---

title: 7. Statistical Inference for Bivariate Regression

execute:

enabled: true

warning: false

---

**metricsAI: An Introduction to Econometrics with Python and AI in the Cloud**

*[Carlos Mendez](https://carlos-mendez.org)*

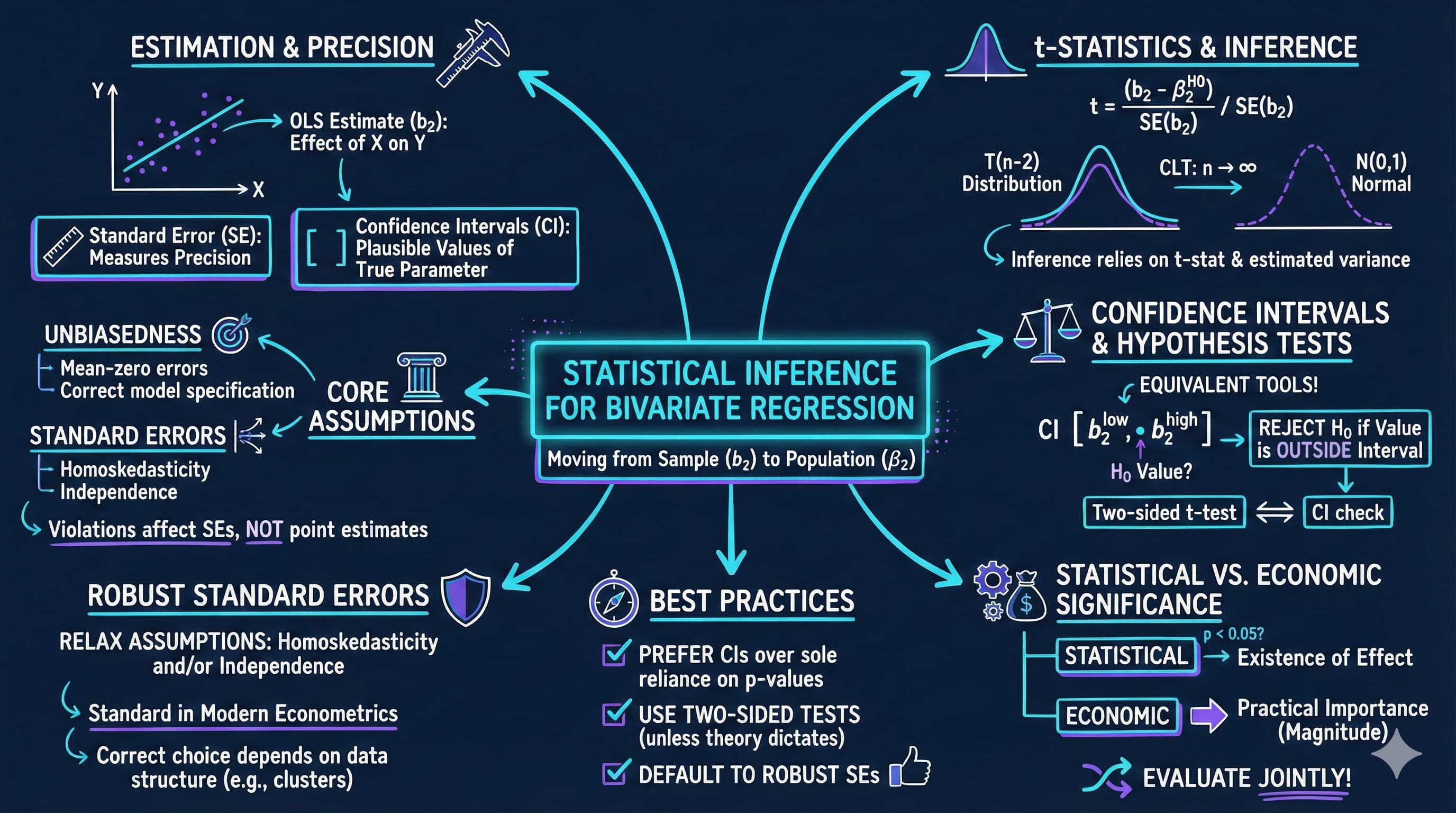

<img src="https://raw.githubusercontent.com/quarcs-lab/metricsai/main/images/ch07_visual_summary.jpg" alt="Chapter 07 Visual Summary" width="100%">

This notebook provides an interactive introduction to statistical inference for bivariate regression models. All code runs directly in Google Colab without any local setup.

[](https://colab.research.google.com/github/quarcs-lab/metricsai/blob/main/notebooks_colab/ch07_Statistical_Inference_for_Bivariate_Regression.ipynb)

<div class="chapter-resources">

<a href="https://www.youtube.com/watch?v=iMi1Fa-PYLs" target="_blank" class="resource-btn">🎬 AI Video</a>

<a href="https://carlos-mendez.my.canva.site/s07-statistical-inference-for-bivariate-regression-pdf" target="_blank" class="resource-btn">✨ AI Slides</a>

<a href="https://cameron.econ.ucdavis.edu/aed/traedv1_07" target="_blank" class="resource-btn">📊 Cameron Slides</a>

<a href="https://app.edcafe.ai/quizzes/697866e42f5d08069e04934f" target="_blank" class="resource-btn">✏️ Quiz</a>

<a href="https://app.edcafe.ai/chatbots/69789f042f5d08069e070885" target="_blank" class="resource-btn">🤖 AI Tutor</a>

</div>

## Chapter Overview

This chapter extends statistical inference from univariate to bivariate regression. You'll gain both theoretical understanding and practical skills through hands-on Python examples, learning how to test hypotheses about regression coefficients and construct confidence intervals.

**What you'll learn:**

- The t-statistic for testing hypotheses about regression coefficients

- Constructing and interpreting confidence intervals for slope parameters

- Tests of statistical significance (whether a regressor matters)

- Two-sided hypothesis tests for specific parameter values

- One-sided directional hypothesis tests

- Heteroskedasticity-robust standard errors and their importance

- Economic vs. statistical significance

**Dataset used:**

- **AED_HOUSE.DTA**: House prices and characteristics for 29 houses sold in Central Davis, California in 1999 (price, size, bedrooms, bathrooms, lot size, age)

**Chapter outline:**

- 7.1 Example: House Price and Size

- 7.2 The t Statistic

- 7.3 Confidence Intervals

- 7.4 Tests of Statistical Significance

- 7.5 Two-Sided Hypothesis Tests

- 7.6 One-Sided Directional Hypothesis Tests

- 7.7 Robust Standard Errors

- Key Takeaways

- Practice Exercises

- Case Studies

## Key Concepts

Six core ideas anchor this chapter. Skim them before you start, and come back when a term feels fuzzy. Each entry pairs a concrete example using the chapter's data with a non-technical analogy. Click a panel to expand it.

**Null Hypothesis for the Slope ($H_0: \beta_2 = 0$):** The default claim that the explanatory variable has *no* linear effect on the outcome — i.e., the population slope is exactly zero. Rejecting this null is what allows the analyst to say "$x$ matters for $y$".

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

For the 29 Davis houses, we test $H_0: \beta_2 = 0$ against $H_a: \beta_2 \neq 0$ on the regression of `price` on `size`. The fitted slope is $b_2 = \$73.77$/sq ft with $\operatorname{se}(b_2) = 11.17$ — a slope this far from zero, this precisely estimated, is the evidence that overturns the null.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

A courtroom presumes the defendant innocent — the regression presumes the regressor irrelevant. Both are starting points the data must overturn. Until the prosecution piles up enough evidence, the defendant walks free; until the slope's t-statistic is big enough, $\beta_2 = 0$ stands.

:::

::::

:::::

**t-Statistic for the Slope:** The standardised distance between the estimated slope and its null-hypothesised value, in standard-error units: $t = (b_2 - \beta_2^0)/\operatorname{se}(b_2)$. For the common $H_0: \beta_2 = 0$, this simplifies to $t = b_2/\operatorname{se}(b_2)$, and $|t|$ above the critical value triggers rejection.

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

For the Davis house regression with $b_2 = 73.77$ and $\operatorname{se}(b_2) = 11.17$, the t-statistic on `size` is $t = 73.77 / 11.17 = 6.60$. The slope sits 6.6 standard errors above zero — far beyond the comfortable noise range — so the chapter rejects $H_0: \beta_2 = 0$ at any conventional significance level.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

A fitness tracker counts your daily steps but also reports a *signal-to-noise ratio*: how confident it is that you're actually walking versus jiggling at your desk. The t-statistic is exactly that ratio for a slope — how many step-counts (sample slope) the watch saw, scaled by how jumpy its baseline (standard error) tends to be.

:::

::::

:::::

**Standard Error of the Slope Coefficient ($\operatorname{se}(b_2)$):** The estimated standard deviation of the OLS slope estimator across hypothetical resamples. It shrinks with better model fit (small $s_e$), more observations, and wider spread in $x$ — the three knobs an analyst can turn to sharpen inference.

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

For the Davis houses, $\operatorname{se}(b_2) = 11.17$ — meaning the slope on `size` would jitter by roughly \$11/sq ft from one sample of 29 houses to another. With $n = 29$, $s_e \approx \$23{,}551$, and the spread $\sigma_{\text{size}} \approx 398$ sq ft, the formula $\operatorname{se}(b_2) = s_e / \sqrt{\sum(x_i - \bar{x})^2}$ produces this estimate; quadrupling $n$ would roughly halve it.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

An archer measures her group size — the diameter of the cluster of arrows around the bullseye — across many practice rounds. A tight group (small SE) means the next shot will land predictably; a spray pattern (large SE) means the next shot could go anywhere. $\operatorname{se}(b_2)$ is the slope's group size from imagined re-runs of the regression.

:::

::::

:::::

**Critical t-Value ($t_{n-2,\,\alpha/2}$):** The cutoff value on the $t$-distribution beyond which the null hypothesis is rejected. For a two-sided test at $\alpha = 0.05$ with $n-2$ degrees of freedom, observed $|t|$ values above this cutoff land in the rejection region.

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

For the Davis house regression, $n = 29$ gives $n - 2 = 27$ degrees of freedom. At $\alpha = 0.05$ two-sided, the critical value is $t_{27,\,0.025} = 2.052$. The observed $|t| = 6.60$ is more than three times this cutoff, so the slope's t-statistic falls deep into the rejection region.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

A playground swing is fitted with a "max-height" sensor: cross it, and the operator pulls the safety brake. The critical value is that statistical max-height. Test statistics that swing higher than the line trigger the rejection brake; those that stay below are within the safe range.

:::

::::

:::::

**Margin of Error for the Slope:** The half-width of a confidence interval for $\beta_2$ — the quantity $t_{n-2,\,\alpha/2} \cdot \operatorname{se}(b_2)$ added to and subtracted from the point estimate. Bigger margin ⇒ vaguer interval; smaller margin ⇒ sharper claim.

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

For the Davis house slope, the 95% margin of error is $2.052 \times 11.17 \approx 22.93$ dollars per square foot. So the 95% confidence interval for $\beta_2$ is $73.77 \pm 22.93 = [50.84, 96.70]$ — a range that excludes \$0 but spans a substantial \$46 spread, telling us "size matters", but at a price between \$51 and \$97 per square foot.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

A photo print arrives with a paper border around the image. The margin of error is that border — the visual reminder that the photo's exact framing isn't pinned to a single line, but extends a few millimetres on either side. A wide border means a less certain crop; a narrow border means the photo's edge is precisely where you put it.

:::

::::

:::::

**Test of Statistical Significance ($H_0: \beta = 0$):** The standard hypothesis test asking "is this regressor's true coefficient distinguishable from zero, given sampling noise?" Standard regression output reports the t-statistic, the two-sided p-value, and stars ($*$, $**$, $***$) flagging the significance level at which $H_0$ is rejected.

::::: {.columns}

:::: {.column width="50%"}

::: {.callout-tip collapse="true" appearance="simple" title="Example"}

The chapter's basic regression output reports `size` with $b_2 = 73.77$, $\operatorname{se} = 11.17$, $t = 6.60$, $p \approx 0.000$ — every column tells the same story: the test of significance rejects $H_0: \beta_2 = 0$ overwhelmingly. Translated: across the Davis 1999 housing market, the data leave essentially no room for the claim that size has zero effect on price.

:::

::::

:::: {.column width="50%"}

::: {.callout-note collapse="true" appearance="simple" title="Analogy"}

A metal detector swept across a beach beeps when its reading rises clearly above the background hum. A test of significance is the same beep applied to a regression coefficient: the t-statistic is the reading, the critical value sets the beep threshold, and the p-value tells you the chance of hearing a beep on an empty patch of sand. A loud, sharp beep means dig.

:::

::::

:::::

## Setup

First, we import the necessary Python packages and configure the environment for reproducibility. All data will stream directly from GitHub.

```{python}

#| code-fold: true

#| code-summary: "Setup: Import libraries and configure environment"

# --- Libraries ---

import numpy as np # numerical operations

import pandas as pd # data manipulation

import matplotlib.pyplot as plt # plotting

import seaborn as sns # statistical visualizations

import pyfixest as pf # fast estimation with robust SEs

from scipy import stats # statistical distributions

import random

import os

# --- Reproducibility ---

RANDOM_SEED = 42

random.seed(RANDOM_SEED)

np.random.seed(RANDOM_SEED)

os.environ['PYTHONHASHSEED'] = str(RANDOM_SEED)

# --- Data source ---

GITHUB_DATA_URL = "https://raw.githubusercontent.com/quarcs-lab/data-open/master/AED/"

# --- Plotting style (dark theme matching book design) ---

plt.style.use('dark_background')

sns.set_style("darkgrid")

plt.rcParams.update({

'axes.facecolor': '#1a2235',

'figure.facecolor': '#12162c',

'grid.color': '#3a4a6b',

'figure.figsize': (10, 6),

'text.color': 'white',

'axes.labelcolor': 'white',

'xtick.color': 'white',

'ytick.color': 'white',

'axes.edgecolor': '#1a2235',

})

print("Setup complete! Ready to explore statistical inference for bivariate regression.")

```

## 7.1 Example: House Price and Size

We begin with a motivating example: the relationship between house price and house size.

**The regression model:**

$$\text{price} = \beta_1 + \beta_2 \times \text{size} + u$$

where:

- $\text{price}$ is the house sale price (in dollars)

- $\text{size}$ is the house size (in square feet)

- $\beta_2$ is the population slope (price increase per square foot)

- $b_2$ is the sample estimate of $\beta_2$

**Key regression output:**

| Variable | Coefficient | Standard Error | t-statistic | p-value | 95% CI |

|----------|-------------|----------------|-------------|---------|--------|

| Size | 73.77 | 11.17 | 6.60 | 0.000 | [50.84, 96.70] |

| Intercept | 115,017.28 | 21,489.36 | 5.35 | 0.000 | [70,924.76, 159,109.8] |

**Interpretation:**

- Each additional square foot is associated with approximately \$73.77 higher house price

- The standard error (11.17) measures uncertainty in this estimate

- The t-statistic (6.60) tests whether the effect is statistically significant

- The 95% confidence interval is [50.84, 96.70]

First, we load the AED house-price dataset and inspect its summary statistics — confirm the sample has 29 houses and that `price` and `size` are on sensible scales (dollars and square feet).

```{python}

# 7.1 Example: House price and size

data_house = pd.read_stata(GITHUB_DATA_URL + 'AED_HOUSE.DTA')

# Data summary

data_house.describe()

```

The sample covers 29 houses: the average sale price is about \$253,910 and the average size about 1,883 square feet, with no implausible values in any variable.

### Basic Regression: Price on Size

We estimate the bivariate regression model using ordinary least squares (OLS).

```{python}

# Table 7.1 - Basic regression

model_basic = pf.feols('price ~ size', data=data_house)

# Key results

intercept = model_basic.coef()['Intercept']

slope = model_basic.coef()['size']

r_squared = model_basic._r2

print(f"Estimated equation: price = {intercept:,.2f} + {slope:.2f} x size")

print(f"Slope: each additional sq ft is associated with ${slope:,.2f} higher price")

print(f"R-squared: {r_squared:.4f} ({r_squared*100:.1f}% of variation explained)\n")

# Full regression output

model_basic.summary()

```

### Coefficient Table

Let's create a clean table showing the key statistics for statistical inference.

```{python}

# Save coefficients in a clean table

coef_table = pd.DataFrame({

'Coefficient': model_basic.coef(),

'Std. Error': model_basic.se(),

't-statistic': model_basic.tstat(),

'p-value': model_basic.pvalue()

})

# Coefficient table

coef_table

```

## 7.2 The t Statistic

The t-statistic is fundamental to statistical inference in regression.

**Statistical inference problem:**

- **Sample**: $\hat{y} = b_1 + b_2 x$ where $b_1$ and $b_2$ are least squares estimates

- **Population**: $E[y|x] = \beta_1 + \beta_2 x$ and $y = \beta_1 + \beta_2 x + u$

- **Goal**: Make inferences about the slope parameter $\beta_2$

**The t-statistic:**

$$T = \frac{\text{estimate} - \text{parameter}}{\text{standard error}} = \frac{b_2 - \beta_2}{se(b_2)} \sim T(n-2)$$

**Why use the T(n-2) distribution?**

Under assumptions 1-4:

- $Var[b_2] = \sigma_u^2 / \sum_{i=1}^n (x_i - \bar{x})^2$

- We don't know $\sigma_u^2$, so we replace it with $s_e^2 = \frac{1}{n-2} \sum_{i=1}^n (y_i - \hat{y}_i)^2$

- This introduces additional uncertainty, so we use $T(n-2)$ instead of $N(0,1)$

**Model Assumptions (1-4):**

1. The population model is $y = \beta_1 + \beta_2 x + u$

2. The error has mean zero conditional on x: $E[u_i | x_i] = 0$

3. The error has constant variance: $Var[u_i | x_i] = \sigma_u^2$

4. The errors are statistically independent: $u_i$ independent of $u_j$

### Understanding Standard Errors: The Foundation of Inference

**What is a standard error?**

The standard error measures the uncertainty in our estimate. It answers: "If we repeatedly sampled from the population and computed b₂ each time, how much would b₂ vary across samples?"

**Key distinction:**

- **Standard deviation**: Variability of individual observations (data spread)

- **Standard error**: Variability of the estimate across samples (estimation uncertainty)

**Formula for SE of the slope:**

$$se(b_2) = \frac{\sigma_u}{\sqrt{\sum_{i=1}^n (x_i - \bar{x})^2}} = \frac{\sigma_u}{\sqrt{n} \cdot \sigma_x}$$

where:

- σ_u = standard deviation of the error term

- σ_x = standard deviation of x

- n = sample size

**What affects the standard error?**

**1. Error variance (σ²_u): Larger σ_u → Larger SE**

- More unexplained variation in y

- Data points farther from regression line

- Less precise estimates

**2. Sample size (n): Larger n → Smaller SE**

- More data reduces uncertainty

- SE decreases at rate 1/√n

- Quadruple n to halve SE

**3. Variation in x (σ_x): Larger σ_x → Smaller SE**

- More spread in x provides more information

- Extreme x values help identify the slope

- Concentrated x values give less precision

**Intuition:**

Think of the regression line as a seesaw balanced at (x̄, ȳ):

- With wide spread in x: Small changes in slope make big differences at the extremes (easy to detect slope)

- With narrow spread in x: Hard to distinguish different slopes (difficult to detect slope)

**Example calculation for our house price data:**

Given:

- Sample size: n = 29

- Standard error of regression: s_e ≈ 23,551

- Standard deviation of size: σ_x ≈ 398

- Estimated SE(b₂) = 23,551 / (√29 × 398) ≈ 11.0

(Actual SE is 11.17; the shortcut formula is slightly smaller because it uses √n in place of √(n-1))

**Why standard errors matter:**

1. **Confidence intervals**: CI = b₂ ± t × SE(b₂)

2. **Hypothesis tests**: t = (b₂ - β₂⁰) / SE(b₂)

3. **Practical significance**: Small SE → precise estimate → more reliable

4. **Study design**: Calculate required n for desired SE

**Relationship to R²:**

Higher R² (better fit) → Smaller σ_u → Smaller SE → More precise estimates

For our house price example:

- R² = 0.62 (size explains 62% of price variation)

- This gives relatively small SE

- If R² were 0.10, SE would be about 1.5 times larger (SE scales with √(1-R²))

The cell below re-displays the regression output and then extracts the ingredients of the t-statistic for `size` — verify that $t = b_2 / \operatorname{se}(b_2)$ reproduces the value 6.60 shown in the table.

```{python}

# 7.2 The t statistic

model_basic.summary()

# Extract key statistics

coef_size = model_basic.coef()['size']

se_size = model_basic.se()['size']

t_stat_size = model_basic.tstat()['size']

p_value_size = model_basic.pvalue()['size']

# Detailed statistics for 'size' coefficient

print(f"Coefficient: ${coef_size:.4f}")

print(f"Standard Error: ${se_size:.4f}")

print(f"t-statistic: {t_stat_size:.4f}")

print(f"p-value: {p_value_size:.6f}")

print(f"t = b₂ / se(b₂) = {coef_size:.4f} / {se_size:.4f} = {t_stat_size:.4f}")

```

> **Key Concept 7.1: The t-Distribution and Degrees of Freedom**

>

> The **t-distribution** is used for statistical inference when the population variance is unknown (which is always the case in practice). Unlike the standard normal distribution, the t-distribution accounts for the additional uncertainty from estimating the variance.

>

> **Key properties:**

>

> - Bell-shaped and symmetric (like the normal distribution)

> - Heavier tails than the normal distribution (more probability in extremes)

> - Converges to the normal distribution as sample size increases

> - Characterized by degrees of freedom (df)

>

> **Degrees of freedom = n - 2** for bivariate regression:

>

> - Start with n observations

> - Estimate β₁ (intercept): -1 df

> - Estimate β₂ (slope): -1 df

> - Remaining df for estimating variance: n - 2

>

> **Practical implication:** For small samples (n < 30), the t-distribution's heavier tails lead to wider confidence intervals and more conservative hypothesis tests compared to the normal distribution. For large samples (n > 100), the difference becomes negligible.

## 7.3 Confidence Intervals

A confidence interval provides a range of plausible values for the population parameter.

**Formula for a \$100(1-\alpha)\%$ confidence interval:**

$$b_2 \pm t_{n-2, \alpha/2} \times se(b_2)$$

where:

- $b_2$ is the slope estimate

- $se(b_2)$ is the standard error of $b_2$

- $t_{n-2, \alpha/2}$ is the critical value from Student's t-distribution with $n-2$ degrees of freedom

**95% confidence interval (approximate):**

$$b_2 \pm 2 \times se(b_2)$$

**Interpretation:**

- If we repeatedly sampled from the population and constructed 95% CIs, approximately 95% of these intervals would contain the true parameter value $\beta_2$

- Any single calculated interval either contains $\beta_2$ or it does not — the 95% refers to the long-run success rate of the interval-construction procedure

**Example calculation for house price:**

$$\begin{aligned}

b_2 \pm t_{27, 0.025} \times se(b_2) &= 73.77 \pm 2.052 \times 11.17 \\

&= 73.77 \pm 22.93 \\

&= [50.84, 96.70]

\end{aligned}$$

> **Key Concept 7.2: Interpreting Confidence Intervals**

>

> A **confidence interval** provides a range of plausible values for the population parameter. For regression slopes, the 95% CI is:

>

> $$b_2 \pm t_{n-2, 0.025} \times se(b_2)$$

>

> **Common misconceptions:**

>

> - WRONG: "There's a 95% probability that β₂ is in this interval"

> - CORRECT: "If we repeated the sampling process many times, 95% of the constructed intervals would contain β₂"

>

> **Practical interpretation:**

>

> - The interval represents our uncertainty about the true parameter value

> - Wider intervals indicate more uncertainty (large SE, small n, or high variability)

> - Narrower intervals indicate more precision (small SE, large n, or low variability)

> - Values inside the interval are "plausible" at the chosen confidence level

> - Values outside the interval would be rejected in a hypothesis test

>

> **Relationship to hypothesis testing:** If a null value β₂* falls inside the 95% CI, we fail to reject H₀: β₂ = β₂* at the 5% significance level. This makes CIs more informative than hypothesis tests alone.

### Understanding Confidence Intervals: A Deep Dive

**What is a confidence interval?**

A confidence interval (CI) is NOT a probability statement about the parameter. Instead, it's a statement about the procedure used to construct the interval.

**Common misconceptions:**

**WRONG**: "There is a 95% probability that β₂ is between 50.84 and 96.70"

- The parameter β₂ is fixed (not random)

- The interval either contains β₂ or it doesn't

**CORRECT**: "If we repeatedly sampled and constructed 95% CIs, approximately 95% of these intervals would contain the true β₂"

- The randomness is in the sampling process

- Our particular interval is one realization from this process

**Intuitive explanation:**

Imagine conducting 100 different studies using different random samples from the same population:

- Each study estimates β₂ and constructs a 95% CI

- About 95 of the 100 intervals will contain the true β₂

- About 5 of the 100 intervals will miss β₂ (just by chance)

**Width of confidence intervals:**

The CI width depends on three factors:

$$\text{Width} = 2 \times t_{n-2, \alpha/2} \times se(b_2)$$

1. **Confidence level (1-α)**: Higher confidence → wider interval

- 90% CI: Narrower (less confident)

- 95% CI: Standard choice (balance)

- 99% CI: Wider (more confident)

2. **Sample size (n)**: Larger sample → narrower interval

- More data reduces uncertainty

- Critical value t_{n-2, α/2} decreases as n increases

3. **Variability in data**: More scatter → wider interval

- se(b₂) increases with unexplained variation

- Tighter relationship → more precise estimates

**Practical use:**

Confidence intervals are more informative than hypothesis tests because they show:

- The point estimate (center of interval)

- The precision of the estimate (width of interval)

- All null values that would not be rejected (values inside interval)

The cell below extracts the 95% confidence intervals directly from the fitted model — compare the `size` row with the hand calculation above, [50.84, 96.70].

```{python}

# 7.3 Confidence intervals

conf_int = model_basic.confint()

# 95% confidence intervals

conf_int

```

### The t-Distribution vs Normal Distribution: Why It Matters

**Why not use the normal distribution?**

In theory, when we know the population variance σ²_u, the test statistic follows a standard normal distribution:

$$Z = \frac{b_2 - \beta_2}{\sigma / \sqrt{\sum(x_i - \bar{x})^2}} \sim N(0,1)$$

**The problem:** We never know σ_u in practice!

**The solution:** Replace σ_u with its estimate s_e (residual standard error):

$$T = \frac{b_2 - \beta_2}{s_e / \sqrt{\sum(x_i - \bar{x})^2}} \sim T(n-2)$$

This substitution introduces additional uncertainty, so we use the t-distribution instead of normal.

**Properties of the t-distribution:**

1. **Shape**: Bell-shaped and symmetric (like normal)

2. **Mean**: 0 (like normal)

3. **Variance**: df/(df-2) > 1 (heavier tails than normal)

4. **Degrees of freedom**: n - 2 for bivariate regression

- n observations

- Minus 2 parameters estimated (β₁ and β₂)

**Key differences from normal:**

| Sample Size | t Critical Value (α=0.05) | z Critical Value | Difference |

|-------------|---------------------------|------------------|------------|

| n = 5 (df=3) | 3.182 | 1.96 | +62% |

| n = 10 (df=8) | 2.306 | 1.96 | +18% |

| n = 30 (df=28) | 2.048 | 1.96 | +4% |

| n = 100 (df=98) | 1.984 | 1.96 | +1% |

| n → ∞ | 1.96 | 1.96 | 0% |

**What this means:**

- **Small samples**: t critical values much larger → wider CIs, harder to reject H₀

- **Large samples**: t ≈ normal → approximately same inference

- **Our house data**: n=29, df=27, t(0.025) = 2.052 vs z = 1.96

**Why degrees of freedom = n - 2?**

- Start with n observations

- Estimate β₁ (intercept): loses 1 df

- Estimate β₂ (slope): loses 1 df

- Remaining df for estimating variance: n - 2

**Practical implications:**

**For n = 29 (our house price data):**

- Using normal: 95% CI margin = 1.96 × 11.17 ≈ 21.90

- Using t(27): 95% CI margin = 2.052 × 11.17 ≈ 22.93

- Difference: 5% wider with t-distribution (more conservative)

**For n = 10 (small sample):**

- Using normal: 95% CI margin = 1.96 × SE

- Using t(8): 95% CI margin = 2.306 × SE

- Difference: 18% wider with t-distribution (much more conservative!)

**Rule of thumb:**

- n < 30: Must use t-distribution

- 30 ≤ n < 100: Use t-distribution (small difference)

- n ≥ 100: Normal approximation usually fine, but still use t

**Modern practice:** Statistical software always uses t-distribution (why not? It's correct for any n)

**Visual intuition:**

The t-distribution has heavier tails:

- More probability in the extremes

- Less probability near the center

- This accounts for the uncertainty in estimating σ_u

- As n increases, estimation uncertainty decreases, and t → normal

### Manual Calculation of Confidence Interval

Let's manually calculate the confidence interval for the size coefficient to understand the mechanics.

```{python}

# Manual calculation of confidence interval for size

n = len(data_house)

df = n - 2

# 0.975 = upper tail for 95% two-sided CI (2.5% in each tail)

t_crit = stats.t.ppf(0.975, df)

ci_lower = coef_size - t_crit * se_size

ci_upper = coef_size + t_crit * se_size

# Manual calculation for 'size' coefficient

print(f"Sample size: {n}")

print(f"Degrees of freedom: {df}")

print(f"Critical t-value (α=0.05): {t_crit:.4f}")

print(f"Margin of error: {t_crit * se_size:.4f}")

print(f"95% CI: [${ci_lower:.4f}, ${ci_upper:.4f}]")

```

The manual calculation matches pyfixest's `confint()` output exactly: the margin of error $2.052 \times 11.17 \approx 22.93$ yields the interval $[50.84, 96.70]$, a spread of roughly \$46 per square foot around the point estimate.

## 7.4 Tests of Statistical Significance

A regressor $x$ has no relationship with $y$ if $\beta_2 = 0$.

**Test of statistical significance** (two-sided test):

$$H_0: \beta_2 = 0 \quad \text{vs.} \quad H_a: \beta_2 \neq 0$$

**Test statistic:**

$$t = \frac{b_2}{se(b_2)} \sim T(n-2)$$

**Decision rules:**

1. **p-value approach**: Reject $H_0$ at level $\alpha$ if $p = Pr[|T_{n-2}| > |t|] < \alpha$

2. **Critical value approach**: Reject $H_0$ at level $\alpha$ if $|t| > c = t_{n-2, \alpha/2}$

**For the house price example:**

- $t = 73.77 / 11.17 = 6.60$

- $p = Pr[|T_{27}| > 6.60] \approx 0.000$

- Critical value: $c = t_{27, 0.025} = 2.052$

- Since $|t| = 6.60 > 2.052$, reject $H_0$

- **Conclusion**: House size is statistically significant at the 5% level

> **Key Concept 7.3: The Hypothesis Testing Framework**

>

> **Hypothesis testing** is a formal procedure for making decisions about population parameters. The key steps are:

>

> **1. State the hypotheses:**

>

> - **Null hypothesis (H₀)**: The claim we're testing (usually "no effect")

> - **Alternative hypothesis (Hₐ)**: What we conclude if we reject H₀

>

> **2. Choose significance level (α):**

>

> - Common choices: 0.10, 0.05, 0.01

> - α = probability of Type I error (rejecting H₀ when it's true)

>

> **3. Calculate test statistic:**

>

> - Standardizes the difference: t = (estimate - null value) / SE

>

> **4. Determine p-value:**

>

> - Probability of observing our result (or more extreme) if H₀ is true

> - Smaller p-value = stronger evidence against H₀

>

> **5. Make decision:**

>

> - Reject H₀ if p-value < α

> - Fail to reject H₀ if p-value ≥ α (never "accept" H₀)

>

> **Understanding p-values:** If p = 0.001, this means "if H₀ were true, we'd observe a result this extreme only 0.1% of the time." This is strong evidence against H₀.

> **Key Concept 7.4: Statistical vs. Economic Significance**

>

> **Statistical significance** and **economic significance** are distinct concepts that answer different questions:

>

> **Statistical Significance:**

>

> - **Question:** Is the effect different from zero?

> - **Determined by:** t-statistic = b₂ / se(b₂), which depends on sample size, variability, and effect size

> - **Interpretation:** We can confidently say the effect exists (not due to chance)

>

> **Economic Significance:**

>

> - **Question:** Is the effect large enough to matter in practice?

> - **Determined by:** The magnitude of b₂ and the context

> - **Interpretation:** The effect has real-world importance

>

> **Why they can diverge:**

>

> 1. **Large n:** Even tiny effects become statistically significant

> - Example: β₂ = \$0.01 with n = 10,000 might have p < 0.001 but be economically trivial

> 2. **Small n:** Large effects may not reach statistical significance

> - Example: β₂ = \$100 with n = 10 might have p = 0.12 but be economically important

>

> **Best practice:** Always report both the coefficient estimate (economic magnitude) and the standard error/confidence interval (statistical precision). Focus on confidence intervals, which show both dimensions simultaneously.

> **Key Concept 7.5: One-Sided vs. Two-Sided Tests**

>

> The choice between one-sided and two-sided tests depends on your research question:

>

> **Two-Sided Test (Most Common):**

>

> - H₀: β₂ = β₂* vs. Hₐ: β₂ ≠ β₂*

> - Detects deviations in either direction

> - Standard practice in academic research

> - Rejection region: Both tails of t-distribution

>

> **One-Sided Test (Directional):**

>

> - Upper: H₀: β₂ ≤ β₂* vs. Hₐ: β₂ > β₂*

> - Lower: H₀: β₂ ≥ β₂* vs. Hₐ: β₂ < β₂*

> - Detects deviations in one specific direction

> - Rejection region: One tail only

>

> **Key relationship:** For the same test statistic, one-sided p-value = (two-sided p-value) / 2 (if sign is correct)

>

> **When to use one-sided tests:**

>

> - Strong theoretical prediction of direction (before seeing data)

> - Only care about deviations in one direction

> - Be cautious: Journals typically require two-sided tests

>

> **Important:** If your data contradicts the predicted direction, you cannot reject H₀ with a one-sided test (p-value > 0.5).

### Example with Artificial Data

To illustrate the concepts more clearly, let's work with a simple artificial dataset.

```{python}

# Example with artificial data

x = np.array([1, 2, 3, 4, 5])

y = np.array([1, 2, 2, 2, 3])

df_artificial = pd.DataFrame({'x': x, 'y': y})

model_artificial = pf.feols('y ~ x', data=df_artificial)

model_artificial.summary()

coef_x = model_artificial.coef()['x']

se_x = model_artificial.se()['x']

n_art = len(x)

df_art = n_art - 2

t_crit_art = stats.t.ppf(0.975, df_art) # 0.975 = upper tail for 95% two-sided CI

ci_lower_art = coef_x - t_crit_art * se_x

ci_upper_art = coef_x + t_crit_art * se_x

# Manual CI for artificial data

print(f"Coefficient: {coef_x:.4f}")

print(f"Standard Error: {se_x:.4f}")

print(f"95% CI: [{ci_lower_art:.4f}, {ci_upper_art:.4f}]")

```

With only $n = 5$ observations, the degrees of freedom drop to 3 and the critical value jumps to $t_{3,\,0.025} = 3.182$, so the 95% interval $[0.03, 0.77]$ is very wide relative to the slope estimate of 0.40 — a concrete illustration of how small samples inflate the margin of error.

### Understanding Hypothesis Testing: The Complete Workflow

**The hypothesis testing framework:**

Hypothesis testing is a formal procedure for making decisions about population parameters using sample data.

**Step-by-step workflow:**

**1. State the hypotheses**

- **Null hypothesis (H₀)**: The claim we're testing (usually "no effect")

- **Alternative hypothesis (Hₐ)**: What we conclude if we reject H₀

- Example: H₀: β₂ = 0 vs Hₐ: β₂ ≠ 0

**2. Choose the significance level (α)**

- Common choices: 0.10, 0.05, 0.01

- α = probability of rejecting H₀ when it's actually true (Type I error)

- Convention: α = 0.05 (5% significance level)

**3. Calculate the test statistic**

- Formula: t = (b₂ - β₂⁰) / se(b₂)

- This standardizes the difference between estimate and null value

- Under H₀, t follows a t-distribution with n-2 degrees of freedom

**4. Determine the p-value**

- p-value = probability of observing a test statistic as extreme as ours if H₀ is true

- Smaller p-value = stronger evidence against H₀

- p-value < α → reject H₀

**5. Make a decision**

- **Reject H₀**: Strong evidence against the null hypothesis

- **Fail to reject H₀**: Insufficient evidence to reject the null

- Note: We never "accept" H₀, we only fail to reject it

**6. State the conclusion**

- Translate the statistical decision into plain language

- Example: "House size has a statistically significant effect on price at the 5% level"

**Understanding p-values:**

The p-value answers this question: "If the null hypothesis were true, what is the probability of getting a result at least as extreme as what we observed?"

**Example interpretation:**

- p = 0.000: If β₂ were truly zero, the probability of getting |t| ≥ 6.60 is less than 0.1%

- This is very unlikely, so we have strong evidence against H₀

**Two approaches to hypothesis testing:**

1. **p-value approach**: Reject H₀ if p-value < α

2. **Critical value approach**: Reject H₀ if |t| > critical value

Both approaches always give the same conclusion!

**Common significance levels and interpretations:**

| p-value | Interpretation | Strength of Evidence |

|---------|----------------|---------------------|

| p > 0.10 | Not significant | Weak/no evidence |

| 0.05 < p ≤ 0.10 | Marginally significant | Moderate evidence |

| 0.01 < p ≤ 0.05 | Significant | Strong evidence |

| p ≤ 0.01 | Highly significant | Very strong evidence |

### Statistical Significance vs Economic Significance

A crucial distinction that is often confused:

**Statistical Significance**

- Answers: "Is the effect different from zero?"

- Depends on: Sample size, variability, effect size

- Formula: t = b₂ / se(b₂)

- Interpretation: We can confidently say the effect exists

**Economic Significance**

- Answers: "Is the effect large enough to matter?"

- Depends on: The magnitude of b₂ and context

- Requires: Domain knowledge and practical judgment

- Interpretation: The effect has real-world importance

**Key insights:**

**1. Statistical significance ≠ Economic significance**

You can have:

- Statistically significant but economically trivial effects

- Example: With n=10,000, β₂ = 0.001 might be statistically significant but meaningless

- Economically important but statistically insignificant effects

- Example: With n=10, β₂ = 100 might not be statistically significant but potentially important

**2. Sample size matters for statistical significance**

$$t = \frac{b_2}{se(b_2)} = \frac{b_2}{\sigma_u / \sqrt{\sum(x_i - \bar{x})^2}}$$

As sample size increases:

- The denominator (standard error) decreases

- The t-statistic increases

- Small effects become statistically significant

**3. Economic significance requires context**

For the house price example:

- Statistical result: β₂ = 73.77, highly significant (p < 0.001)

- Economic interpretation: Each additional sq ft is associated with \$73.77 higher price

- Context matters:

- For a 100 sq ft difference: \$7,377 difference (substantial!)

- For a 10 sq ft difference: \$737.70 difference (moderate)

- This is economically meaningful in the housing market

**Practical guidance:**

1. **Always report both**:

- The coefficient estimate (economic magnitude)

- The p-value or confidence interval (statistical precision)

2. **Focus on confidence intervals**:

- Shows both statistical and economic significance

- Example: 95% CI = [50.84, 96.70]

- Interpretation: Effect is between \$50.84 and \$96.70 per sq ft

- Even the lower bound is economically meaningful

3. **Consider practical importance**:

- Would anyone change their behavior based on this result?

- Is the effect large enough to justify policy interventions?

- Does the effect matter in real-world terms?

**Example of the distinction:**

Suppose we study the effect of an expensive job training program on wages:

- Statistical result: Training increases wages by \$0.50/hour (p = 0.001)

- Statistical significance: YES (highly significant)

- Economic significance: Questionable

- Annual benefit: \$0.50 × 2000 hours = \$1,000

- If program costs \$10,000, not worth it

- If program costs \$500, might be worth it

**Bottom line:** Statistical significance tells you the effect exists. Economic significance tells you whether you should care.

### Understanding Two-Sided vs One-Sided Tests

**When to use which test?**

The choice between two-sided and one-sided tests depends on your research question and what you want to conclude.

**Two-Sided Test (Most Common)**

**Setup:**

- H₀: β₂ = β₂*

- Hₐ: β₂ ≠ β₂*

**Use when:**

- You want to detect any difference from the null value

- You don't have a strong prior about the direction

- You want to be conservative (standard practice in research)

**Rejection region:** Both tails of the distribution

**Example:** Does house size affect price?

- H₀: β₂ = 0 (no effect)

- Hₐ: β₂ ≠ 0 (some effect, positive or negative)

- We reject if the effect is either very positive or very negative

**One-Sided Test (Directional)**

**Setup (upper tail):**

- H₀: β₂ ≤ β₂*

- Hₐ: β₂ > β₂*

**Setup (lower tail):**

- H₀: β₂ ≥ β₂*

- Hₐ: β₂ < β₂*

**Use when:**

- You have a specific directional hypothesis

- Economic theory predicts a specific direction

- You only care about deviations in one direction

**Rejection region:** One tail of the distribution

**Example:** Does house size increase price by less than \$90/sq ft?

- Claim: β₂ < 90

- H₀: β₂ ≥ 90 (null is opposite of claim)

- Hₐ: β₂ < 90 (this is what we want to prove)

- We only reject if the effect is significantly below 90

**Mathematical relationship:**

For the same test statistic t:

- Two-sided p-value = 2 × Pr[T > |t|]

- One-sided p-value = Pr[T > t] (upper tail) or Pr[T < t] (lower tail)

- One-sided p-value = (Two-sided p-value) / 2 (if sign is correct)

**Important considerations:**

**1. Direction matters for one-sided tests**

- If testing Hₐ: β₂ > β₂* but get b₂ < β₂*, you CANNOT reject H₀

- The data contradicts your hypothesis, so rejection is impossible

- In this case, one-sided p-value > 0.5

**2. Two-sided tests are safer**

- Academic journals typically require two-sided tests

- Avoids "fishing" for significant results

- More conservative approach

**3. One-sided tests have more power**

- For the same significance level α, easier to reject in the predicted direction

- Critical value is smaller: t(n-2, α) vs t(n-2, α/2)

- Example: For α = 0.05 and df = 27

- Two-sided: t(27, 0.025) = 2.052

- One-sided: t(27, 0.05) = 1.703

**Practical example from our house price data:**

**Question 1: Does size affect price? (Two-sided)**

- H₀: β₂ = 0 vs Hₐ: β₂ ≠ 0

- t = 6.60, p-value = 0.000 (two-sided)

- Conclusion: Reject H₀, size affects price

**Question 2: Does size increase price? (One-sided)**

- H₀: β₂ ≤ 0 vs Hₐ: β₂ > 0

- t = 6.60, p-value = 0.000 / 2 = 0.000 (one-sided)

- Conclusion: Reject H₀, size increases price

**Question 3: Does size increase price by less than \$90/sq ft? (One-sided)**

- H₀: β₂ ≥ 90 vs Hₐ: β₂ < 90

- t = (73.77 - 90) / 11.17 = -1.452

- p-value = 0.079 (one-sided, lower tail)

- Conclusion: Fail to reject H₀ at α = 0.05 (but would reject at α = 0.10)

**Decision rule:**

Use two-sided tests unless:

1. You have strong theoretical reasons for a directional hypothesis

2. You specified the direction before seeing the data

3. You only care about deviations in one direction (rare in economics)

Back to the house-price data: the next cell carries out the test of statistical significance for `size`, checking both decision rules — the p-value against $\alpha = 0.05$ and $|t|$ against the critical value 2.052.

```{python}

# 7.4 Tests of statistical significance

# Null hypothesis: β₂ = 0 (size has no effect on price)

print(f"t-statistic: {t_stat_size:.4f}")

print(f"p-value: {p_value_size:.6f}")

print(f"Critical value (α=0.05): ±{t_crit:.4f}")

if p_value_size < 0.05:

print(f"\nResult: Reject H₀ at 5% significance level")

else:

print(f"\nResult: Fail to reject H₀ at 5% significance level")

```

> **Key Concept 7.6: Heteroskedasticity and Robust Standard Errors**

>

> **Heteroskedasticity** occurs when the error variance is not constant across observations: Var[u_i | x_i] = σ²_i (varies with i).

>

> **Homoskedasticity assumption** (Assumption 3): Var[u_i | x_i] = σ²_u (constant)

>

> **Why heteroskedasticity matters:**

>

> - Coefficient estimates (b₂): Still unbiased

> - Standard errors: WRONG (biased)

> - t-statistics, p-values, CIs: All invalid

>

> **Solution: Heteroskedasticity-robust standard errors**

>

> - Valid whether or not heteroskedasticity exists

> - No need to test for heteroskedasticity first

> - Modern best practice for cross-sectional data

>

> **Practical impact:**

>

> - Robust SEs usually larger → more conservative inference

> - Protects against false positives (Type I errors)

> - Sometimes smaller → gain power

>

> **Types of robust SEs:**

>

> - **HC (Heteroskedasticity-Consistent):** Cross-sectional data

> - **HAC (Heteroskedasticity and Autocorrelation Consistent):** Time series

> - **Cluster-robust:** Grouped/clustered data

>

> **Bottom line:** Always report heteroskedasticity-robust standard errors for cross-sectional data. They're free insurance against model misspecification.

## 7.5 Two-Sided Hypothesis Tests

Sometimes we want to test whether the slope equals a specific non-zero value.

**General two-sided test:**

$$H_0: \beta_2 = \beta_2^* \quad \text{vs.} \quad H_a: \beta_2 \neq \beta_2^*$$

**Test statistic:**

$$t = \frac{b_2 - \beta_2^*}{se(b_2)} \sim T(n-2)$$

**Decision rules:**

- **p-value approach**: Reject if $p = Pr[|T_{n-2}| > |t|] < \alpha$

- **Critical value approach**: Reject if $|t| > t_{n-2, \alpha/2}$

**Example**: Test whether house price increases by \$90 per square foot.

$$t = \frac{73.77 - 90}{11.17} = -1.452$$

- $p = Pr[|T_{27}| > 1.452] = 0.158$

- Since $p = 0.158 > 0.05$, do not reject $H_0$

- **Conclusion**: The data are consistent with $\beta_2 = 90$

**Relationship to confidence intervals:**

- If $\beta_2^*$ falls inside the 95% CI, do not reject $H_0$ at 5% level

- Since 90 is inside [50.84, 96.70], we do not reject

```{python}

# 7.5 Two-sided hypothesis tests

# Test H₀: β₂ = 90 vs H₁: β₂ ≠ 90

null_value = 90

t_stat_90 = (coef_size - null_value) / se_size

p_value_90 = 2 * (1 - stats.t.cdf(abs(t_stat_90), df))

t_crit_90 = stats.t.ppf(0.975, df) # 0.975 = upper tail for 95% two-sided CI

print(f"\nTest: H₀: β₂ = {null_value} vs H₁: β₂ ≠ {null_value}")

print(f" t-statistic: {t_stat_90:.4f}")

print(f" p-value: {p_value_90:.6f}")

print(f" Critical value (α=0.05): ±{t_crit_90:.4f}")

if abs(t_stat_90) > t_crit_90:

print(f"\nResult: Reject H₀ (|t| = {abs(t_stat_90):.4f} > {t_crit_90:.4f})")

else:

print(f"\nResult: Fail to reject H₀ (|t| = {abs(t_stat_90):.4f} < {t_crit_90:.4f})")

print(f"Conclusion: The data are consistent with β₂ = {null_value}")

print(f"\n95% CI for β₂: [{ci_lower:.2f}, {ci_upper:.2f}]")

print(f"Since {null_value} is inside the CI, we do not reject H₀.")

```

### Why Robust Standard Errors Matter

**The problem with default standard errors:**

Default (classical) standard errors rely on a strong assumption:

**Assumption 3 (Homoskedasticity):** Var[u_i | x_i] = σ²_u (constant variance)

This means:

- The spread of errors is the same for all values of x

- Residuals should have constant variance across fitted values

- In reality, this assumption is often violated

**What is heteroskedasticity?**

**Heteroskedasticity** means the error variance changes with x:

- Var[u_i | x_i] = σ²_i (varies with i)

- Common in cross-sectional data

- Examples:

- Income variation increases with education level

- Sales variance increases with firm size

- Medical costs vary more for older patients

**Visual detection:**

Check the residual plot (residuals vs fitted values):

- **Homoskedasticity**: Random scatter, constant spread

- **Heteroskedasticity**: Funnel shape, increasing/decreasing spread

**Consequences of heteroskedasticity:**

If heteroskedasticity is present but you use default SEs:

1. **Coefficient estimates (b₂)**: Still unbiased and consistent

2. **Standard errors**: WRONG (biased)

3. **t-statistics**: WRONG (biased)

4. **p-values**: WRONG (invalid)

5. **Confidence intervals**: WRONG (invalid coverage)

**Direction of bias:**

- Heteroskedasticity can cause SEs to be too small or too large

- Cannot predict direction without knowing the form of heteroskedasticity

- Could lead to false significance or miss true significance

**The solution: Robust standard errors**

**Heteroskedasticity-robust standard errors** (HC, White, Huber-White):

- Valid whether or not heteroskedasticity is present

- Automatically adjust for non-constant variance

- No need to test for heteroskedasticity first

- Modern best practice: Always use for cross-sectional data

**How they work:**

Default SE formula (assumes homoskedasticity):

$$se(b_2) = \frac{\sigma_u}{\sqrt{\sum(x_i - \bar{x})^2}}$$

Robust SE formula (allows heteroskedasticity):

$$se_{robust}(b_2) = \frac{\sqrt{\sum e_i^2 (x_i - \bar{x})^2}}{\sum(x_i - \bar{x})^2}$$

Key difference: Uses individual residuals e²_i instead of pooled variance σ²_u

**Practical implications:**

1. **Coefficient estimates unchanged**

- Only standard errors change

- Point estimates remain the same

2. **Standard errors typically larger**

- Robust SEs are usually (but not always) bigger

- More conservative inference

- Wider confidence intervals

3. **t-statistics typically smaller**

- Less likely to find statistical significance

- Protects against false positives

4. **Results may change qualitative conclusions**

- Variable significant with default SEs might become insignificant

- Or the reverse (if robust SEs are smaller)

**Types of robust standard errors:**

Different formulas for finite-sample adjustment:

- **HC0**: Basic White formula

- **HC1**: Degrees of freedom correction (n/(n-k)), most common in Stata

- **HC2**: Leverage-weighted

- **HC3**: Even more conservative

**Python (pyfixest):** the default is classical (iid) standard errors — request robust SEs explicitly with `vcov='HC1'`, which matches Stata's "robust" option

**For our house price example:**

| Coefficient | Standard SE | Robust SE | % Change |

|-------------|-------------|-----------|----------|

| size | 11.17 | 11.33 | +1.4% |

| Intercept | 21,489 | 20,299 | -5.5% |

- Difference is small (good news!)

- Suggests heteroskedasticity is not severe

- But always report robust SEs as standard practice

**Other types of robust SEs:**

1. **HAC (Heteroskedasticity and Autocorrelation Consistent)**

- For time series data

- Accounts for both heteroskedasticity and serial correlation

2. **Cluster-robust**

- For clustered/grouped data

- Students within schools, patients within hospitals

- Accounts for within-cluster correlation

**Best practices:**

1. **Cross-sectional data**: Always use heteroskedasticity-robust SEs

2. **Time series data**: Use HAC robust SEs (Newey-West)

3. **Panel/clustered data**: Use cluster-robust SEs

4. **When in doubt**: Use robust SEs (can't hurt, might help)

**Bottom line:** Robust standard errors provide valid inference under weaker assumptions. They're essentially free insurance against heteroskedasticity.

### Comparing Standard vs Robust Standard Errors: A Practical Guide

**How to interpret the comparison:**

When you compute both standard and robust SEs, you're essentially running two different analyses:

**Standard SEs (Classical):**

- Assumes: Homoskedasticity (constant variance)

- Valid only if: Assumption 3 holds

- Interpretation: "If errors have constant variance, here's the uncertainty"

**Robust SEs (Heteroskedasticity-Consistent):**

- Assumes: Heteroskedasticity allowed (no constant variance assumption)

- Valid: Whether or not heteroskedasticity exists

- Interpretation: "Here's the uncertainty, accounting for possible non-constant variance"

**What do differences tell us?**

**Case 1: Robust SE ≈ Standard SE (difference < 10%)**

- Example: Our house price data (11.33 vs 11.17)

- Interpretation: Little evidence of heteroskedasticity

- Implication: Assumption 3 approximately holds

- Decision: Still report robust SEs (good practice)

**Case 2: Robust SE > Standard SE (difference > 20%)**

- Example: Robust SE = 15.0, Standard SE = 10.0

- Interpretation: Evidence of heteroskedasticity

- Implication: Standard SEs underestimate uncertainty

- Consequence: Default t-stats too large, p-values too small

- Risk: False positives (finding significance that isn't real)

- Decision: MUST use robust SEs

**Case 3: Robust SE < Standard SE (less common)**

- Example: Robust SE = 8.0, Standard SE = 10.0

- Interpretation: Specific pattern of heteroskedasticity

- Implication: Standard SEs overestimate uncertainty

- Consequence: Default t-stats too small, p-values too large

- Risk: False negatives (missing real significance)

- Decision: Use robust SEs (more powerful)

**Visual comparison for our house price data:**

```

Variable: size

Standard SE: 11.17 |████████████████████|

Robust SE: 11.33 |█████████████████████| (+1.4%)

Variable: Intercept

Standard SE: 21,489 |████████████████████|

Robust SE: 20,299 |███████████████████| (-5.5%)

```

**Impact on inference:**

Let's see how the choice affects our conclusions:

| Test | Standard SE | Robust SE | Conclusion |

|------|-------------|-----------|------------|

| t-statistic | 73.77/11.17 = 6.60 | 73.77/11.33 = 6.51 | Both highly significant |

| p-value | 0.0000 | 0.0000 | Both p < 0.001 |

| 95% CI | [50.84, 96.70] | [50.52, 97.02] | Nearly identical |

| Reject H₀? | YES | YES | Same conclusion |

**When robust SEs matter most:**

1. **Large sample differences**

- If robust SE = 2 × standard SE

- Significance can disappear

- Example: t = 2.5 (p=0.02) → t = 1.25 (p=0.22)

2. **Borderline significance**

- If p-value near 0.05 with standard SEs

- Might become non-significant with robust SEs

- Example: p = 0.04 → p = 0.07

3. **High-stakes decisions**

- Policy recommendations

- Medical treatments

- Financial investments

- Need valid inference

**Reading regression output in practice:**

Most statistical software now reports both:

```

Standard Robust

Variable Coef. SE t SE t

size 73.77 11.17 6.60 11.33 6.51

```

**What to report in your paper:**

**Minimum:** Robust standard errors in main results

**Better:** Show both, explain differences if substantial

**Best:** Report robust SEs, note "Results similar with classical SEs"

**Example write-up:**

"We find that each additional square foot is associated with a \$73.77 higher house price (robust SE = 11.33, t = 6.51, p < 0.001). The heteroskedasticity-robust standard error is nearly identical to the classical standard error (11.17), suggesting homoskedasticity is approximately satisfied. The effect is highly statistically significant and economically meaningful, with a 95% confidence interval of [\$50.52, \$97.02]."

**Common mistakes to avoid:**

1. **Using standard SEs for cross-sectional data**

- Modern practice: Always use robust SEs

2. **Testing for heteroskedasticity first**

- Just use robust SEs (they're valid either way)

- Pre-testing affects inference in complex ways

3. **Switching between standard and robust to get significance**

- This is p-hacking

- Choose robust SEs before looking at results

4. **Ignoring large differences**

- If robust SE >> standard SE, investigate

- Might indicate model misspecification

- Consider transformations or different functional forms

**The bottom line:**

Think of robust SEs as the "safe" choice:

- If no heteroskedasticity: Robust SEs ≈ Standard SEs (no harm done)

- If heteroskedasticity exists: Robust SEs correct the problem (saved you!)

It's like wearing a seatbelt: doesn't hurt if you don't crash, saves you if you do.

As a compact recap, the next cell repeats the $H_0: \beta_2 = 90$ test in three lines, pulling the coefficient and standard error directly from the fitted model object — the t-statistic and p-value match the Section 7.5 results.

```{python}

# Hypothesis test using manual t-statistic (pyfixest)

t_manual = (model_basic.coef()['size'] - null_value) / model_basic.se()['size']

p_manual = 2 * (1 - stats.t.cdf(abs(t_manual), df))

print(f"Test H₀: size = {null_value}")

print(f" t-statistic: {t_manual:.4f}")

print(f" p-value: {p_manual:.4f}")

```

## 7.6 One-Sided Directional Hypothesis Tests

Sometimes we have a directional hypothesis (greater than or less than).

**One-sided tests:**

1. **Upper one-tailed**: $H_0: \beta_2 \leq \beta_2^*$ vs $H_a: \beta_2 > \beta_2^*$

- Reject in the right tail: $p = Pr[T_{n-2} > t]$

2. **Lower one-tailed**: $H_0: \beta_2 \geq \beta_2^*$ vs $H_a: \beta_2 < \beta_2^*$

- Reject in the left tail: $p = Pr[T_{n-2} < t]$

**Example**: Test whether house price rises by less than \$90 per square foot.

- Claim: $\beta_2 < 90$

- Test: $H_0: \beta_2 \geq 90$ vs $H_a: \beta_2 < 90$ (lower-tailed)

- $t = (73.77 - 90) / 11.17 = -1.452$

- $p = Pr[T_{27} < -1.452] = 0.079$

- Since $p = 0.079 > 0.05$, do not reject $H_0$ at 5% level

- **Conclusion**: Not enough evidence to support the claim at 5% level

**Note on computer output:**

- Computer gives p-value for two-sided test of $H_0: \beta_2 = 0$

- For one-sided test of significance:

- If $b_2$ has expected sign, halve the printed p-value

- If $b_2$ has wrong sign, reject is not possible (p > 0.5)

```{python}

# 7.6 One-sided directional hypothesis tests

# Upper one-tailed test: H₀: β₂ ≤ 90 vs H₁: β₂ > 90

p_value_upper = 1 - stats.t.cdf(t_stat_90, df)

t_crit_upper = stats.t.ppf(0.95, df) # one-sided test

print(f"\nUpper one-tailed test: H₀: β₂ ≤ {null_value} vs H₁: β₂ > {null_value}")

print(f" t-statistic: {t_stat_90:.4f}")

print(f" p-value (one-tailed): {p_value_upper:.6f}")

print(f" Critical value (α=0.05): {t_crit_upper:.4f}")

if t_stat_90 > t_crit_upper:

print(" Result: Reject H₀")

else:

print(" Result: Fail to reject H₀")

# Lower one-tailed test: H₀: β₂ ≥ 90 vs H₁: β₂ < 90

p_value_lower = stats.t.cdf(t_stat_90, df)

print(f"\nLower one-tailed test: H₀: β₂ ≥ {null_value} vs H₁: β₂ < {null_value}")

print(f" t-statistic: {t_stat_90:.4f}")

print(f" p-value (one-tailed): {p_value_lower:.6f}")

print(f" Critical value (α=0.05): {-t_crit_upper:.4f}")

if t_stat_90 < -t_crit_upper:

print(" Result: Reject H₀")

print(" Conclusion: There is evidence that β₂ < 90")

else:

print(" Result: Fail to reject H₀")

print(" Conclusion: Not enough evidence to support β₂ < 90 at 5% level")

print(f" (Would reject at 10% level since p = {p_value_lower:.3f} < 0.10)")

```

## 7.7 Robust Standard Errors

Default standard errors make assumptions 1-4. Robust standard errors relax some of these assumptions.

**Heteroskedasticity-Robust Standard Errors:**

- **Default assumption** (homoskedasticity): $Var[u_i | x_i] = \sigma_u^2$ (constant)

- **Relaxed assumption** (heteroskedasticity): $Var[u_i | x_i] = \sigma_i^2$ (varies with $i$)

**Why use robust standard errors?**

- Heteroskedasticity is common in cross-sectional data

- Default SEs are incorrect when heteroskedasticity is present

- Robust SEs are valid whether or not heteroskedasticity exists

- **Modern practice**: Always report robust SEs for cross-sectional data

**Heteroskedastic-robust SE formula:**

$$se_{het}(b_2) = \frac{\sqrt{\sum_{i=1}^n e_i^2 (x_i - \bar{x})^2}}{\sum_{i=1}^n (x_i - \bar{x})^2}$$

**Effect on inference:**

- Coefficient estimates unchanged

- Standard errors typically increase (more conservative)

- t-statistics typically decrease

- Confidence intervals typically wider

**Other robust SEs:**

- **HAC robust**: For time series with autocorrelation

- **Cluster robust**: For clustered data (students in schools, people in villages, etc.)

The cell below re-estimates the same regression with `vcov='HC1'` and collects classical and robust standard errors side by side — for these data the robust SE on `size` (11.33) barely differs from the classical one (11.17).

```{python}

# 7.7 Robust standard errors

robust_results = pf.feols('price ~ size', data=data_house, vcov='HC1')

# Comparison of standard and robust standard errors

comparison_df = pd.DataFrame({

'Coefficient': model_basic.coef(),

'Std. Error': model_basic.se(),

'Robust SE': robust_results.se(),

't-stat (standard)': model_basic.tstat(),

't-stat (robust)': robust_results.tstat(),

'p-value (standard)': model_basic.pvalue(),

'p-value (robust)': robust_results.pvalue()

})

comparison_df

```

### Full Regression Output with Robust Standard Errors

The full summary now reports `Inference: HC1`: the coefficients are identical to the classical fit — only the standard errors, t-statistics, and confidence intervals change.

```{python}

# Regression with robust standard errors

robust_results.summary()

```

### Visualization: Scatter Plot with Regression Line

Visual representation of the bivariate regression relationship.

```{python}

# Figure 7.1: Scatter plot with regression line

fig, ax = plt.subplots(figsize=(10, 6))

ax.scatter(data_house['size'], data_house['price'],

alpha=0.6, s=50, # alpha = transparency, s = marker size

color='#22d3ee', label='Actual observations')

ax.plot(data_house['size'], model_basic.predict(), color='#c084fc',

linewidth=2, label='Fitted regression line')

ax.set_xlabel('Size (square feet)', fontsize=12)

ax.set_ylabel('Price (dollars)', fontsize=12)

ax.set_title('Figure 7.1: House Price vs Size with Regression Line',

fontsize=14, fontweight='bold')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

```

**What to look for in this scatter plot:**

- **Direction**: Positive -- larger houses tend to have higher prices

- **Form**: Roughly linear -- the points follow an upward-sloping pattern consistent with our regression model

- **Scatter**: Points do not lie exactly on the line -- this variation is the residual "error" that the model cannot explain

- **Regression line**: The fitted line summarizes the average relationship, with the slope reflecting $73.77 per additional square foot

### Visualization: Confidence Intervals

Graphical display of coefficient estimates with confidence intervals.

```{python}

# Figure 7.2: Confidence interval visualization

fig, ax = plt.subplots(figsize=(10, 6))

# Plot point estimate and confidence interval

coef_names = ['Intercept', 'Size']

coefs = model_basic.coef().values

ci_low = conf_int.iloc[:, 0].values

ci_high = conf_int.iloc[:, 1].values

y_pos = np.arange(len(coef_names))

ax.errorbar(coefs, y_pos, xerr=[coefs - ci_low, ci_high - coefs],

fmt='o', markersize=8, capsize=5, capthick=2, linewidth=2, color='#22d3ee')

ax.set_yticks(y_pos)

ax.set_yticklabels(coef_names)

ax.axvline(x=0, color='red', linestyle='--', linewidth=1, alpha=0.5,

label='H₀: β = 0')

ax.set_xlabel('Coefficient Value', fontsize=12)

ax.set_title('Figure 7.2: Coefficient Estimates with 95% Confidence Intervals',

fontsize=14, fontweight='bold')

ax.legend()

ax.grid(True, alpha=0.3, axis='x')

plt.tight_layout()

plt.show()

```

**What to look for in this confidence interval plot:**

- **Exclusion of zero**: If the confidence interval does not cross the red dashed line (zero), the coefficient is statistically significant at the 5% level

- **Width**: Wider intervals indicate less precision in the estimate; narrower intervals indicate more certainty

- **Both coefficients**: The intercept and size coefficient are both statistically significant since neither CI contains zero

### Visualization: Residual Plot

Check for patterns in residuals that might violate model assumptions.

```{python}

# Figure 7.3: Residual plot

fig, ax = plt.subplots(figsize=(10, 6))

ax.scatter(model_basic.predict(), model_basic._u_hat,

alpha=0.6, s=50, color='#22d3ee') # alpha = transparency, s = marker size

ax.axhline(y=0, color='red', linestyle='--', linewidth=2, label='Zero residual line')

ax.set_xlabel('Fitted values', fontsize=12)

ax.set_ylabel('Residuals', fontsize=12)

ax.set_title('Figure 7.3: Residual Plot', fontsize=14, fontweight='bold')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

```

**What to look for in this residual plot:**

- **Random scatter**: Residuals should appear randomly distributed around zero -- no discernible pattern

- **Constant spread**: The vertical spread of residuals should be roughly the same across all fitted values (homoskedasticity)

- **Funnel shape**: If the spread widens or narrows, this signals heteroskedasticity -- robust standard errors are needed

- **Outliers**: Points far from zero may be influential observations worth investigating

## Key Takeaways

1. **The t-statistic** is fundamental to statistical inference in regression:

- Formula: $t = \frac{b_2 - \beta_2}{se(b_2)} \sim T(n-2)$

- Parallels univariate inference: $t = \frac{\bar{x} - \mu}{se(\bar{x})} \sim T(n-1)$

2. **Confidence intervals** provide a range of plausible values:

- Formula: $b_2 \pm t_{n-2, \alpha/2} \times se(b_2)$

- 95% CI (approximate): $b_2 \pm 2 \times se(b_2)$

- Interpretation: 95% of such intervals will contain the true $\beta_2$

3. **Tests of statistical significance** assess whether a regressor matters:

- $H_0: \beta_2 = 0$ vs $H_a: \beta_2 \neq 0$

- Reject if $p$-value $< \alpha$ or $|t| > t_{n-2, \alpha/2}$

- Statistical significance $\neq$ economic significance

4. **Two-sided tests** for specific values:

- $H_0: \beta_2 = \beta_2^*$ vs $H_a: \beta_2 \neq \beta_2^*$

- Equivalent to checking if $\beta_2^*$ is in the confidence interval

5. **One-sided tests** for directional hypotheses:

- Upper tail: $H_0: \beta_2 \leq \beta_2^*$ vs $H_a: \beta_2 > \beta_2^*$

- Lower tail: $H_0: \beta_2 \geq \beta_2^*$ vs $H_a: \beta_2 < \beta_2^*$

- p-value is half the two-sided p-value (if sign is correct)

6. **Robust standard errors** provide valid inference under weaker assumptions:

- Heteroskedasticity-robust (HC1): Relaxes constant variance assumption

- Modern practice: Always use for cross-sectional data

- Other types: HAC (time series), cluster (grouped data)

**Model Assumptions (1-4):**

1. Linearity: $y = \beta_1 + \beta_2 x + u$

2. Zero conditional mean: $E[u_i | x_i] = 0$

3. Constant variance: $Var[u_i | x_i] = \sigma_u^2$ (relaxed with robust SEs)

4. Independence: $u_i$ independent of $u_j$

**House Price Example Results:**

- Coefficient: Each additional sq ft is associated with \$73.77 higher price

- 95% CI: [\$50.84, \$96.70]

- Highly statistically significant (t = 6.60, p < 0.001)

- Economically meaningful effect

**Python Tools Used:**

- `pandas`: Data manipulation and summary statistics

- `pyfixest`: Econometric estimation and hypothesis testing

- `scipy.stats`: Statistical distributions and critical values

- `matplotlib` & `seaborn`: Visualization

**Practical Skills Developed:**

- Conducting t-tests on regression coefficients

- Constructing and interpreting confidence intervals

- Testing economic hypotheses (two-sided and one-sided)

- Using robust standard errors for valid inference

- Visualizing regression results

- Distinguishing statistical from economic significance

**Python Libraries and Code:**

This single code block reproduces the core workflow of Chapter 7. It is self-contained — copy it into an empty notebook and run it to review the complete pipeline from data loading to hypothesis testing, confidence intervals, and robust standard errors.

```python

# =============================================================================

# CHAPTER 7 CHEAT SHEET: Statistical Inference for Bivariate Regression

# =============================================================================

# --- Libraries ---

import pandas as pd # data loading and manipulation

import matplotlib.pyplot as plt # creating plots and visualizations

import pyfixest as pf # fast estimation with robust SEs

from scipy import stats # t-distribution and critical values

# =============================================================================

# STEP 1: Load data directly from a URL

# =============================================================================

# pd.read_stata() reads Stata .dta files — the house price dataset has 29 houses

url = "https://raw.githubusercontent.com/quarcs-lab/data-open/master/AED/AED_HOUSE.DTA"

data_house = pd.read_stata(url)

print(f"Dataset: {data_house.shape[0]} observations, {data_house.shape[1]} variables")

# =============================================================================

# STEP 2: Estimate the regression and extract key statistics

# =============================================================================

# The t-statistic measures how many standard errors the estimate is from zero

model = pf.feols('price ~ size', data=data_house)

slope = model.coef()['size'] # marginal effect: $/sq ft

intercept = model.coef()['Intercept']

se_slope = model.se()['size'] # standard error of the slope

t_stat = model.tstat()['size'] # t = b2 / se(b2)

p_value = model.pvalue()['size'] # two-sided p-value for H0: b2 = 0

print(f"Estimated equation: price = {intercept:,.0f} + {slope:.2f} × size")

print(f"Standard error of slope: {se_slope:.2f}")

print(f"t-statistic: {t_stat:.4f}")

print(f"p-value: {p_value:.6f}")

# Full regression table (coefficients, std errors, t-stats, p-values, R²)

model.summary()

# =============================================================================

# STEP 3: Confidence interval — a range of plausible values for β₂

# =============================================================================

# CI = b2 ± t_crit × se(b2), using T(n-2) distribution

n = len(data_house)

df = n - 2 # degrees of freedom

t_crit = stats.t.ppf(0.975, df) # critical value for 95% CI

ci_lower = slope - t_crit * se_slope

ci_upper = slope + t_crit * se_slope

print(f"Degrees of freedom: {df}")

print(f"Critical t-value (α=0.05, two-sided): {t_crit:.4f}")

print(f"95% CI for slope: [{ci_lower:.2f}, {ci_upper:.2f}]")

print(f"Interpretation: each sq ft adds between ${ci_lower:.0f} and ${ci_upper:.0f} to price")

# =============================================================================

# STEP 4: Hypothesis tests — does size matter? Is the effect $90/sq ft?

# =============================================================================

# Test 1: Statistical significance (H0: β₂ = 0)

print(f"Test H₀: β₂ = 0 → t = {t_stat:.2f}, p = {p_value:.6f} → Reject H₀")

# Test 2: Two-sided test for a specific value (H0: β₂ = 90)

null_value = 90

t_90 = (slope - null_value) / se_slope

p_90 = 2 * (1 - stats.t.cdf(abs(t_90), df))

print(f"Test H₀: β₂ = 90 → t = {t_90:.4f}, p = {p_90:.4f} → Fail to reject H₀")

print(f" (90 is inside the 95% CI [{ci_lower:.2f}, {ci_upper:.2f}])")

# =============================================================================

# STEP 5: One-sided test — does size increase price by less than $90/sq ft?

# =============================================================================

# H0: β₂ ≥ 90 vs Ha: β₂ < 90 (lower-tailed test)

p_lower = stats.t.cdf(t_90, df) # one-sided p-value (left tail)

print(f"One-sided test H₀: β₂ ≥ 90 vs Hₐ: β₂ < 90")

print(f" t = {t_90:.4f}, one-sided p = {p_lower:.4f}")

print(f" Fail to reject at 5% (p = {p_lower:.3f} > 0.05)")

print(f" Would reject at 10% (p = {p_lower:.3f} < 0.10)")

# =============================================================================

# STEP 6: Robust standard errors — valid with or without heteroskedasticity

# =============================================================================

# HC1 robust SEs protect against non-constant variance in the errors

robust_model = pf.feols('price ~ size', data=data_house, vcov='HC1')

print(f"{'':20s} {'Standard':>12s} {'Robust (HC1)':>12s}")

print("-" * 46)

print(f"{'SE(size)':<20s} {se_slope:>12.2f} {robust_model.se()['size']:>12.2f}")

print(f"{'t-statistic':<20s} {t_stat:>12.2f} {robust_model.tstat()['size']:>12.2f}")

print(f"{'p-value':<20s} {p_value:>12.6f} {robust_model.pvalue()['size']:>12.6f}")

pct_change = ((robust_model.se()['size'] - se_slope) / se_slope) * 100

print(f"\nRobust SE is {pct_change:+.1f}% different from standard SE")

# =============================================================================

# STEP 7: Scatter plot with regression line and inference summary

# =============================================================================

fig, ax = plt.subplots(figsize=(10, 6))

ax.scatter(data_house['size'], data_house['price'], s=50, alpha=0.7, label='Actual prices')

ax.plot(data_house['size'], model.predict(), color='red', linewidth=2, label='Fitted line')

ax.set_xlabel('House Size (square feet)')

ax.set_ylabel('House Sale Price (dollars)')

ax.set_title(f'price = {intercept:,.0f} + {slope:.2f} × size '

f'95% CI for slope: [{ci_lower:.0f}, {ci_upper:.0f}]')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

```

**Try it yourself!** Copy this code into an empty Google Colab notebook and run it: [Open Colab](https://colab.research.google.com/notebooks/empty.ipynb)

**Next Steps:**

- Extend to multiple regression (Chapter 11)

- Learn about model specification and variable selection

- Study violations of assumptions and diagnostics

- Practice with different datasets and research questions

---

**Congratulations!** You've completed Chapter 7. You now have both theoretical understanding and practical skills in conducting statistical inference for bivariate regression models!

> **Common Mistakes to Avoid**

>

> - **Using standard errors when heteroskedasticity is present**: Always check robust standard errors

> - **Confusing confidence intervals for prediction intervals**: CIs are for the mean response, not individual observations

> - **Forgetting to check model assumptions before interpreting p-values**

## Practice Exercises

**Exercise 1: Understanding Standard Errors**

Suppose you estimate a regression of wages on education using data from 100 workers. The estimated slope is b₂ = 5.2 (each additional year of education increases wages by \$5.20/hour) with standard error se(b₂) = 1.8.

a) Calculate the 95% confidence interval for β₂ (use t-critical value ≈ 2.0).

b) Interpret the confidence interval in plain language.

c) If the sample size were 400 instead of 100, how would the standard error change (approximately)? Explain why.

**Exercise 2: Hypothesis Testing Mechanics**

Using the wage-education regression from Exercise 1 (b₂ = 5.2, se(b₂) = 1.8):

a) Test H₀: β₂ = 0 vs. Hₐ: β₂ ≠ 0 at the 5% level. Calculate the t-statistic and state your conclusion.

b) Calculate the approximate p-value for this test.

c) Would you reject H₀ at the 1% level? Explain.

**Exercise 3: Two-Sided Tests**

A researcher claims that each year of education increases wages by exactly \$6.00/hour. Using the regression from Exercise 1:

a) State the null and alternative hypotheses to test this claim.

b) Calculate the test statistic.

c) At the 5% level, do you reject the researcher's claim? Explain your reasoning.

d) Is the claim consistent with the 95% confidence interval from Exercise 1?

**Exercise 4: One-Sided Tests**