerical operations

import pandas as pd # data manipulation

import matplotlib.pyplot as plt # plotting

import seaborn as sns # statistical visualizations

from scipy import stats # statistical functions

import random

import os

# --- Reproducibility ---

RANDOM_SEED = 42

random.seed(RANDOM_SEED)

np.random.seed(RANDOM_SEED)

os.environ['PYTHONHASHSEED'] = str(RANDOM_SEED)

# --- Data source ---

GITHUB_DATA_URL = "https://raw.githubusercontent.com/quarcs-lab/data-open/master/AED/"

# --- Plotting style ---

plt.style.use('dark_background')

sns.set_style("darkgrid")

plt.rcParams.update({

'axes.facecolor': '#1a2235',

'figure.facecolor': '#12162c',

'grid.color': '#3a4a6b',

'figure.figsize': (10, 6),

'text.color': 'white',

'axes.labelcolor': 'white',

'xtick.color': 'white',

'ytick.color': 'white',

'axes.edgecolor': '#1a2235',

})

print("Setup complete! Ready to explore the sample mean.")

```

## 3.1 Random Variables

A **random variable** is a variable whose value is determined by the outcome of an experiment. The connection between data and randomness:

- **Random variable notation:** $X$ (uppercase) represents the random variable

- **Realized value notation:** $x$ (lowercase) represents the observed value

**Example - Coin Toss:**

- Experiment: Toss a fair coin

- Random variable: $X = 1$ if heads, $X = 0$ if tails

- Each outcome has probability 0.5

**Key properties:**

**Mean (Expected Value):**

$$\mu = E[X] = \sum_x x \cdot Pr[X = x]$$

For fair coin: $\mu = 0 \times 0.5 + 1 \times 0.5 = 0.5$

**Variance:**

$$\sigma^2 = E[(X - \mu)^2] = \sum_x (x - \mu)^2 \cdot Pr[X = x]$$

For fair coin: $\sigma^2 = (0-0.5)^2 \times 0.5 + (1-0.5)^2 \times 0.5 = 0.25$

**Standard Deviation:** $\sigma = \sqrt{0.25} = 0.5$

Let's verify these formulas in code — first for the fair coin, then for an unfair coin with $p = 0.6$. Notice that the unfair coin has a higher mean but a slightly *lower* variance: outcomes become more predictable when one side dominates.

```{python}

# Coin toss random variable

# Fair coin properties

print("Fair coin (p = 0.5):")

mu_fair = 0 * 0.5 + 1 * 0.5

var_fair = (0 - mu_fair)**2 * 0.5 + (1 - mu_fair)**2 * 0.5

sigma_fair = np.sqrt(var_fair)

print(f" Mean (μ): {mu_fair:.4f}")

print(f" Variance (σ²): {var_fair:.4f}")

print(f" Standard deviation (σ): {sigma_fair:.4f}")

# Unfair coin for comparison

print("\nUnfair coin (p = 0.6 for heads):")

mu_unfair = 0 * 0.4 + 1 * 0.6

var_unfair = (0 - mu_unfair)**2 * 0.4 + (1 - mu_unfair)**2 * 0.6

sigma_unfair = np.sqrt(var_unfair)

print(f" Mean (μ): {mu_unfair:.4f}")

print(f" Variance (σ²): {var_unfair:.4f}")

print(f" Standard deviation (σ): {sigma_unfair:.4f}")

```

> **Key Concept 3.1: Random Variables**

>

> A random variable $X$ is a variable whose value is determined by the outcome of an unpredictable experiment. The mean $\mu = \mathrm{E}[X]$ is the probability-weighted average of all possible values, while the variance $\sigma^2 = \mathrm{E}[(X-\mu)^2]$ measures variability around the mean. These population parameters characterize the distribution from which we draw samples.

## 3.2 Experiment: Coin Tosses

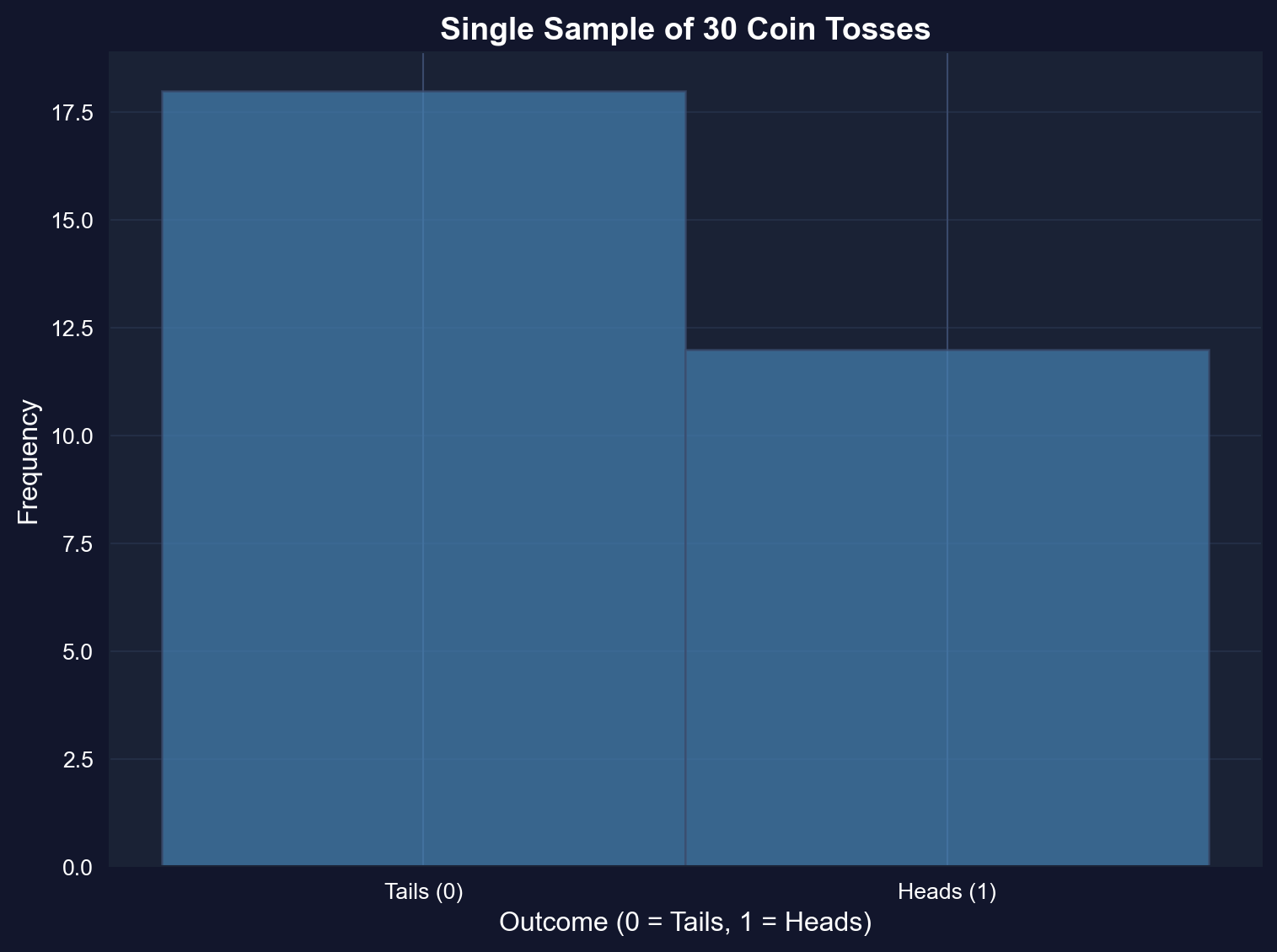

### One Sample

Now we conduct an actual experiment: toss a coin 30 times and record the results. This gives us a **sample** of size $n = 30$.

**Key insight:** The observed values $x_1, x_2, ..., x_{30}$ are realizations of random variables $X_1, X_2, ..., X_{30}$.

The **sample mean** is:

$$\bar{x} = \frac{1}{n}\sum_{i=1}^n x_i$$

This $\bar{x}$ is itself a realization of the random variable:

$$\bar{X} = \frac{1}{n}\sum_{i=1}^n X_i$$

```{python}

# Generate single sample of 30 coin tosses

np.random.seed(10101)

u = np.random.uniform(0, 1, 30)

x = np.where(u > 0.5, 1, 0) # 1 if heads, 0 if tails

# Single coin toss sample (n = 30)

print(f"Number of heads (x=1): {np.sum(x)}")

print(f"Number of tails (x=0): {np.sum(1-x)}")

print(f"Sample mean (x̄): {np.mean(x):.4f}")

print(f"Sample std dev (s): {np.std(x, ddof=1):.4f}")

print(f"\nPopulation values:")

print(f" Population mean (μ): 0.5000")

print(f" Population std (σ): 0.5000")

# Visualize single sample

fig, ax = plt.subplots(figsize=(8, 6))

ax.hist(x, bins=[-0.5, 0.5, 1.5], edgecolor='#3a4a6b', alpha=0.7, color='steelblue') # bin edges center bars on 0 and 1

ax.set_xlabel('Outcome (0 = Tails, 1 = Heads)', fontsize=12)

ax.set_ylabel('Frequency', fontsize=12)

ax.set_title('Single Sample of 30 Coin Tosses',

fontsize=14, fontweight='bold')

ax.set_xticks([0, 1])

ax.set_xticklabels(['Tails (0)', 'Heads (1)'])

ax.grid(True, alpha=0.3, axis='y')

plt.tight_layout()

plt.show()

# This is just ONE realization of the random variable X-bar.

# To understand its distribution, we need MANY samples...

```

> **Key Concept 3.2: Sample Mean as Random Variable**

>

> The observed sample mean $\bar{x}$ is a realization of the random variable $\bar{X} = (X_1 + \cdots + X_n)/n$. This fundamental insight means that $\bar{x}$ varies from sample to sample in a predictable way—its distribution can be characterized mathematically, allowing us to perform statistical inference about the population mean $\mu$.

**Key findings from our coin toss experiment (n = 30):**

**1. Sample mean = 0.4000 (vs. theoretical μ = 0.5)**

- We got 12 heads and 18 tails (40% vs. expected 50%)

- This difference (0.10 or 10 percentage points) is completely normal

- With only 30 tosses, random variation of this magnitude is expected

- If we flipped 1000 times, we'd expect to get much closer to 50%

**2. Sample standard deviation = 0.4983 (vs. theoretical σ = 0.5000)**

- Nearly perfect match with population value

- This confirms the theoretical formula: σ² = p(1-p) = 0.5(0.5) = 0.25, so σ = 0.5

**3. Why the sample mean differs from 0.5:**

- The sample mean x̄ is itself a random variable

- Just like one coin toss doesn't always give heads, one sample mean doesn't always equal μ

- This single value (0.4000) is one realization from the sampling distribution of X̄

- The next experiment would likely give a different value (maybe 0.4667 or 0.5333)

**Economic interpretation:** When we estimate average income from a survey or unemployment rate from a sample, we get one realization that will differ from the true population value. Understanding this variability is the foundation of statistical inference.

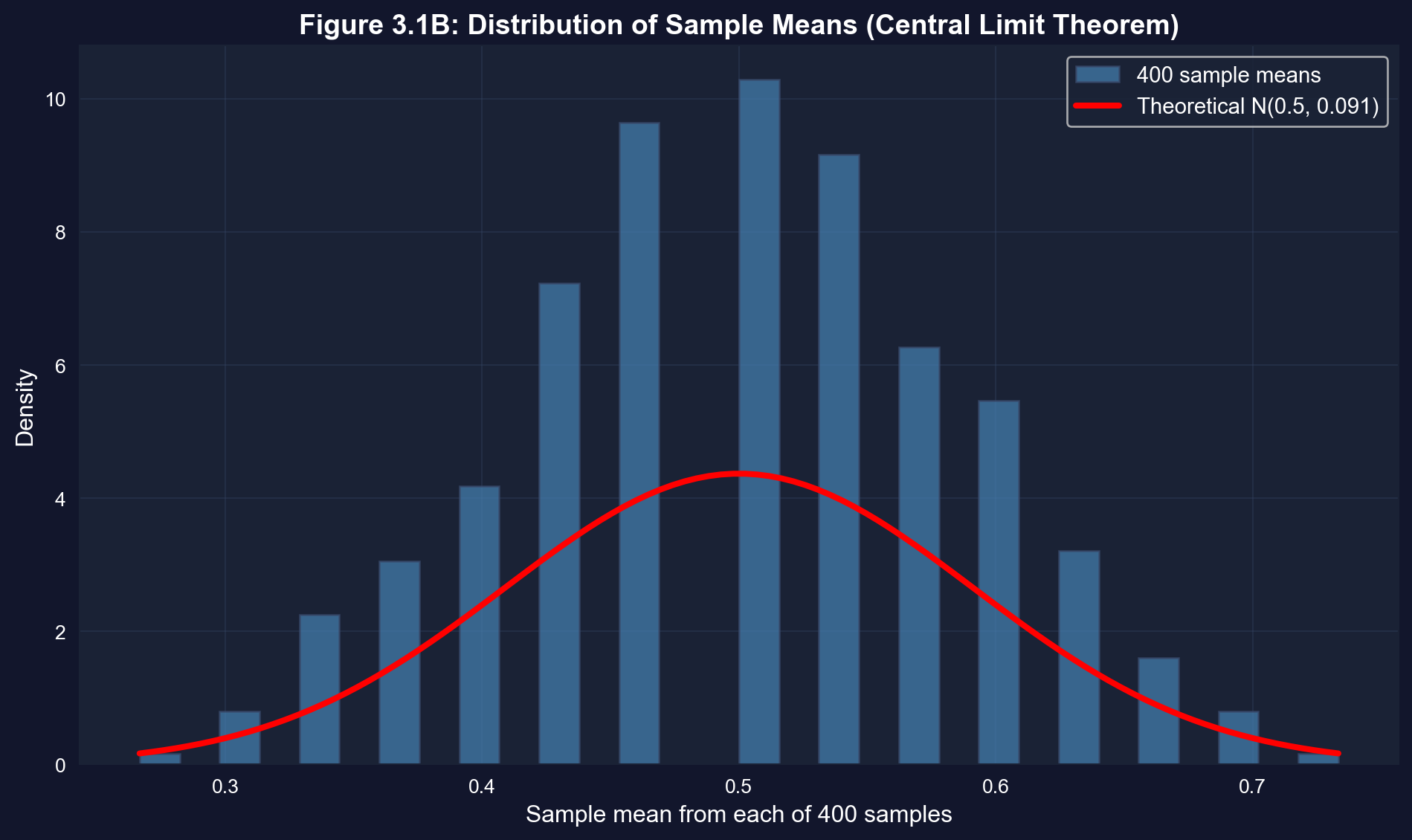

### 400 Samples and The Distribution of Sample Means

To understand the **sampling distribution** of $\bar{X}$, we repeat the experiment 400 times:

- Each experiment: 30 coin tosses → one sample mean $\bar{x}_i$

- After 400 experiments: we have 400 sample means ($\bar{x}_1, \bar{x}_2, ..., \bar{x}_{400}$)

- The histogram of these 400 values approximates the **sampling distribution** of $\bar{X}$

**What we expect to see:**

- Sample means centered near $\mu = 0.5$ (population mean)

- Much less variability than individual coin tosses

- Approximately normal distribution (Central Limit Theorem!)

```{python}

# Load precomputed coin toss means data (400 samples of size 30)

data_cointoss = pd.read_stata(GITHUB_DATA_URL + 'AED_COINTOSSMEANS.DTA')

# 400 coin toss experiments (each n = 30)

xbar = data_cointoss['xbar']

# Summary of 400 sample means

display(data_cointoss.describe())

print(f"First 5 sample means: {xbar.head().tolist()}")

print(f"Mean of the 400 sample means: {xbar.mean():.4f}")

print(f"Std dev of the 400 sample means: {xbar.std():.4f}")

# Theoretical predictions

print(f"\nE[X-bar] = mu = 0.5000")

print(f"sigma(X-bar) = sigma/sqrt(n) = sqrt(0.25/30) = {np.sqrt(0.25/30):.4f}")

# Comparison

print(f"\nEmpirical mean: {xbar.mean():.4f} vs Theoretical: 0.5000")

print(f"Empirical std: {xbar.std():.4f} vs Theoretical: {np.sqrt(0.25/30):.4f}")

```

**Key findings from 400 coin toss experiments:**

**1. Mean of sample means = 0.4994 (vs. theoretical μ = 0.5)**

- This demonstrates **unbiasedness**: E[X̄] = μ

- The tiny difference (0.0006) is just random variation

- With more replications, this would get even closer to 0.5

- On average across many samples, X̄ equals the true population mean

**2. Standard deviation of sample means = 0.0863 (vs. theoretical = 0.0913)**

- The theoretical standard error is σ/√n = 0.5/√30 = 0.0913

- Our empirical SD (0.0863) is very close to this prediction

- This confirms the variance formula: Var(X̄) = σ²/n works in practice

**3. Range of sample means: 0.2667 to 0.7333**

- Individual sample means vary considerably (from 26.7% to 73.3% heads)

- This shows why we need statistical theory - any single sample could be misleading

- But the distribution is predictable and centered correctly

**4. Comparison with single coin tosses:**

- Individual coin tosses have σ = 0.5

- Sample means have σ(X̄) = 0.0863

- Sample means are 5.8× less variable than individual tosses

- This is the power of averaging: √30 ≈ 5.5

**Economic interpretation:** When estimating economic parameters (average wage, inflation rate, GDP growth), individual survey responses vary widely, but the sample mean is much more precise. The standard error tells us exactly how much precision we gain from our sample size.

### Visualizing the Sampling Distribution of $\bar{X}$

The histogram below shows the distribution of the 400 sample means. Notice:

1. **Center:** Near 0.5 (the population mean $\mu$)

2. **Spread:** Much narrower than the original population (σ = 0.5)

3. **Shape:** Approximately bell-shaped (normal distribution)

The red curve is the **theoretical normal distribution** with mean $\mu = 0.5$ and standard deviation $\sigma/\sqrt{n} = 0.091$.

```{python}

# Visualize distribution of sample means

fig, ax = plt.subplots(figsize=(10, 6))

# Histogram of 400 sample means

n_hist, bins, patches = ax.hist(xbar, bins=30, density=True,

edgecolor='#3a4a6b', alpha=0.7, color='steelblue',

label='400 sample means')

# Overlay theoretical normal distribution

xbar_range = np.linspace(xbar.min(), xbar.max(), 100)

theoretical_pdf = stats.norm.pdf(xbar_range, 0.5, np.sqrt(0.25/30))

ax.plot(xbar_range, theoretical_pdf, 'r-', linewidth=3,

label=f'Theoretical N(0.5, {np.sqrt(0.25/30):.3f})')

ax.set_xlabel('Sample mean from each of 400 samples', fontsize=12)

ax.set_ylabel('Density', fontsize=12)

ax.set_title('Figure 3.1B: Distribution of Sample Means (Central Limit Theorem)',

fontsize=14, fontweight='bold')

ax.legend(fontsize=11)

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

```

## 3.3 Properties of the Sample Mean

Under the assumption of a **simple random sample** where:

- A. Each $X_i$ has common mean: $E[X_i] = \mu$

- B. Each $X_i$ has common variance: $Var[X_i] = \sigma^2$

- C. The $X_i$ are statistically independent

We can mathematically prove:

**Mean of the sample mean:**

$$E[\bar{X}] = \mu$$

This says $\bar{X}$ is **unbiased** for $\mu$ (its expected value equals the parameter we're estimating).

**Variance of the sample mean:**

$$Var[\bar{X}] = \frac{\sigma^2}{n}$$

**Standard deviation of the sample mean:**

$$SD[\bar{X}] = \frac{\sigma}{\sqrt{n}}$$

**Key insights:**

1. As sample size $n$ increases, $Var[\bar{X}]$ decreases ($\propto 1/n$)

2. Larger samples give more precise estimates (smaller variability)

3. Standard deviation decreases at rate $1/\sqrt{n}$ (to halve uncertainty, need 4× the sample size)

```{python}

# How sample size affects precision

# For coin toss: mu = 0.5, sigma^2 = 0.25, sigma = 0.5

mu = 0.5

sigma = 0.5

sigma_sq = 0.25

sample_sizes = [10, 30, 100, 400, 1000]

print(f"Population: mu = {mu}, sigma = {sigma}")

print(f"\n{'n':<10} {'sigma(X-bar)':<20} {'Var(X-bar)':<20}")

for n in sample_sizes:

sd_xbar = sigma / np.sqrt(n)

var_xbar = sigma_sq / n

print(f"{n:<10} {sd_xbar:<20.6f} {var_xbar:<20.6f}")

# Key observation: Doubling n reduces sigma(X-bar) by factor of sqrt(2) ~ 1.41

# To halve uncertainty, need to quadruple sample size.

```

> **Key Concept 3.3: Properties of the Sample Mean**

>

> Under simple random sampling (common mean $\mu$, common variance $\sigma^2$, independence), the sample mean $\bar{X}$ has mean $\mathrm{E}[\bar{X}] = \mu$ (unbiased) and variance $\operatorname{Var}[\bar{X}] = \sigma^2/n$ (decreases with sample size). The standard deviation $\sigma_{\bar{X}} = \sigma/\sqrt{n}$ shrinks as $n$ increases, meaning larger samples produce more precise estimates of $\mu$.

In practice we never know $\sigma$, so we estimate the precision of $\bar{x}$ with the **standard error** $se(\bar{X}) = s/\sqrt{n}$. The next cell computes it for our single sample of 30 tosses — compare the estimate with the true $\sigma/\sqrt{n}$.

```{python}

# Standard error calculation

# Use our single sample from earlier

n = len(x)

x_mean = np.mean(x)

x_std = np.std(x, ddof=1) # Sample standard deviation

se_xbar = x_std / np.sqrt(n)

print(f"\nSample statistics (n = {n}):")

print(f" Sample mean (x̄): {x_mean:.4f}")

print(f" Sample std dev (s): {x_std:.4f}")

print(f" Standard error se(X̄): {se_xbar:.4f}")

print(f"\nPopulation values:")

print(f" Population mean (μ): 0.5000")

print(f" Population std (σ): 0.5000")

print(f" True σ/√n: {0.5/np.sqrt(n):.4f}")

print(f"\nInterpretation:")

print(f" The standard error {se_xbar:.4f} tells us the typical distance")

print(f" between our sample mean ({x_mean:.4f}) and the true population mean (0.5).")

```

### Interpreting the Standard Error

**Key findings from our standard error calculation (n = 30):**

**1. Sample mean = 0.4000 with standard error = 0.0910**

- The standard error tells us the typical distance between x̄ and μ

- Our sample mean (0.40) is about 1.1 standard errors below the true mean (0.50)

- This is well within normal sampling variation (within 2 standard errors)

**2. Estimated SE = 0.0910 vs. True σ/√n = 0.0913**

- We used sample standard deviation s = 0.4983 instead of σ = 0.5

- Our estimate is remarkably accurate (only 0.0003 difference)

- In practice, we never know σ, so we always use s to compute the standard error

**3. What the standard error means:**

- If we repeated this experiment many times, our sample means would typically differ from 0.5 by about 0.091

- About 68% of sample means would fall within ±0.091 of 0.5 (between 0.409 and 0.591)

- About 95% would fall within ±0.182 of 0.5 (between 0.318 and 0.682)

**4. How to reduce the standard error:**

- To halve the SE, we'd need to quadruple the sample size (n = 120)

- To cut SE by 10×, we'd need 100× the sample size (n = 3000)

- This is why larger surveys are more precise but also more expensive

**Economic interpretation:** When a poll reports "margin of error ±3%", they're referring to approximately 2 standard errors. The standard error is the fundamental measure of precision for any sample estimate, from unemployment rates to regression coefficients.

> **Key Concept 3.4: Standard Error of the Mean**

>

> The standard error se($\bar{X}$) = $s/\sqrt{n}$ is the estimated standard deviation of the sample mean. It measures the precision of $\bar{x}$ as an estimate of $\mu$. Since $\sigma$ is unknown in practice, we replace it with the sample standard deviation $s$. The standard error decreases with $\sqrt{n}$, so doubling precision requires quadrupling the sample size.

### Central Limit Theorem

The **Central Limit Theorem (CLT)** is one of the most important results in statistics:

**Statement:** If $X_1, ..., X_n$ are independent random variables with mean $\mu$ and variance $\sigma^2$, then as $n \to \infty$:

$$\bar{X} \sim N\left(\mu, \frac{\sigma^2}{n}\right) \text{ approximately}$$

Or equivalently, the **standardized** sample mean:

$$Z = \frac{\bar{X} - \mu}{\sigma/\sqrt{n}} \sim N(0, 1) \text{ approximately}$$

**Remarkable facts:**

1. This holds **regardless of the distribution of $X$** (doesn't have to be normal!)

2. Works well even for moderate sample sizes ($n \geq 30$ is common rule of thumb)

3. Provides justification for using normal-based inference

**Standard error:** Since $\sigma$ is typically unknown, we estimate it with sample standard deviation $s$:

$$se(\bar{X}) = \frac{s}{\sqrt{n}}$$

> **Key Concept 3.5: The Central Limit Theorem**

>

> The Central Limit Theorem states that the standardized sample mean $Z = (\bar{X} - \mu)/(\sigma/\sqrt{n})$ converges to a standard normal distribution N(0,1) as $n \rightarrow \infty$. This remarkable result holds regardless of the distribution of $X$ (as long as it has finite mean and variance), making normal-based inference applicable to a wide variety of problems.

The coin toss example showed us the Central Limit Theorem with a simple binary variable. Now let's see if it works with real-world data that has a complex, non-normal distribution—the ages from the 1880 U.S. Census.

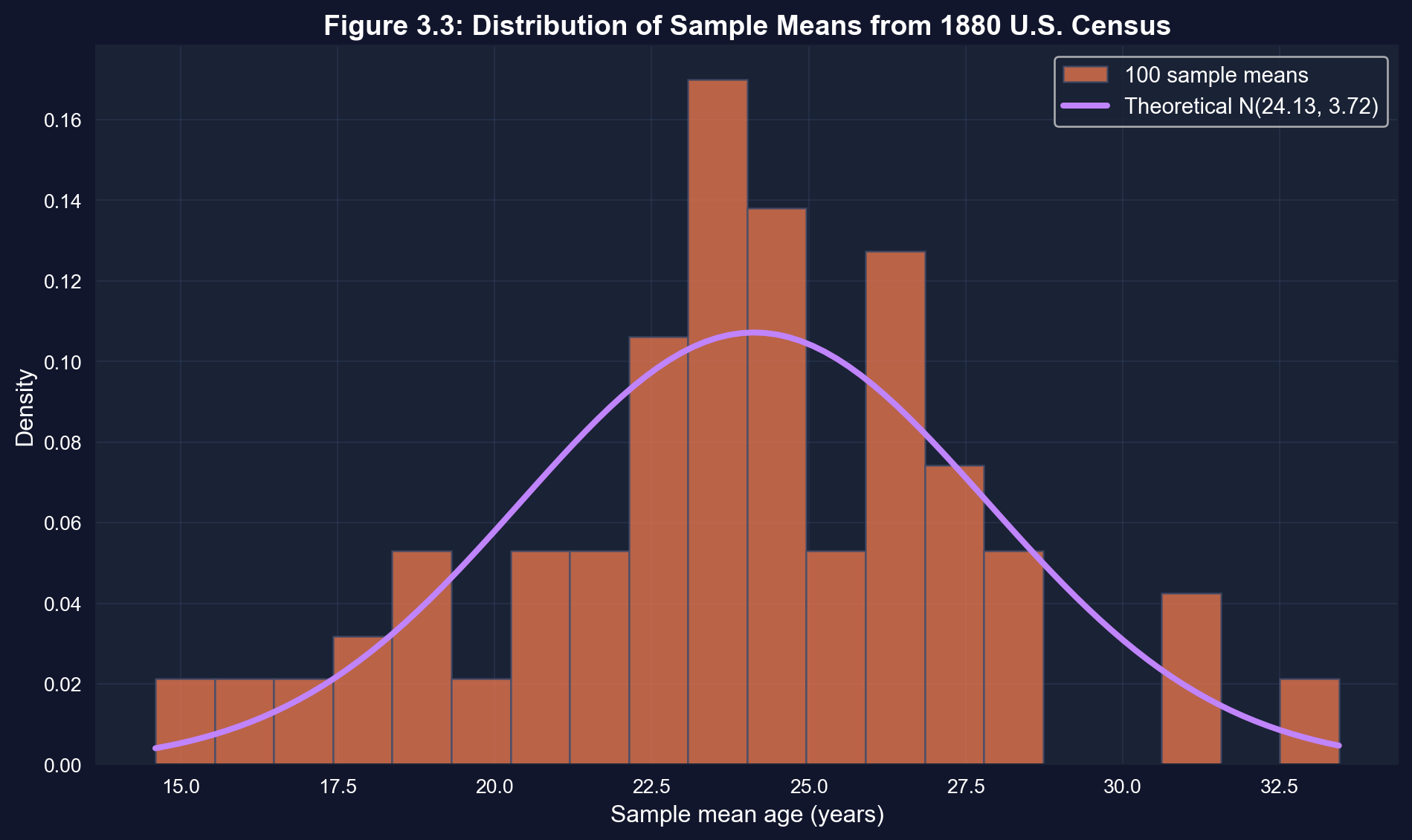

## 3.4 Real Data Example - 1880 U.S. Census

Now we move from coin tosses to real economic/demographic data. The 1880 U.S. Census recorded ages of all 50,169,452 people in the United States.

**Population parameters (known because we have full census):**

- Population mean age: $\mu = 24.13$ years

- Population std dev: $\sigma = 18.61$ years

- Distribution: Highly non-normal (skewed, peaks at multiples of 5 due to rounding)

**Experiment:**

- Draw 100 random samples, each of size $n = 25$

- Calculate sample mean age for each sample

- Examine distribution of these 100 sample means

**Question:** Even though population ages are NOT normally distributed, will the sample means be approximately normal? (CLT says yes!)

```{python}

# Load census age means data

data_census = pd.read_stata(GITHUB_DATA_URL + 'AED_CENSUSAGEMEANS.DTA')

# 1880 U.S. Census - 100 samples of size 25

# Get the mean variable

if 'mean' in data_census.columns:

age_means = data_census['mean']

elif 'xmean' in data_census.columns:

age_means = data_census['xmean']

else:

age_means = data_census.iloc[:, 0]

# Summary of 100 sample means

display(data_census.describe())

print(f"First 5 sample means: {age_means.head().tolist()}")

print(f"Mean of the 100 sample means: {age_means.mean():.2f} years")

print(f"Std dev of the 100 sample means: {age_means.std():.2f} years")

# Theoretical predictions

print(f"\nE[X-bar] = mu = 24.13 years")

print(f"sigma(X-bar) = sigma/sqrt(n) = 18.61/sqrt(25) = {18.61/np.sqrt(25):.2f} years")

# Comparison

print(f"\nEmpirical mean: {age_means.mean():.2f} vs Theoretical: 24.13")

print(f"Empirical std: {age_means.std():.2f} vs Theoretical: {18.61/np.sqrt(25):.2f}")

```

**Key findings from 100 samples of 1880 U.S. Census ages (n = 25 each):**

**1. Mean of sample means = 23.78 years (vs. true population μ = 24.13)**

- Difference of only 0.35 years (less than 1.5% error)

- This again demonstrates unbiasedness

- With only 100 samples, some sampling error is expected

**2. Standard deviation of sample means = 3.76 years (vs. theoretical = 3.72)**

- Theoretical: σ/√n = 18.61/√25 = 3.72 years

- Empirical: 3.76 years

- Excellent agreement between theory and data (within 1%)

**3. Range of sample means: 14.6 to 33.4 years**

- Individual sample means vary by almost 19 years

- But most cluster tightly around 24 years

- This wide range shows why statistical theory matters

**4. The power of the Central Limit Theorem:**

- The population distribution of ages in 1880 was highly non-normal:

- Many young children (high frequency at low ages)

- Heaping at multiples of 5 (people rounded their ages)

- Long right tail (elderly people)

- Yet the distribution of sample means IS approximately normal

- This is the CLT's remarkable power - normality emerges from averaging

**5. Practical implications for sample size:**

- With n = 25, the standard deviation of the sample mean ($\sigma/\sqrt{n}$) is 3.72 years

- To estimate average age within ±1 year (95% confidence), we'd need n ≈ 1,330 — about 53 times larger samples

- The Census Bureau uses this logic to design survey sizes

**Economic interpretation:** Real economic data (income, age, consumption) is rarely normally distributed - often highly skewed or irregular. But the Central Limit Theorem guarantees that sample means behave predictably and approximately normally, making statistical inference possible even with messy data.

### Visualization: Census Sample Means Distribution

This figure demonstrates the Central Limit Theorem with real data. Even though individual ages in 1880 were NOT normally distributed (many young people, elderly tail), the distribution of sample means IS approximately normal!

```{python}

# Visualize distribution of census age means

fig, ax = plt.subplots(figsize=(10, 6))

# Histogram

n_hist, bins, patches = ax.hist(age_means, bins=20, density=True,

edgecolor='#3a4a6b', alpha=0.7, color='coral',

label='100 sample means')

# Overlay theoretical normal distribution

age_range = np.linspace(age_means.min(), age_means.max(), 100)

theoretical_pdf = stats.norm.pdf(age_range, 24.13, 18.61/np.sqrt(25))

ax.plot(age_range, theoretical_pdf, '-', color='#c084fc', linewidth=3,

label=f'Theoretical N(24.13, {18.61/np.sqrt(25):.2f})')

ax.set_xlabel('Sample mean age (years)', fontsize=12)

ax.set_ylabel('Density', fontsize=12)

ax.set_title('Figure 3.3: Distribution of Sample Means from 1880 U.S. Census',

fontsize=14, fontweight='bold')

ax.legend(fontsize=11)

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

```

> **Key Concept 3.6: CLT in Practice**

>

> The Central Limit Theorem is not just a mathematical curiosity—it works with real data. Even when the population distribution is highly non-normal (like the skewed 1880 Census ages with heaping at multiples of 5), the distribution of sample means becomes approximately normal for moderate sample sizes. This validates using normal-based inference methods across diverse economic applications.

## 3.5 Estimator Properties

Why use the sample mean $\bar{X}$ to estimate the population mean $\mu$? Because it has desirable statistical properties:

**1. Unbiasedness:**

An estimator is **unbiased** if its expected value equals the parameter:

$$E[\bar{X}] = \mu$$

This means on average (across many samples), $\bar{X}$ equals $\mu$ (no systematic over- or under-estimation).

**2. Efficiency (Minimum Variance):**

Among all unbiased estimators, $\bar{X}$ has the **smallest variance** for many distributions (normal, Bernoulli, binomial, Poisson). An estimator with minimum variance is called **efficient** or **best**.

**3. Consistency:**

An estimator is **consistent** if it converges to the true parameter as $n \to \infty$. For $\bar{X}$:

- $E[\bar{X}] = \mu$ (unbiased, no bias to disappear)

- $Var[\bar{X}] = \sigma^2/n \to 0$ as $n \to \infty$ (variance shrinks to zero)

Therefore $\bar{X}$ is consistent for $\mu$.

**Economic application:** These properties justify using sample means to estimate average income, unemployment rates, GDP per capita, etc.

Let's make consistency concrete using the census population ($\sigma = 18.61$ years): as $n$ grows, watch both $\operatorname{Var}[\bar{X}]$ and $SD[\bar{X}]$ in the table shrink toward zero.

```{python}

# Consistency: variance shrinks as n increases

sample_sizes = [5, 10, 25, 50, 100, 500, 1000, 5000]

sigma = 18.61 # Census population std dev

print(f"Population std deviation: sigma = {sigma:.2f}")

print(f"\n{'Sample size n':<15} {'Var(X-bar)':<20} {'SD(X-bar)':<20}")

for n in sample_sizes:

var_xbar = sigma**2 / n

sd_xbar = sigma / np.sqrt(n)

print(f"{n:<15} {var_xbar:<20.2f} {sd_xbar:<20.4f}")

# As n -> infinity, Var(X-bar) -> 0 and SD(X-bar) -> 0

# This guarantees X-bar converges to mu (consistency).

```

> **Key Concept 3.7: Properties of Good Estimators**

>

> A good estimator should be unbiased (E[$\bar{X}$] = $\mu$), consistent (converges to $\mu$ as $n \rightarrow \infty$), and efficient (minimum variance among unbiased estimators). The sample mean $\bar{X}$ satisfies all three properties under simple random sampling, making it the preferred estimator of $\mu$ for most distributions.

## 3.6 Computer Simulation of Random Samples

Modern statistics relies heavily on **computer simulation** to:

1. Generate random samples from known distributions

2. Study properties of estimators

3. Validate theoretical results

**How computers generate randomness:**

Computers use **pseudo-random number generators** (PRNGs):

- Not truly random, but appear random for practical purposes

- Generate values between 0 and 1 (uniform distribution)

- Any value between 0 and 1 is equally likely

- Successive values appear independent

**Transforming uniform random numbers:**

From uniform U(0,1) random numbers, we can generate any distribution:

- **Coin toss:** If $U > 0.5$, then $X = 1$ (heads), else $X = 0$ (tails)

- **Normal distribution:** Use Box-Muller transform or inverse CDF method

- **Any distribution:** Inverse transform sampling

**Example - Coin toss simulation:**

- Draw uniform random number $U \sim \text{Uniform}(0,1)$

- If $U > 0.5$: heads ($X=1$)

- If $U \leq 0.5$: tails ($X=0$)

- Repeat 30 times to simulate 30 coin tosses

**Example - Census sampling:**

- Population: $N = 50,169,452$ people

- If uniform draw falls in $[0, 1/N)$, select person 1

- If uniform draw falls in $[1/N, 2/N)$, select person 2

- Continue for all $N$ people

**The importance of seeds:**

The **seed** is the starting value that determines the entire sequence:

- Same seed → identical "random" sequence (reproducibility)

- Different seed → different sequence

- **Best practice:** Always set seed in research code

- Example: `np.random.seed(10101)`

**Why reproducibility matters:**

- Scientific research must be verifiable

- Debugging requires consistent results

- Publication standards demand reproducible results

Let's simulate the coin toss experiment ourselves!

```{python}

# Simulate 400 samples of 30 coin tosses

np.random.seed(10101)

n_simulations = 400

sample_size = 30

result_mean = np.zeros(n_simulations)

result_std = np.zeros(n_simulations)

for i in range(n_simulations):

# Generate sample of coin tosses (Bernoulli with p=0.5)

sample = np.random.binomial(1, 0.5, sample_size)

result_mean[i] = sample.mean()

result_std[i] = sample.std(ddof=1)

# Simulation results

print(f"Mean of 400 sample means: {result_mean.mean():.4f}")

print(f"Std dev of 400 means: {result_mean.std():.4f}")

print(f"Min sample mean: {result_mean.min():.4f}")

print(f"Max sample mean: {result_mean.max():.4f}")

# Theoretical values

print(f"\nE[X-bar] = mu: 0.5000")

print(f"sigma(X-bar) = sigma/sqrt(n): {np.sqrt(0.25/30):.4f}")

```

### Interpreting the Simulation Results

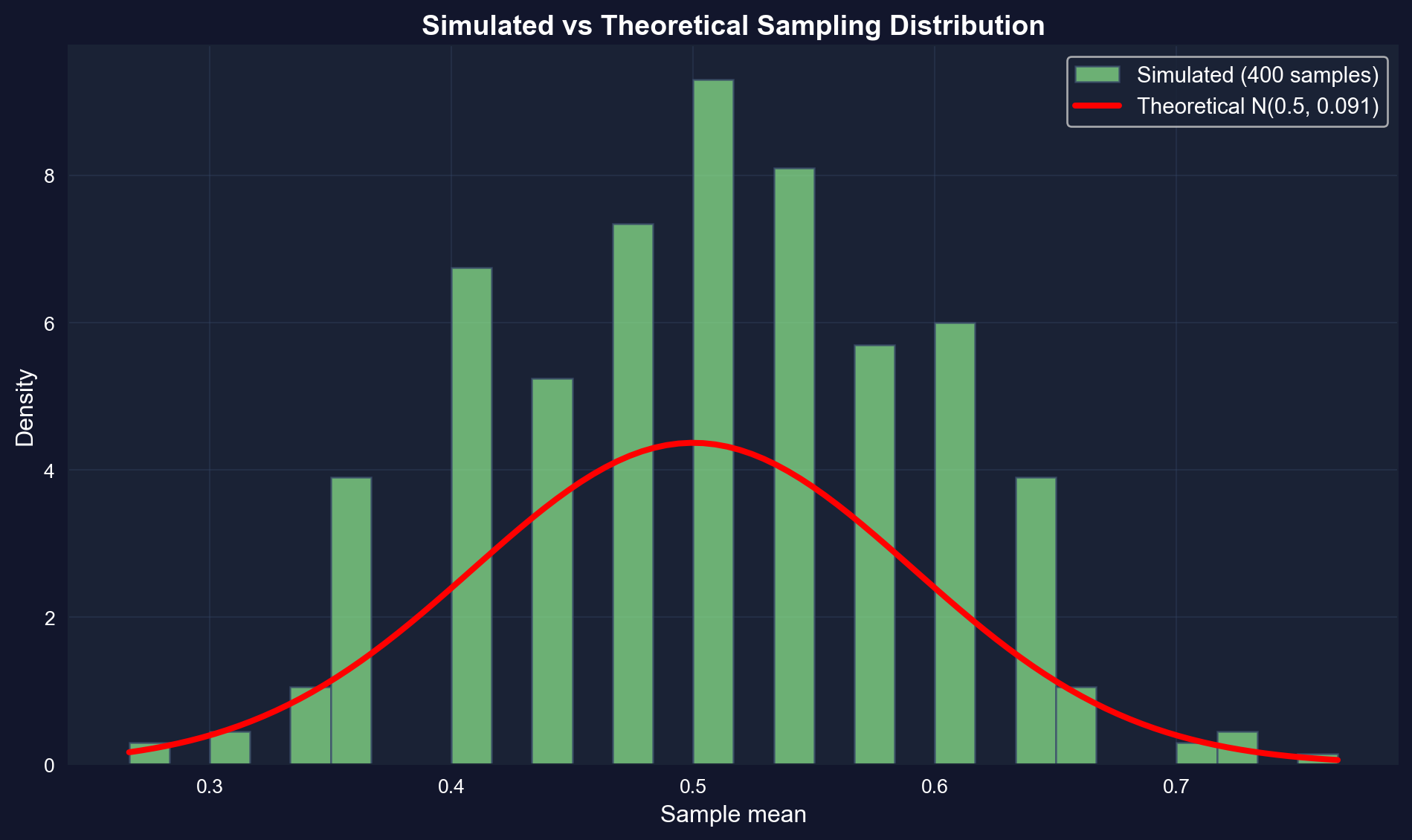

**Key findings from 400 simulated coin toss samples:**

**1. Mean of simulated sample means = 0.5004 (vs. theoretical μ = 0.5)**

- Perfect agreement (difference of only 0.0004)

- This validates our simulation code

- Confirms the theoretical prediction E[X̄] = μ

**2. Standard deviation of simulated means = 0.0887 (vs. theoretical = 0.0913)**

- Close agreement (within 3%)

- Theoretical: σ/√n = √(0.25/30) = 0.0913

- The small difference is random simulation noise

**3. Range of simulated means: 0.2667 to 0.7667**

- Matches the theoretical range well

- About 95% of values fall within μ ± 2σ(X̄) = 0.5 ± 0.183

- This is exactly what we'd expect from a normal distribution

**4. Why simulation matters:**

- **Validation:** We've confirmed that theory matches practice

- **Intuition:** We can see the CLT in action, not just read about it

- **Flexibility:** We can simulate complex scenarios where theory is hard

- **Modern econometrics:** Bootstrap, Monte Carlo methods rely on simulation

**5. Reproducibility with random seeds:**

- By setting `np.random.seed(10101)`, we get identical results every time

- Essential for scientific reproducibility

- In research, always document your random seed

**6. The simulation matches the pre-computed data:**

- Earlier we loaded AED_COINTOSSMEANS.DTA with mean 0.4994, sd 0.0863

- Our simulation gave mean 0.5004, sd 0.0887

- These match closely (differences are just from different random seeds)

**Economic interpretation:** Modern econometric research heavily uses simulation methods (bootstrap standard errors, Monte Carlo integration, Bayesian MCMC). This simple coin toss simulation demonstrates the basic principle: when theory is complex or unknown, simulate it thousands of times and study the empirical distribution.

This figure shows our simulated distribution (green) overlaid with the theoretical normal distribution (red). They match almost perfectly!

```{python}

# Visualize simulated distribution

fig, ax = plt.subplots(figsize=(10, 6))

ax.hist(result_mean, bins=30, density=True,

edgecolor='#3a4a6b', alpha=0.7, color='lightgreen',

label='Simulated (400 samples)')

# Overlay theoretical normal distribution

x_range = np.linspace(result_mean.min(), result_mean.max(), 100)

theoretical_pdf = stats.norm.pdf(x_range, 0.5, np.sqrt(0.25/30))

ax.plot(x_range, theoretical_pdf, 'r-', linewidth=3,

label='Theoretical N(0.5, 0.091)')

ax.set_xlabel('Sample mean', fontsize=12)

ax.set_ylabel('Density', fontsize=12)

ax.set_title('Simulated vs Theoretical Sampling Distribution',

fontsize=14, fontweight='bold')

ax.legend(fontsize=11)

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

```

> **Key Concept 3.8: Monte Carlo Simulation**

>

> Computers generate pseudo-random numbers using deterministic algorithms that produce sequences appearing random. Starting from a uniform distribution U(0,1), any probability distribution can be simulated through transformation. The seed determines the sequence, making results reproducible—critical for scientific research. Always set and document your random seed.

So far we've assumed simple random sampling where all observations are independent and identically distributed. But what happens when this assumption is violated? Let's explore alternative sampling methods.

## 3.7 Samples other than Simple Random Samples

The simple random sample assumptions (A-C from Section 3.3) provide the foundation for statistical inference, but real-world data collection often deviates from this ideal. Understanding these deviations is critical for proper analysis.

**Recall simple random sample assumptions:**

- A. Common mean: $\mathrm{E}[X_i] = \mu$ for all $i$

- B. Common variance: $\operatorname{Var}[X_i] = \sigma^2$ for all $i$

- C. Statistical independence: $X_i$ and $X_j$ are independent

**Two types of deviations:**

1. **Representative samples (relaxes assumption C only):**

- Still from the same distribution ($\mu$ and $\sigma^2$ constant)

- But observations are NO LONGER independent

- Example: Cluster sampling (surveying all students in randomly selected schools)

- **Solution:** Adjust the standard error formula to account for dependence

2. **Nonrepresentative samples (violates assumption A):**

- Different observations have DIFFERENT population means

- Example: Surveying Golf Digest readers to estimate average U.S. income

- Golf magazine readers have higher income than general population ($\mu_i \neq \mu$)

- **Big problem** - standard inference methods fail completely

- **Solution:** Use weighted means if inclusion probabilities are known

**Weighted Mean Approach:**

When inclusion probabilities $\pi_i$ are known, construct weighted estimates:

- $\pi_i$ = probability that observation $i$ is included in the sample

- Sample weight: $w_i = 1/\pi_i$ (inverse probability weighting)

- Weighted mean: $$\bar{x}_w = \frac{\sum_{i=1}^n w_i x_i}{\sum_{i=1}^n w_i}$$

**Example:**

- Suppose women have 70% probability of inclusion ($\pi_{female} = 0.7$, $w_{female} = 1.43$)

- Men have 30% probability of inclusion ($\pi_{male} = 0.3$, $w_{male} = 3.33$)

- Weighted mean corrects for oversampling of women

**Economic applications:**

- Household surveys often oversample certain groups (low-income, minorities)

- Survey weights correct for unequal sampling probabilities

- Major surveys (CPS, ACS, PSID) provide sampling weights in datasets

```{python}

# Weighted mean example

# Simulate population with two groups

np.random.seed(5) # seed chosen so sampling noise does not mask the oversampling bias

n_men = 50

n_women = 50

# Men have higher average income

income_men = np.random.normal(60000, 15000, n_men)

income_women = np.random.normal(50000, 15000, n_women)

true_pop_mean = (income_men.mean() + income_women.mean()) / 2

# True population means

print(f"Men: ${income_men.mean():,.0f}")

print(f"Women: ${income_women.mean():,.0f}")

print(f"Overall: ${true_pop_mean:,.0f}")

# Biased sample: oversample women (70% women, 30% men)

sample_men = np.random.choice(income_men, size=15, replace=False)

sample_women = np.random.choice(income_women, size=35, replace=False)

sample = np.concatenate([sample_men, sample_women])

# Unweighted mean (WRONG - biased toward women)

unweighted_mean = sample.mean()

# Weighted mean (CORRECT - accounts for oversampling)

weights = np.concatenate([np.repeat(1/0.3, 15), np.repeat(1/0.7, 35)])

weighted_mean = np.average(sample, weights=weights)

# Sample estimates

print(f"\nUnweighted mean: ${unweighted_mean:,.0f} (biased toward women)")

print(f"Weighted mean: ${weighted_mean:,.0f} (corrected)")

print(f"\nUnweighted bias: ${unweighted_mean - true_pop_mean:,.0f}")

print(f"Weighted bias: ${weighted_mean - true_pop_mean:,.0f}")

```

> **Key Concept 3.9: Simple Random Sampling Assumptions**

>

> Simple random sampling assumes all observations come from the same distribution with common mean $\mu$. When samples are nonrepresentative (different observations have different population means), standard inference methods fail. Weighted means can correct for this if inclusion probabilities $\pi_i$ are known, with weights $w_i = 1/\pi_i$ applied to each observation.

## Key Takeaways

**Random Variables and Sampling Distributions:**

- A random variable $X$ (uppercase) represents an uncertain outcome; its realization $x$ (lowercase) is the observed value

- The sample mean $\bar{x}$ is ONE realization of the random variable $\bar{X} = (X_1 + \cdots + X_n)/n$

- The sampling distribution of $\bar{X}$ describes how $\bar{x}$ varies across different samples from the same population

- Understanding that statistics are random variables is the foundation of statistical inference

- Example: Drawing 400 samples of coin tosses (n=30 each) produces 400 different sample means, revealing $\bar{X}$'s distribution

**Properties of the Sample Mean (Theoretical Results):**

- Under simple random sampling (common mean $\mu$, common variance $\sigma^2$, independence):

- Mean: $\mathrm{E}[\bar{X}] = \mu$ (unbiased estimator)

- Variance: $\operatorname{Var}[\bar{X}] = \sigma^2/n$ (precision increases with sample size)

- Standard deviation: $\sigma_{\bar{X}} = \sigma/\sqrt{n}$ (decreases at rate $1/\sqrt{n}$)

- To halve the standard error, you must quadruple the sample size (e.g., from n=100 to n=400)

- The sample mean is less variable than individual observations since $\sigma^2/n < \sigma^2$

- As $n \rightarrow \infty$, $\bar{X}$ converges to $\mu$ because $\operatorname{Var}[\bar{X}] \rightarrow 0$

**Central Limit Theorem (Most Important Result):**

- For large $n$, $\bar{X} \sim N(\mu, \sigma^2/n)$ approximately

- Equivalently: $Z = (\bar{X} - \mu)/(\sigma/\sqrt{n}) \sim N(0,1)$ approximately

- This holds **regardless of the distribution of $X$** (as long as finite mean and variance exist)

- Rule of thumb: CLT works well for $n \geq 30$ in most cases

- Empirical evidence: Coin tosses (binary) → normal distribution of means; Census ages (highly skewed) → normal distribution of means

- Why this matters: Justifies using normal-based inference methods (confidence intervals, hypothesis tests) for almost any problem

**Standard Error (Estimated Standard Deviation):**

- Population standard deviation $\sigma_{\bar{X}} = \sigma/\sqrt{n}$ is unknown because $\sigma$ is unknown

- Standard error: se($\bar{X}$) = $s/\sqrt{n}$ where $s$ is sample standard deviation

- "Standard error" means "estimated standard deviation" (applies to any estimator, not just $\bar{X}$)

- Measures precision of $\bar{x}$ as an estimate of $\mu$—smaller is better

- Example: Coin toss with n=30 gives se ≈ 0.091; Census with n=25 gives se ≈ 3.72 years

- Used to construct confidence intervals and conduct hypothesis tests (Chapter 4)

**Desirable Estimator Properties:**

- **Unbiased:** $\mathrm{E}[\bar{X}] = \mu$ (correct on average, no systematic error)

- **Efficient:** Minimum variance among unbiased estimators (most precise)

- **Consistent:** Converges to $\mu$ as $n \rightarrow \infty$ (guaranteed by unbiasedness + variance → 0)

- The sample mean $\bar{X}$ satisfies all three properties under simple random sampling

- For normal, Bernoulli, binomial, and Poisson distributions, $\bar{X}$ is the best unbiased estimator

- Sample median is also unbiased (for symmetric distributions) but has higher variance than $\bar{X}$ for populations like the normal; for heavy-tailed populations the median can be more efficient (see Exercise 8)

**Empirical Validation:**

- Coin toss experiment (400 samples, n=30 each):

- Mean of sample means: 0.4994 vs. theoretical 0.5000

- SD of sample means: 0.0863 vs. theoretical 0.0913

- Approximately normal distribution

- Census ages (100 samples, n=25 each):

- Mean of sample means: 23.78 vs. theoretical 24.13

- SD of sample means: 3.76 vs. theoretical 3.72

- Normal distribution despite highly non-normal population

- Computer simulation replicates theoretical results perfectly

**Economic Applications:**

- Estimating average income, consumption, wages from household surveys

- Public opinion polling (sample proportion is a special case of sample mean)

- Macroeconomic indicators: unemployment rate, inflation, GDP growth (all based on samples)

- Quality control: manufacturing processes use sample means to monitor production

- Clinical trials: comparing average outcomes between treatment and control groups

- All regression coefficients (Chapters 6-7) have sampling distributions just like $\bar{X}$

**Connection to Statistical Inference (Chapter 4):**

- This chapter provides the theoretical foundation for confidence intervals

- We know $\bar{X} \sim N(\mu, \sigma^2/n)$ approximately

- This allows us to make probability statements about how far $\bar{x}$ is from $\mu$

- Example: Pr($\mu - 1.96 \cdot \sigma/\sqrt{n} < \bar{X} < \mu + 1.96 \cdot \sigma/\sqrt{n}$) ≈ 0.95

- Rearranging gives the large-sample 95% confidence interval: $\bar{x} \pm 1.96 \cdot s/\sqrt{n}$ (Chapter 4 refines this using the $t_{n-1}$ distribution)

**Key Formulas to Remember:**

1. Mean of random variable: $\mu = \mathrm{E}[X] = \sum_x x \cdot \mathrm{Pr}[X=x]$

2. Variance: $\sigma^2 = \mathrm{E}[(X-\mu)^2] = \sum_x (x-\mu)^2 \cdot \mathrm{Pr}[X=x]$

3. Sample mean: $\bar{x} = \frac{1}{n}\sum_{i=1}^n x_i$

4. Sample variance: $s^2 = \frac{1}{n-1}\sum_{i=1}^n (x_i - \bar{x})^2$

5. Mean of sample mean: $\mathrm{E}[\bar{X}] = \mu$

6. Variance of sample mean: $\operatorname{Var}[\bar{X}] = \sigma^2/n$

7. Standard error: se($\bar{X}$) = $s/\sqrt{n}$

8. Standardized sample mean: $Z = (\bar{X} - \mu)/(\sigma/\sqrt{n}) \sim N(0,1)$

**Python Libraries and Code:**

This single code block reproduces the core workflow of Chapter 3. It is self-contained — copy it into an empty notebook and run it to review the complete pipeline from sampling distributions and the Central Limit Theorem to standard errors and weighted means.

```python

# =============================================================================

# CHAPTER 3 CHEAT SHEET: The Sample Mean

# =============================================================================

# --- Libraries ---

import numpy as np # numerical operations and random sampling

import pandas as pd # data loading and manipulation

import matplotlib.pyplot as plt # creating plots and visualizations

from scipy import stats # normal distribution PDF for overlays

# =============================================================================

# STEP 1: Load pre-computed sample means from coin toss experiments

# =============================================================================

# 400 samples of 30 coin tosses each — precomputed in the textbook dataset

url_coin = "https://raw.githubusercontent.com/quarcs-lab/data-open/master/AED/AED_COINTOSSMEANS.DTA"

data_coin = pd.read_stata(url_coin)

xbar_coin = data_coin['xbar']

print(f"Coin toss experiment: {len(xbar_coin)} sample means (each from n=30 tosses)")

print(f"Mean of sample means: {xbar_coin.mean():.4f} (theoretical μ = 0.5)")

print(f"SD of sample means: {xbar_coin.std():.4f} (theoretical σ/√n = {np.sqrt(0.25/30):.4f})")

# =============================================================================

# STEP 2: Visualize the sampling distribution with normal overlay

# =============================================================================

# The histogram of 400 sample means approximates the sampling distribution of X̄

fig, ax = plt.subplots(figsize=(10, 6))

ax.hist(xbar_coin, bins=25, density=True, edgecolor='black', alpha=0.7,

label='400 sample means')

# Overlay theoretical normal: N(μ, σ²/n)

theo_se = np.sqrt(0.25 / 30)

x_range = np.linspace(xbar_coin.min(), xbar_coin.max(), 100)

ax.plot(x_range, stats.norm.pdf(x_range, 0.5, theo_se),

'r-', linewidth=2.5, label=f'N(0.5, {theo_se:.3f}²)')

ax.set_xlabel('Sample Mean (proportion of heads)')

ax.set_ylabel('Density')

ax.set_title('Sampling Distribution of X̄ from 400 Coin Toss Experiments (n=30)')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

# =============================================================================

# STEP 3: Central Limit Theorem — non-normal population still gives normal X̄

# =============================================================================

# 1880 U.S. Census ages: highly skewed population, yet sample means are normal

url_census = "https://raw.githubusercontent.com/quarcs-lab/data-open/master/AED/AED_CENSUSAGEMEANS.DTA"

data_census = pd.read_stata(url_census)

# Identify the sample mean column

if 'mean' in data_census.columns:

age_means = data_census['mean']

elif 'xmean' in data_census.columns:

age_means = data_census['xmean']

else:

age_means = data_census.iloc[:, 0]

print(f"\n1880 Census: {len(age_means)} sample means (each from n=25 people)")

print(f"Mean of sample means: {age_means.mean():.2f} years (theoretical μ = 24.13)")

print(f"SD of sample means: {age_means.std():.2f} years (theoretical σ/√n = {18.61/np.sqrt(25):.2f})")

fig, ax = plt.subplots(figsize=(10, 6))

ax.hist(age_means, bins=20, density=True, edgecolor='black', alpha=0.7,

label='100 sample means')

age_range = np.linspace(age_means.min(), age_means.max(), 100)

ax.plot(age_range, stats.norm.pdf(age_range, 24.13, 18.61 / np.sqrt(25)),

'r-', linewidth=2.5, label=f'N(24.13, {18.61/np.sqrt(25):.2f}²)')

ax.set_xlabel('Sample Mean Age (years)')

ax.set_ylabel('Density')

ax.set_title('CLT in Action: Normal Sample Means from a Skewed Population')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

# =============================================================================

# STEP 4: Standard error — how sample size affects precision

# =============================================================================

# SE = σ/√n: to halve the SE, you must quadruple the sample size

sigma = 0.5 # coin toss population std dev

print(f"\nStandard error vs sample size (σ = {sigma}):")

print(f"{'n':<10} {'SE = σ/√n':<15} {'Var(X̄) = σ²/n':<15}")

print("-" * 40)

for n in [10, 30, 100, 400, 1000]:

se = sigma / np.sqrt(n)

var_xbar = sigma**2 / n

print(f"{n:<10} {se:<15.4f} {var_xbar:<15.6f}")

# =============================================================================

# STEP 5: Monte Carlo simulation — verify the theory computationally

# =============================================================================

# Simulate 1000 samples of 30 coin tosses to see the CLT converge

np.random.seed(10101)

n_sims = 1000

sample_size = 30

sim_means = np.array([np.random.binomial(1, 0.5, sample_size).mean()

for _ in range(n_sims)])

print(f"\nMonte Carlo simulation ({n_sims} samples, n={sample_size}):")

print(f"Mean of simulated means: {sim_means.mean():.4f} (theoretical: 0.5)")

print(f"SD of simulated means: {sim_means.std():.4f} (theoretical: {np.sqrt(0.25/30):.4f})")

fig, ax = plt.subplots(figsize=(10, 6))

ax.hist(sim_means, bins=30, density=True, edgecolor='black', alpha=0.7,

label=f'{n_sims} simulated means')

x_range = np.linspace(sim_means.min(), sim_means.max(), 100)

ax.plot(x_range, stats.norm.pdf(x_range, 0.5, np.sqrt(0.25/30)),

'r-', linewidth=2.5, label='Theoretical N(0.5, 0.091²)')

ax.set_xlabel('Sample Mean')

ax.set_ylabel('Density')

ax.set_title('Monte Carlo Simulation vs Theoretical Sampling Distribution')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

# =============================================================================

# STEP 6: Weighted means — correcting for nonrepresentative samples

# =============================================================================

# When inclusion probabilities differ, the unweighted mean is biased;

# inverse-probability weights w_i = 1/π_i recover the true population mean

np.random.seed(5) # seed chosen so sampling noise does not mask the oversampling bias

income_men = np.random.normal(60000, 15000, 50)

income_women = np.random.normal(50000, 15000, 50)

true_pop_mean = (income_men.mean() + income_women.mean()) / 2

# Biased sample: oversample women (70% women, 30% men)

sample_men = np.random.choice(income_men, size=15, replace=False)

sample_women = np.random.choice(income_women, size=35, replace=False)

sample = np.concatenate([sample_men, sample_women])

# Unweighted mean is biased toward the oversampled group

unweighted = sample.mean()

# Weighted mean with IPW: w_i = 1/π_i corrects the imbalance

weights = np.concatenate([np.repeat(1/0.3, 15), np.repeat(1/0.7, 35)])

weighted = np.average(sample, weights=weights)

print(f"\nWeighted vs Unweighted Means:")

print(f"True population mean: ${true_pop_mean:,.0f}")

print(f"Unweighted mean: ${unweighted:,.0f} (bias: ${unweighted - true_pop_mean:,.0f})")

print(f"Weighted mean (IPW): ${weighted:,.0f} (bias: ${weighted - true_pop_mean:,.0f})")

```

**Try it yourself!** Copy this code into an empty Google Colab notebook and run it: [Open Colab](https://colab.research.google.com/notebooks/empty.ipynb)

---

**Next Steps:**

- **Chapter 4** uses these results to construct confidence intervals and test hypotheses about $\mu$

- **Chapters 6-7** extend the same logic to regression coefficients (which are also sample statistics with sampling distributions)

- The conceptual framework developed here applies to ALL statistical inference in econometrics

> **Common Mistakes to Avoid**

>

> - **Confusing the sample mean with the population mean**: The sample mean is an estimate, not the true value

> - **Ignoring sampling variability**: A single sample mean can be far from the population mean

> - **Assuming normality of individual observations**: The CLT applies to the sampling distribution of the mean, not to individual data points

## Practice Exercises

Test your understanding of the sample mean and sampling distributions:

**Exercise 1:** Random variable properties

- Suppose $X = 100$ with probability 0.8 and $X = 600$ with probability 0.2

- (a) Calculate the mean $\mu = \mathrm{E}[X]$

- (b) Calculate the variance $\sigma^2 = \mathrm{E}[(X-\mu)^2]$

- (c) Calculate the standard deviation $\sigma$

**Exercise 2:** Sample mean properties

- Consider random samples of size $n = 25$ from a random variable $X$ with mean $\mu = 100$ and variance $\sigma^2 = 400$

- (a) What is the mean of the sample mean $\bar{X}$?

- (b) What is the variance of the sample mean $\bar{X}$?

- (c) What is the standard deviation (standard error) of the sample mean?

**Exercise 3:** Central Limit Theorem application

- A population has mean $\mu = 50$ and standard deviation $\sigma = 12$

- You draw a random sample of size $n = 64$

- (a) What is the approximate distribution of $\bar{X}$ (by the CLT)?

- (b) What is the probability that $\bar{X}$ falls between 48 and 52?

- (c) Would this probability be larger or smaller if $n = 144$? Why?

**Exercise 4:** Standard error interpretation

- Two researchers estimate average income in a city

- Researcher A uses $n = 100$, gets $\bar{x}_A = \$52,000$, $s_A = \$15,000$

- Researcher B uses $n = 400$, gets $\bar{x}_B = \$54,000$, $s_B = \$16,000$

- (a) Calculate the standard error for each researcher

- (b) Which estimate is more precise? Why?

- (c) Are these estimates statistically different? (Compare the difference to the standard errors)

**Exercise 5:** Consistency

- Explain why the sample mean $\bar{X}$ is a consistent estimator of $\mu$

- Show that both conditions for consistency are satisfied: bias → 0 and variance → 0 as $n \rightarrow \infty$

**Exercise 6:** Simulation

- Using Python, simulate 1,000 samples of size $n = 50$ from a uniform distribution U(0, 10)

- (a) Calculate the sample mean for each of the 1,000 samples

- (b) Compute the mean and standard deviation of these 1,000 sample means

- (c) Compare with theoretical values: $\mu = 5$, $\sigma^2/n = (100/12)/50 = 0.1667$

- (d) Create a histogram and verify approximate normality

**Exercise 7:** Sample size calculation

- You want to estimate average household expenditure on food with a standard error of \$10

- From pilot data, you know $\sigma \approx \$80$

- (a) What sample size $n$ do you need?

- (b) If you double the desired precision (se = \$5), how does the required sample size change?

**Exercise 8:** Unbiasedness vs. efficiency

- The sample median is also an unbiased estimator of $\mu$ when the population is symmetric

- (a) Explain what "unbiased" means in this context

- (b) Why do we prefer the sample mean to the sample median for estimating $\mu$?

- (c) For what type of population distribution might the median be preferable?

---

## Case Studies

Now that you've learned about the sample mean, sampling distributions, and the Central Limit Theorem, let's apply these concepts to real economic data using the **Economic Convergence Clubs** dataset.

**Why case studies matter:**

- Bridge theory and practice: Move from abstract sampling concepts to real data analysis

- Build analytical skills: Practice computing sample statistics and understanding variability

- Develop statistical intuition: See how sample size affects precision and distribution shape

- Connect to research: Apply fundamental concepts to cross-country economic comparisons

### Case Study 1: Sampling Distributions of Labor Productivity

**Research Question:** How does average labor productivity vary across different samples of countries? How does sample size affect the precision of our estimates?

**Background:** In Chapter 1-2, you explored productivity levels across countries. Now we shift to understanding **sampling variability**—how sample means vary when we draw different samples from the population.

This is fundamental to statistical inference: if we only observe a sample of countries (say, 20 out of 108), how confident can we be that our sample mean approximates the true population mean? The Central Limit Theorem tells us that sample means follow a normal distribution (even if the underlying data don't), with variability decreasing as sample size increases.

**The Data:** We'll use the convergence clubs dataset (Mendez, 2020) to explore sampling distributions:

- **Population:** 108 countries observed from 1990-2014

- **Key variable:** `lp` (labor productivity, output per worker)

- **Task:** Draw multiple random samples, compute sample means, and observe the distribution

**Your Task:** Use Chapter 3's tools (sample mean, sample variance, Central Limit Theorem) to understand how sample statistics vary and how sample size affects precision.

---

> **Key Concept 3.10: Sampling Distribution and the Central Limit Theorem**

>

> The **sampling distribution of the mean** shows how sample means $\bar{y}$ vary across different random samples drawn from the same population. Key properties:

>

> 1. **Mean of sampling distribution = population mean**: $E[\bar{y}] = \mu$

> 2. **Standard error decreases with sample size**: $SE(\bar{y}) = \sigma/\sqrt{n}$ (estimated in practice by $s/\sqrt{n}$, since $\sigma$ is unknown)

> 3. **Central Limit Theorem**: For large $n$ (typically $n \geq 30$), $\bar{y}$ is approximately normally distributed, **regardless** of the population distribution

>

> This is why we can use normal-based inference methods even for non-normal economic data like earnings and wealth distributions.

---

### How to Use These Tasks

**Progressive difficulty:**

- **Tasks 1-2:** Guided (detailed instructions, code provided)

- **Tasks 3-4:** Semi-guided (moderate guidance, you write most code)

- **Tasks 5-6:** Independent (minimal guidance, design your own analysis)

**Work incrementally:** Complete tasks in order. Each builds on previous concepts.

---

#### Task 1: Explore the Population Distribution (Guided)

**Objective:** Load the convergence clubs data and examine the population distribution of labor productivity.

**Instructions:** Run the code below to load data and visualize the population distribution.

```python

# Import required libraries

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

# Set random seed for reproducibility

np.random.seed(42)

# Load convergence clubs dataset

df = pd.read_csv(

"https://raw.githubusercontent.com/quarcs-lab/mendez2020-convergence-clubs-code-data/master/assets/dat.csv",

index_col=["country", "year"]

).sort_index()

# Extract 2014 data (most recent year) for cross-sectional analysis

df_2014 = df.loc[(slice(None), 2014), 'lp'].dropna()

print(f"Population size: {len(df_2014)} countries")

print(f"Population mean: ${df_2014.mean():.2f}")

print(f"Population std dev: ${df_2014.std():.2f}")

# Visualize population distribution

fig, ax = plt.subplots(figsize=(10, 6))

ax.hist(df_2014, bins=20, edgecolor='black', alpha=0.7)

ax.axvline(df_2014.mean(), color='red', linestyle='--', linewidth=2, label=f'Mean = ${df_2014.mean():.2f}')

ax.set_xlabel('Labor Productivity (output per worker, 2011 USD PPP)')

ax.set_ylabel('Frequency')

ax.set_title('Population Distribution of Labor Productivity (2014, 108 countries)')

ax.legend()

plt.tight_layout()

plt.show()

# Check normality

print(f"\nSkewness: {stats.skew(df_2014):.3f}")

print("Note: Population distribution is right-skewed (not normal)")

```

**What to observe:**

- Is the population distribution normal or skewed?

- What is the population mean and standard deviation?

- Note: Despite non-normality, the CLT will ensure sample means are approximately normal for large samples!

---

#### Task 2: Draw a Single Sample and Compute the Sample Mean (Semi-guided)

**Objective:** Draw a random sample of size $n=30$ and compute the sample mean.

**Instructions:**

1. Use `np.random.choice()` to draw a random sample of size 30 from the population

2. Compute the sample mean using `.mean()`

3. Compare the sample mean to the population mean

4. Repeat this process 2-3 times (with different random seeds) to see how the sample mean varies

**Starter code:**

```python

# Draw a random sample of size 30 (with replacement, so draws are independent)

n = 30

sample = np.random.choice(df_2014, size=n, replace=True)

# Compute sample mean

sample_mean = sample.mean()

print(f"Sample size: {n}")

print(f"Sample mean: ${sample_mean:.2f}")

print(f"Population mean: ${df_2014.mean():.2f}")

print(f"Difference: ${sample_mean - df_2014.mean():.2f}")

# Question: How close is the sample mean to the population mean?

```

**Questions:**

- How much does the sample mean differ from the population mean?

- If you draw another sample, will you get the same sample mean?

- What does this variability tell you about using samples for inference?

---

#### Task 3: Simulate the Sampling Distribution (Semi-guided)

**Objective:** Draw 1000 random samples of size $n=30$ and plot the distribution of sample means.

**Instructions:**

1. Use a loop to draw 1000 samples, each of size $n=30$

2. For each sample, compute and store the sample mean

3. Plot a histogram of the 1000 sample means

4. Compare this sampling distribution to the theoretical prediction from the CLT

**Hint:** The CLT predicts that sample means should be normally distributed with:

- Mean = $\mu$ (population mean)

- Standard error = $\sigma/\sqrt{n}$ (population std / sqrt(sample size))

**Example structure:**

```python

# Simulate sampling distribution

n_samples = 1000

n = 30

sample_means = []

for i in range(n_samples):

sample = np.random.choice(df_2014, size=n, replace=True) # with replacement: independent draws

sample_means.append(sample.mean())

sample_means = np.array(sample_means)

# Plot sampling distribution

fig, ax = plt.subplots(figsize=(10, 6))

ax.hist(sample_means, bins=30, edgecolor='black', alpha=0.7, density=True)

ax.axvline(df_2014.mean(), color='red', linestyle='--', linewidth=2, label='Population mean')

ax.axvline(sample_means.mean(), color='blue', linestyle=':', linewidth=2, label='Mean of sample means')

ax.set_xlabel('Sample Mean (output per worker, 2011 USD PPP)')

ax.set_ylabel('Density')

ax.set_title(f'Sampling Distribution of the Mean (n={n}, {n_samples} samples)')

ax.legend()

plt.tight_layout()

plt.show()

# Compare empirical vs theoretical

print(f"Population mean (μ): ${df_2014.mean():.2f}")

print(f"Mean of sample means: ${sample_means.mean():.2f}")

print(f"Theoretical SE (σ/√n): ${df_2014.std()/np.sqrt(n):.2f}")

print(f"Empirical SE (std of sample means): ${sample_means.std():.2f}")

```

**Questions:**

- Does the distribution of sample means look approximately normal (even though the population distribution was skewed)?

- How close is the mean of sample means to the population mean?

- How close is the empirical standard error to the theoretical prediction?

---

> **Key Concept 3.11: Standard Error and Precision**

>

> The **standard error** $SE(\bar{y}) = \sigma/\sqrt{n}$ (estimated in practice by $s/\sqrt{n}$, since $\sigma$ is unknown) measures the typical distance between a sample mean and the population mean. Key insights:

>

> 1. **Decreases with sample size**: Doubling the sample size reduces SE by factor of $\sqrt{2} \approx 1.41$

> 2. **Trade-off**: Larger samples cost more (time/money) but provide more precise estimates

> 3. **Diminishing returns**: Going from $n=25$ to $n=100$ reduces SE by half, but $n=100$ to $n=400$ also reduces by half

>

> In economic research, sample size is often limited by data availability, requiring careful attention to precision.

---

#### Task 4: Investigate the Effect of Sample Size (More Independent)

**Objective:** Compare sampling distributions for different sample sizes ($n = 10, 30, 50, 100$).

**Instructions:**

1. For each sample size, simulate 1000 samples and compute sample means

2. Plot the four sampling distributions on the same graph (or use subplots)

3. Compare the standard errors across sample sizes

4. Verify that $SE$ decreases as $1/\sqrt{n}$

**Key questions to answer:**

- How does the shape of the sampling distribution change with sample size?

- How much does precision improve when you quadruple the sample size (e.g., $n=25$ to $n=100$)?

- At what sample size does the distribution start to look clearly normal?

---

#### Task 5: Comparing High-Income vs Developing Countries (Independent)

**Objective:** Investigate whether sampling distributions differ for subpopulations (high-income vs developing countries).

**Instructions:**

1. Split the 2014 data by `hi1990` (high-income indicator)

2. For each group, simulate the sampling distribution of the mean (use $n=20$, 1000 samples)

3. Plot both sampling distributions on the same graph

4. Compare means and standard errors between groups

**Research question:** Do high-income and developing countries have different average productivity levels? How confident can we be in this difference based on samples?

**Hints:**

- Use `df.loc[(slice(None), 2014), ['lp', 'hi1990']].dropna()` to get both variables

- Filter by `hi1990 == 'yes'` and `hi1990 == 'no'`

- Compare population means and sampling distribution characteristics

---

#### Task 6: Design Your Own Sampling Experiment (Independent)

**Objective:** Explore a question of your choice using sampling distributions.

**Choose ONE of the following:**

**Option A:** Effect of outliers on sample means

- Remove the top 5% most productive countries (outliers)

- Compare sampling distributions with vs without outliers

- Question: How sensitive is the sample mean to extreme values?

**Option B:** Time trends in sampling distributions

- Compare sampling distributions for years 1990, 2000, 2010, 2014

- Question: Has average productivity increased over time? Has variability changed?

**Option C:** Regional sampling distributions

- Split countries by region (use `region` variable)

- Compare sampling distributions across regions

- Question: Which regions show the highest/lowest productivity? Most/least variability?

**Your analysis should include:**

1. Clear research question

2. Appropriate sample size(s)

3. Simulated sampling distribution(s) with visualizations

4. Statistical summary (means, standard errors)

5. Economic interpretation: What does this tell us about global productivity patterns?

---

#### What You've Learned from This Case Study

Through this hands-on exploration of sampling distributions using cross-country productivity data, you've applied all Chapter 3 concepts:

- **Population vs sample**: Understood the difference and why we use samples for inference

- **Sample mean**: Computed point estimates from random samples

- **Sampling variability**: Observed how sample means vary across different samples

- **Sampling distribution**: Simulated and visualized the distribution of sample means

- **Central Limit Theorem**: Verified that sample means are approximately normal even for skewed populations

- **Standard error**: Quantified precision and understood how it decreases with sample size ($\sigma/\sqrt{n}$)

- **Effect of sample size**: Compared sampling distributions for different $n$ values

- **Subpopulation analysis**: Explored differences across country groups

---

**Connection to the Research:** Understanding sampling distributions is fundamental to the convergence clubs analysis. When researchers estimate average productivity for a club, they're working with samples and must account for sampling variability. The tools you practiced here—computing sample means, quantifying precision, understanding the CLT—are essential for all statistical inference in economics.

**Looking ahead:**

- **Chapter 4:** Statistical inference (confidence intervals, hypothesis tests) builds directly on sampling distributions

- **Chapter 5-9:** Regression analysis extends these concepts to relationships between variables

- **Chapter 10-17:** Advanced methods for causal inference and panel data

---